3 SFC model presentation

Flexible rate mortgage loans: An SFC model of the impact of mortgage credit innovations on Danish balance sheet stability

Abstract

Innovations in mortgage lending options have expounded in recent decades, resulting primarily in a reduction in the initial monthly costs associated with borrowing, and made home ownership possible for socio-economic groups that were previously excluded from the market. These changes have also drastically changed the composition of household balance sheets, both at a micro and a macro level, and the volume of outstanding debt relative to household income expanded aggressively leading up to the global financial crisis in 2007-8. The innovations unfortunately also simultaneously transferred significant risks to borrowers. This paper investigates the present day macroeconomic consequences of the change in composition from fixed- to adjustable-rate mortgage (ARM) debt that occurred in Denmark between 2003 and 2009. A state-of-the-art Stock-Flow Consistent model is adapted to allow for changes in the composition of debt, and to permit shifts in the proportion of debt between fixed-interest and ARM products. The risks to financial stability are evaluated through the imposition of two plausible shocks to the economy: the first is a two percentage point rise in borrowing costs; and, the second is a 20 per cent decline in property prices. The model allows for a clear observation of the transmission channels, and the stocks and flows most at risk, and the results suggest that the expansion of ARM mortgage credit has increased the instability of the household sector. An interesting observation was that a positive net lending response can be misinterpreted as positive developments in the absence of the broader economic context. The paper is supplemented by a new presentation method for SFC model responses, where a cross-section of proportional responses are ranked, ordered and categorised in tabular form.

3.1 Introduction

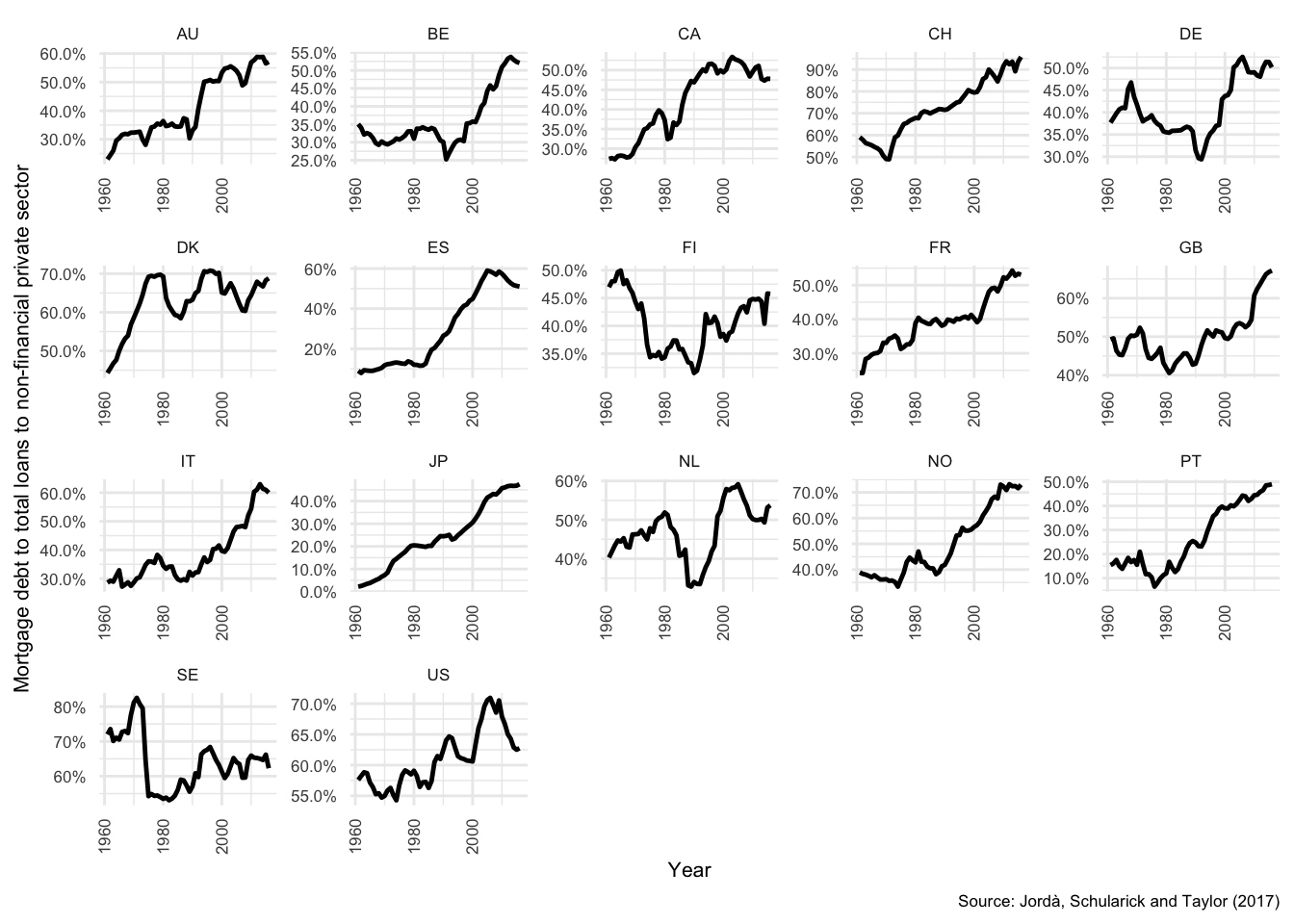

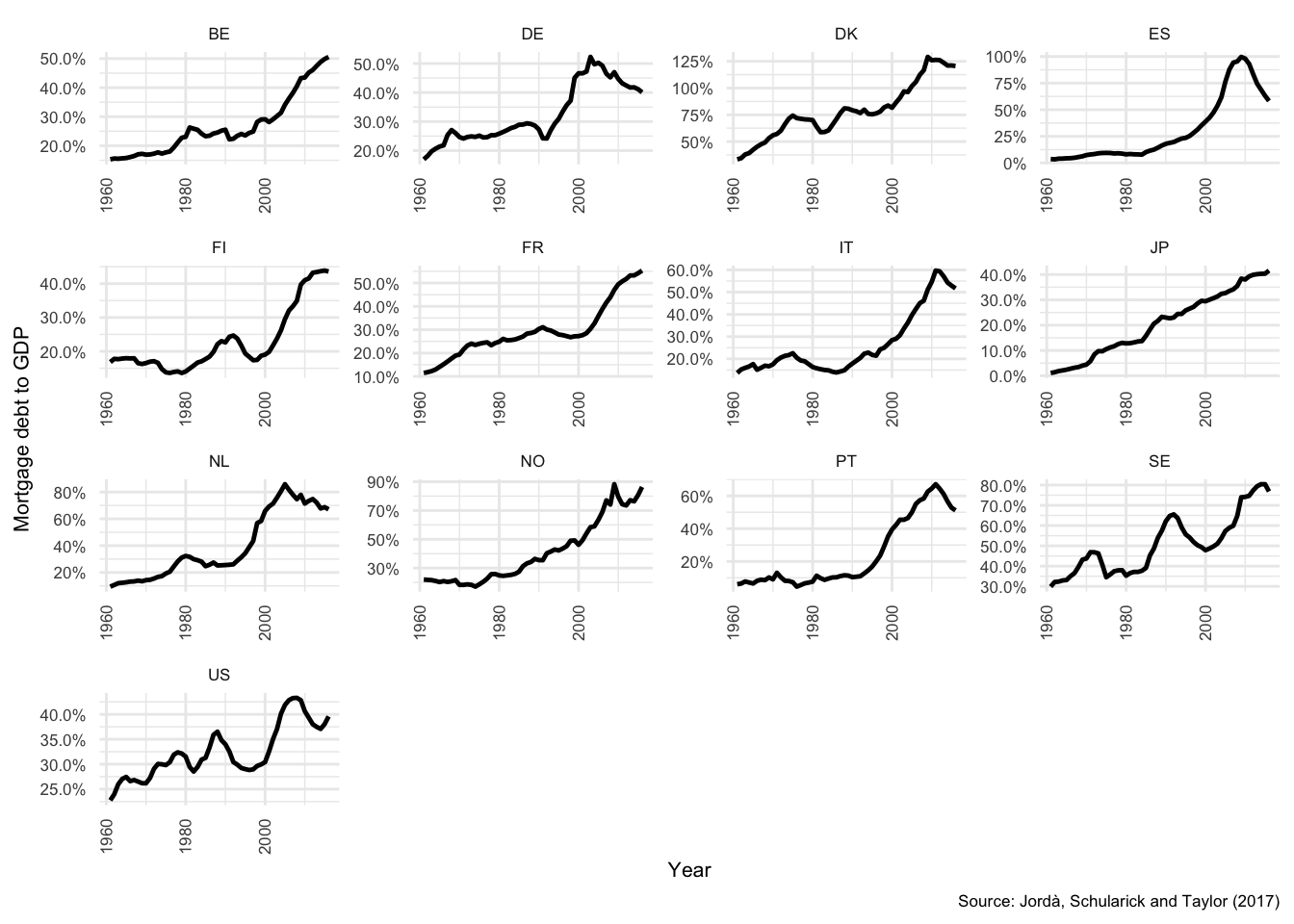

Private sector debt continues to be a concern in many developed countries, in particular mortgage debt. Debt levels expanded in most developed countries during the period leading up to the financial crisis, in the household sector this was driven primarily by the extension of mortgage credit (as can be seen in Figure , Section ). The proportion of mortgage debt to total debt increased in all countries from around 1960, but accelerated dramatically during the 1990s and 2000s (Jordà, Schularick, and Taylor 2017). That growth was unfortunately not matched by growth in household incomes, and debt-to-income continued to expand for all countries until the great financial crisis in 2007-08 (see Figure in Section ). In most countries, the supply of credit slowed or even reversed as liquidity in overnight markets dried up during the financial crisis1.

The growing debt, particularly relative to income, carries several significant risks to financial stability. These include several demand related risks, such as the future need to deleverage and the associated intertemporal substitution of demand (Justiniano, Primiceri, and Tambalotti 2015; Raberto, Teglio, and Cincotti 2012; Seppecher and Salle 2015), deterioration of balance sheets and potential risks to refinancing requirements (B. S. Bernanke 2007; Scanlon, Lunde, and Whitehead 2008; Disyatat 2011), and sensitivity of interest payments to rate changes (Sheehy 2014). There are also possible contagion effects across financial markets of default (or non-performance on loans), asset price adjustments and possible deterioration of financial intermediary capital positions (Danmarks Nationalbank 2016). As seen in credit-default-swap market during the 2007-08 financial crisis, the possible collapse of liquidity in certain markets can also generate global instability. At a sectoral level there is also the general risk of the accumulation of large imbalances, such as government or foreign deficits, that can take many years to unwind.

While there are a number of parallels between various housing finance systems, the stability of each is unique to a variety of in and out of country conditions. The European Network of Housing Research (ENHR) (Lunde and Whitehead 2014) found that Political, geographical and institutional factors were not sufficient to explain significant differences in developments across 21 OECD countries since 1989. They (Lunde and Whitehead 2014, 4) noted that “housing finance systems are very specific to each country, reflecting different histories, legal systems, institutions, economic conditions, policies and politics.” It is therefore necessary to explore the particular dynamics that are at play in each country.

This paper focuses on the Danish system, which makes an excellent country for a number of reasons. Firstly, the Danish housing finance system has been no stranger to innovation, with a number of legislative and product changes introduced since 2003. It is also a relatively small and open economy with strong international trade ties and close ties with the European Union. Thus, a number of parallels can be drawn between the Danish system and several other countries with advanced mortgage financing systems. Denmark is also one of the very few countries that has reliable data for institutional sector balance sheets in granular detail from 1995, and sub-sector level data from 2003. This data allows one to study the problem from comprehensive empirical data. It also allows one to construct a model that integrates the complex interactions and feedback mechanisms of the five institutional sectors that is founded on observable empirical relationships2.

In this paper I modify an existing empirical stock flow consistent (SFC) model for the Danish economy first presented by Byrialsen and Raza (2019). As explained by Wynne Godley and Lavoie (2012), these models maintain strict stock and flow consistency, in the sense that all flows are accounted for in a complete system of accumulations in the stocks of all five major institutional sectors. It attempts to capture the aggregate drivers of macroeconomic interactions as they happen in real time, although it uses ex post aggregate accounting values to estimate these relationships.

The completeness of the model requires that some of the variables in the model are passive to changes in others. The choice of the active variables over the passive (residual) variables is determined by a combination of accounting identities and economic theory, in this case, Post Keynesian theory. The grounds for this decision are discussed in Section .

Since the household sector is at the core of the analysis in the model, most sectors are passive to changes in the household sector, and it combines the attractive features of econometrics (structural econometric models, SEMs) with path dependency and Post Keynesian behaviours. In the strict sense the model does not demonstrate causality. Rather, it estimates the expected co-movement of certain economic aggregates based on historical evidence and theoretical expectations. These estimates inform several parameters in a medium sized system of equations3.

The core focus of the investigation in this version of the model is the Danish mortgage system, and the expected macroeconomic consequences of innovations in the mortgage product range offered to Danish borrowers. The model in Byrialsen and Raza (2019) is the most advanced empirical SFC model available for Denmark, and thus provides the best possible point of departure. The model is under continuous development, and there are some limitations imposed by the largely exogenous nature of rates of return (including interest rates) and asset prices. A secondary goal is to identify any potential improvements to the existing model with respect to mortgage credit markets.

The original structure is modified to include a split in household debt between fixed and flexible rate products. This allows for the evaluation of the effects of proportional shifts in credit composition. In particular, to investigate the short-term implications for the accumulation of stocks in the household sector of a shift in the proportion of debt from flexible-interest-rate debt to fixed-interest-rate debt, and vice versa4. The exogenous nature of rates of return and financial asset prices is both an advantage and disadvantage. On the one hand they allow for specific channels in the model to be highlighted, free of disturbance of from inter-connected markets. On the other hand, it implies that market rates and price fluctuations are not propagated automatically. This makes the overall model results less realistic.

One of the major benefits of the SFC framework is that it allows for path dependent accumulation of imbalances. Although there are some limitations (as discussed below), it is thus possible to fully account for feedback effects from accumulations in selected asset classes, albeit within a simple structure. The analysis that follows may also be of value in the assessment of mortgage financing structures in a macroeconomic framework, and contributes to the growing literature on empirical SFC models.

The remainder of the paper is structured as follows, Section presents a review of the literature, and Section provides context for the Danish mortgage market. Section describes the model, and explains some of the key innovations made in this paper, and Section explains the scenarios for shocks applied to the model. In Section the effects of the shocks are described for each of the scenarios, taken from the perspective of each of the main institutional sectors. Section contains a discussion of the main observations from the model, and Section concludes. The first appendix, Section , contains a number of additional charts and figures, and the second appendix, Section , provides a full exposition of the model employed, together with explanations for the major innovations.

3.2 Literature and theory

3.2.1 Stock flow consistent models

Stock flow consistent (SFC) models are a relatively new branch of macroeconomic model, and as mentioned above, are characterised by strict adherence to double entry accounting rules. They resemble structural econometric models, but the expected behaviours that are modelled are typically informed by Post Keynesian theory. W. Godley and Lavoie (2007)5 is widely regarded as the catalyst for the recent growth in research using the SFC framework, and since 2007 the number of models has grown rapidly.

As noted by Nikiforos and Zezza (2017, 3), “accounting consistency is just one side of the SFC approach, with a demand-led economy and an explicit treatment of the financial side being the other.” Dos Santos (2006), Caverzasi and Godin (2013), Caverzasi and Godin (2015) and Nikiforos and Zezza (2017) provide surveys of the literature, each progressively covering the most recent publications. These studies provide a comprehensive review of both the topic and methodological coverage of SFC research. SFC models can be separated into three broad categories; theoretical models, which are typically much simpler and are used for the exploration of theoretical propositions; simulated calibrated models, which are larger models that are constructed to have similar features to real economies, but where the underlying data is constructed for illustrative purposes; and, empirical models, where the entire model is based on real-world data. While each form presents challenges, empirical models face additional challenges with regards availability and reliability of data. Where data is available, the researcher is faced with the challenge of appropriate aggregation.

There are relatively few fully empirical SFC models in the literature, and the number of models for which comprehensive data was available is even lower. The model presented below is an empirical model, based on the one constructed by Byrialsen and Raza (2019). Unlike many other empirical SFC models, it is constructed from the ground up, rather than adapted from one of the more broadly used Wynne Godley and Lavoie (2012) models. This approach mirrors that suggested by Gennaro Zezza and Zezza (2019), where the full complexity of national accounts data is used as the point of departure. The explicit treatment of the financial side entails significant simplification of the wide variety of financial instruments that are available.

Much like many other modelling forms, the complexity of an SFC model has implications for how easily the results can be interpreted. The greater the number of interdependent features, the lower the transparency of transmission mechanisms. In summary of a central banker forum, Pill (2001, 25) noted that some participants argued that large “eclectic” macroeconomic models often “lack the simplicity, internal consistency and intuitive appeal which are prerequisites for providing good policy advice.” In contrast, others “suggested that preparing policy guidance in the context of a single model allowed a holistic and rich picture of the economic situation to be obtained.” This conflict between holistic context and intuitive simplicity was a key part of the decision to keep rates of return exogenous in the present model. It also provides some explanation of the aggregation process. A careful investigation of the size and relative importance of various stocks and flows was conducted to render the model to workable size. Further details regarding the actual aggregation of different categories financial and real flows are provided in Section .

This process requires detailed data, particularly in terms of the balance sheets and flow-of-funds between the institutional sectors. This data is available for very few countries for a long enough time-period to be able to estimate statistical relationships, and Denmark is one of those countries. The model is based on annual data from 1995 to 2017, and there are thus a maximum of twenty two observations in any estimation and the extent to which the model effectively follows the data is comprehensively illustrated in Byrialsen and Raza (2019).

3.2.2 Post Keynesian theoretical foundations

The theoretical basis of the model informs the behaviours in and ordering of equations. Since the publication of Wynne Godley and Lavoie (2012)’s first edition in 2007, the number of SFC models developed globally has grown exponentially, and due to the Post Keynesian roots of the framework, the bulk of these models could be referred to as Post Keynesian Stock Flow Consistent models (PK-SFC models), PK will henceforth be used refer to the “Post Keynesian” school of thought. PK theory is typically juxtaposed with the New Neo-Classical synthesis, or New Keynesianism in order to highlight the points of difference. Such a discussion is beyond the scope of this paper6, and a brief summary of the key characteristics of PK systems will need to suffice here, with a special focus on those parts used to inform the model below.

In terms of the trajectory of the economy, PKs typically reject the notion of a long run equilibrium in favour of path dependency, and argue that present decisions and institutional structures materially change the nature of the economy in the future. For the present model, this is reflected in the focus on short to medium term (typically the first period or two after a shock, but up to approximately 5 years). They argue also that the economy is significantly more complex than the sum of its parts (Chick 2003), and sometimes liken it to an organic entity, or the complex interactions of an ecosystem. Economic trajectories can therefore be altered by active intervention and long term historical averages are therefore not predictive of future events. This is reflected in the model below by a lack of long-run mean reversion or stabilising elements in the model. The most significant omission relative to mainstream literature is the inter-temporal optimisation of household consumption. There are no utility functions, and there is no long-run or inter-temporal optimisation of behaviour.

For economic policy concerns, the implication is that financial and social imbalances cannot self-correct (at least not without significant social, political or economic consequences), and market mechanisms are not able to manage these issues automatically. To the contrary, unchecked imbalances that are perpetuated by market structures are problematic. Just as the accumulation of poor quality private debt prior to the 2007-08 GFC proved to be.

PKs often refer to Keynes (1937), who stated that the future is fundamentally uncertain. It is therefore crucial to understand the economy as it presently stands, and to have some idea of what future economic conditions are desirable. It should thereafter be possible to actively plan for and develop a desirable future economic landscape, without the need for projections of the distant future, or acceptance of any long-run equilibria or natural rates. From a modelling perspective it is therefore not necessary that a model be stationary in order to be useful, it is more important that it should be representative of the present reality.

In terms of the sequence of events inside PK models, they emphasise the importance of demand (or rather effective demand7) in the economy, and are predominantly demand driven rather than supply driven - although, more recent works have put more emphasis on supply side constrains (Ryoo and Skott 2008). Keynes’s animal spirits and short term expectations drive investors to either increase or decrease investment. This is also related to the PK theory of an endogenous demand and supply of money in the economy. The demands of possible borrowers are tested against credit worthiness and all viable demand for credit is (or can be) accommodated by the banking sector. New lending creates new money, and therefore the demand for investment funding drives the growth in money. In this model, this analogy is applied to the household sector in that the demand for new housing investment drives the demand for mortgage credit.

There are several estimated equations in the model, and the motivations for each are discussed in a full presentation of the model in Section , in the appendix. The structure of the estimated equations are informed by PK and country specific literature, and refined to reflect the reality of the data.

3.2.3 Credit markets and global financial conditions

From a broader international perspective, the period leading up to the crisis has been called “the great moderation” (as noted by, Buttiglione et al. (2014, 28)) and was an extended period of unprecedented economic growth and apparent stability of financial markets. As noted by Englund (1999), this was accompanied by the relaxation of lending requirements and credit worthiness checks, and as Scanlon, Lunde, and Whitehead (2008) identified, rising property prices and expectations of capital gains. There was a gradual reduction of interest rates, and the cost of borrowing (the long-run cost of capital falling steadily from the 1970s). According to Scanlon, Lunde, and Whitehead (2008), a simultaneous development on a global scale was an increased belief in the market mechanism, extensive privatisation and deregulation of financial markets8. The onset of the global financial crisis (GFC) later revealed significant flaws and systemically risky interdependencies between markets. Even though the initial effects were felt by all countries, the effects, both in terms of intensity and real economic and financial trajectories, differed greatly. (Lunde and Whitehead 2014)

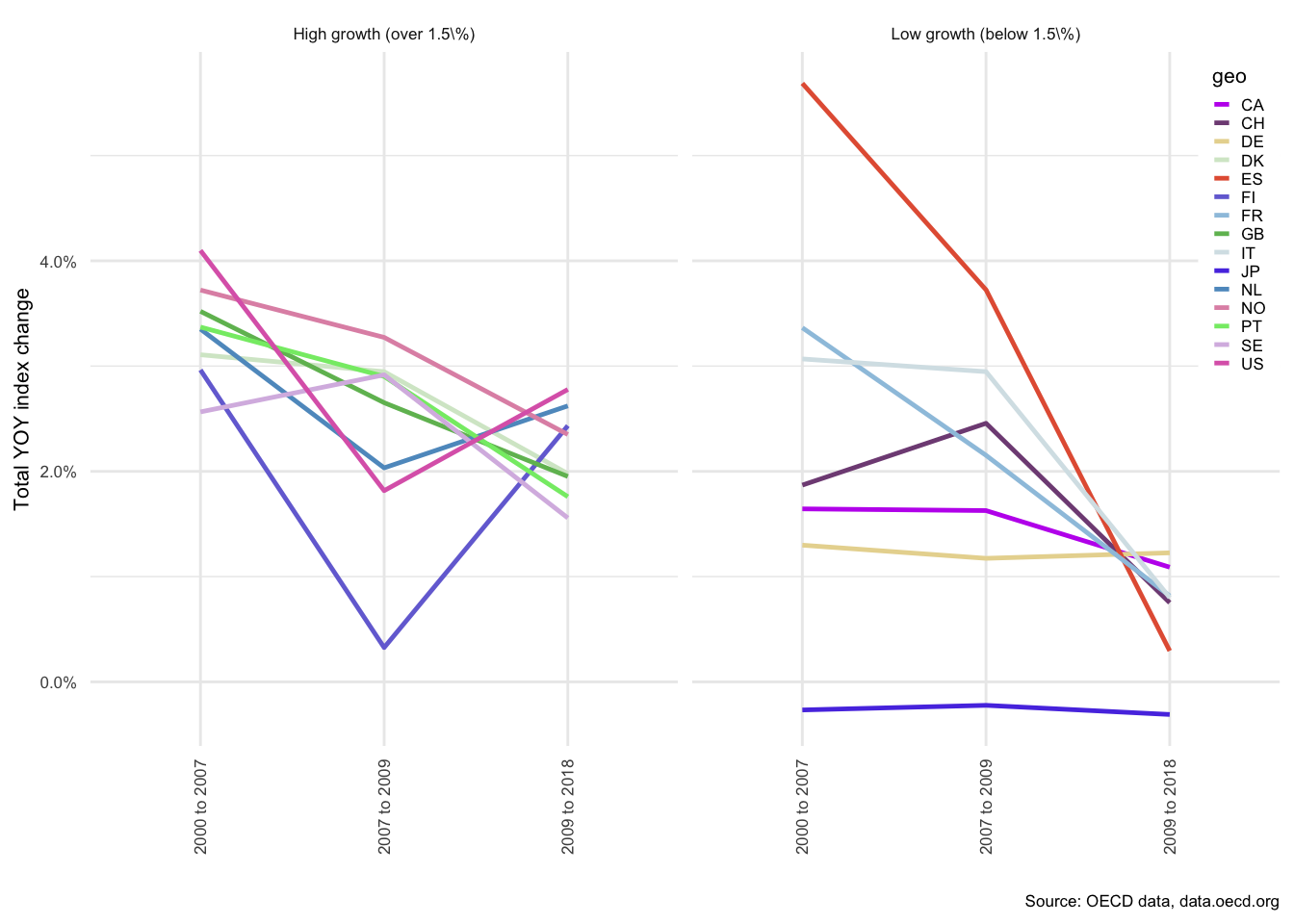

In the post-crisis period, there have been significant changes to the regulatory landscape, and the extent of mortgage lending has slowed or reversed in many countries. At the height of the crisis, liquidity in key financial instruments, particularly credit default swaps, dried up almost instantly (Nationalbank 2009). Ultimately this triggered quantitative easing (QE) policies in both the USA and Europe, with the Fed and the ECB buying immense quantities of financial assets and market-making with the assistance of larger banks. On the regulatory front, banking prudential and capital adequacy requirements were tightened significantly. The period from 2009 to 2018, while not as extreme as the period preceding the crisis, has however, continued to show strong growth in property prices, with more than half of the OECD countries in the sample showing year-on-year growth rates of over 2%, as can be seen in .

US and European QE policies also led to excess liquidity in global financial markets. The low short-term rates have gradually resulted in record low long-term rates of return, placing added pressure on fund management and investment companies to search for yield in unconventional investments9. These policies and other commitments by European central banks and the ECB have contributed significantly to persistent low interest rates in market based mortgage lending systems. While the rate of growth in the level of debt relative to income appears to stabilised in many countries, the magnitude of household debt continues to expand. The risks associated with this debt depend not only on the magnitude of the debt, but also very strongly on its composition.

A correlated development has been the expansion of the product range offered by mortgage lenders. Leading up to 2007, innovations were made to almost every aspect of mortgage lending, and the vast majority of these changes have contributed to a reduction in the initial payments on mortgages for the borrower. According to Scanlon, Lunde, and Whitehead (2008), while the innovations were different according to each specific country, some broader characteristics were similar across developed nations. Two key aspects to these innovations were that they made initial payments on mortgages cheaper, and secondly, they increased the flexibility and range of options available, and thus transferred significant elements of risk to the borrower. André (2016) also explains that house price bubbles are often related to periods of financial de-regulation, and highlights the introduction of interest-only (periods without capital repayments) loans in Denmark in 2003 as an example.

These international developments were not applied uniformly to all countries, or even in specific geographical areas. Lunde and Whitehead (2014) found, rather surprisingly, that in contrast to a geo-political grouping, for example with other Scandinavian countries, Denmark was closer to Finland, Poland and Russia in terms of real economic and housing financing conditions after the 2007-08 financial crisis. An additional point was that the introduction of adjustable rate mortgage (ARM) products introduced a small but significant possibility of systemic risk to the Danish mortgage system10. ARMs were first introduced in 1996, but and are just one of several innovations that were introduced to the Danish market.

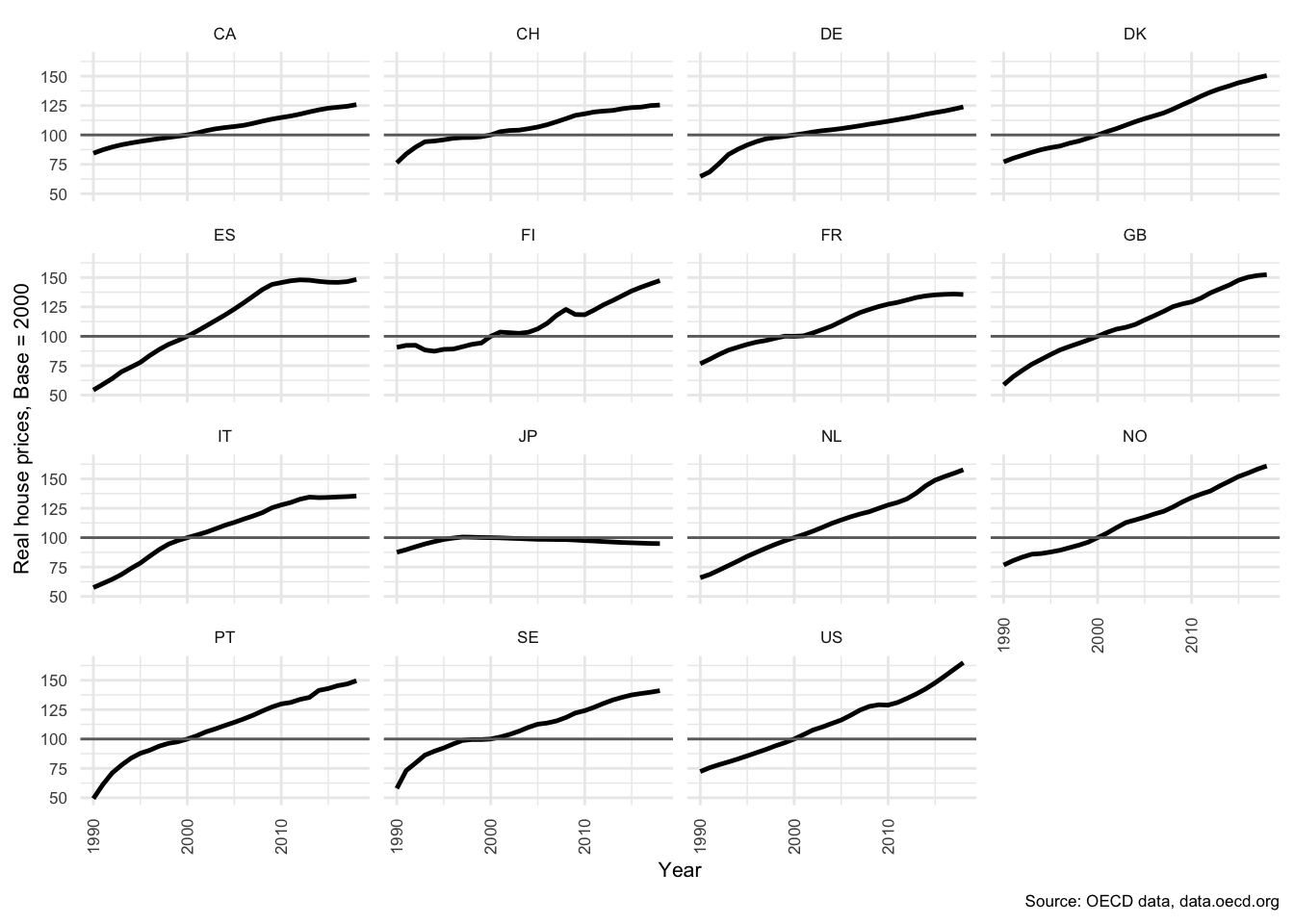

Affordability of housing also became a prominent issue and tax incentives for interest payments on mortgages were common. According to Scanlon, Lunde, and Whitehead (2011), real house prices in Denmark fell 14.9% from the peak in 2007 to Q4 2008. House prices rose in all OECD countries from 2000 to 200711, with Slovakia (22.41% year-on-year (yoy)), Ireland (16.65% yoy), Estonia (15.89% yoy), Hungary (13.52% yoy) and Latvia (11.22% yoy) as the most extreme examples, while Denmark rose at 3.11% yoy. From 2007 to 2009, house prices stabilised in most countries, and collapsed in a few with Estonia (-17.06% yoy) and Ireland (-12.57% yoy) showing the largest collapses. As noted above, Danish house prices reached a trough in Q4 2008 at -14.9%.

The asset and property price bubbles and collapses of recent years appear therefore to be closely related to developments in credit markets, and as is briefly explained below, the over-extension of private balance sheets and the risk of significant declines in property prices (the bursting of a bubble) could have serious consequences for both individual borrowers and the broader economy. Some of the key credit market innovations that occurred are discussed in the next section, together with some of their main advantages and disadvantages.

3.2.4 Key innovations and developments in product scope

Amongst the most common innovations noted by Scanlon, Lunde, and Whitehead (2008) included the following. The introduction of flexible-interest rates, and a variety of length of interest rate fixation periods. The introduction of interest-only periods, where repayment of capital or principal are postponed temporarily. Full term interest-only loans, with the principal payable on maturity - these are sometimes linked to investment vehicles designed to accumulate greater capital than the amount contributed (i.e. with an expected positive spread above the rate of interest). Longer terms of debt, some up to 50 years. Reduced up-front cash (or own) contribution requirements. Increased percentages allowed to be allocated to bond financing, typically at a significantly lower interest rate than would otherwise be available from a bank. Exceptionally low interest rate levels have also seen some innovations in terms of price. Zero-interest 20 year fixed-rate loans as well as negative interest rate flexible-rate (ARM) bonds are at the time of writing available in the Danish market.

Some of the key drivers of these innovations were, as noted by Alpanda and Zubairy (2017), the availability of new technology, which permitted significantly more complex products to be managed effectively. Government deregulation, and the associated greater market orientation. Rising asset prices and problems with housing affordability. In the post-crisis period, innovations have been driven by some additional factors, including record low interest rates and quantitative easing. Interest rates in developed economies, particularly northern Europe, have been set to record low levels. This has had the dual impact of reducing the cost of borrowing and significantly reducing lender revenues.

3.2.4.1 Advantages of innovations

The advantages of these innovations have been felt most by borrowers, particularly those groups of borrowers that were previously unable to afford initial payments on home loans (Scanlon, Lunde, and Whitehead 2008). As mentioned above, mortgage repayments are in many countries now more affordable in the short term. The flexibility of repayment options has made it possible for borrowers to structure their mortgages according to their expected cash flow requirements, this is especially helpful for borrowers with irregular incomes.

The introduction of interest-only periods, allow borrowers that have limited capacity to change their income levels, particularly the elderly, to maintain a stable standard of living (Scanlon, Lunde, and Whitehead 2008) - in effect consuming part of their home equity without the need to liquidate the asset. Interest-only periods also allow younger families to absorb temporary increases in living costs, without necessitating the sale of the family home. For example the cost of children, education, or other foreseeable and unforeseeable expenses.

The lengthening of the term of mortgage debts also reduces payments for the full term of the debt, making housing more accessible to groups that would otherwise not have been able to afford it. More sophisticated investors also have the opportunity to benefit from the innovations, where in very low interest environments, they might be able to borrow and invest at higher rates of return than the cost of borrowing. Unfortunately these advantages come with a cost.

3.2.4.2 Disadvantages of innovations

The disadvantages described below are considered as compared with a standard fixed-rate annuity mortgage. In general, the innovations in mortgages place significantly greater onus on the borrower to fully understand the product that they choose to take. Several of the benefits described above are also only true for the initial stages of the debt contract, as principal repayment is often built into later stages. These products also introduce additional risk in several forms, including interest rate risk, credit risk, market risk and significant potential opportunity costs - each will be discussed briefly below.

Interest rate risk Perhaps the simplest and most direct effect, which would not be felt by a fix interest rate borrower, is that flexibility of interest rates expose the borrower to future increases in interest expenses, and therefore negative effects to disposable income if interest rates rise.

Credit risk Interest-only periods may reduce monthly outlays, but they also prevent the accumulation of equity by the borrower. This means that there is less of a buffer, making them more sensitive to negative shocks. Negative shocks may include an increase interest rates, the loss of income, illness of self or family members, breakdown of relationships (possibly divorce) or a fall in property prices.

Market risk Borrower solvency is determined on the basis of outstanding debt relative to the value of the property held as collateral, or loan-to-value (LTV) ratio. In the case of property price declines, traditional borrowers would have built a buffer to absorb a decline in collateral value. By contrast, the lack of equity accumulation for interest-only borrowers means that the outstanding debt would not have fallen relative to collateral. Any borrowers with LTVs close to the limit would risk falling into negative equity, and possibly insolvency. Scanlon, Lunde, and Whitehead (2011) found that the groups that were most likely to be negatively affected in a crisis were those who had withdrawn equity (potentially via refinancing), or those who had bought close to the top of the market - resulting in high loan-to-value ratios and increased probability of falling into negative equity.

Opportunity cost Taking Denmark as an example, the borrower is endowed with several rights, one of which is that any mortgage bond is callable at any time, and at which time, the borrow can choose to either pay the remaining par value of debt, or to repurchase the same (or similar) bond sold at time of borrowing. What this means is that if interest rates rise after the date of borrowing, there is an opportunity for mortgage borrowers to settle their debt at a significantly reduced capital value. This reduction of debt can also be accomplished by refinancing at a later stage if interest rates were to rise sufficiently to outweigh the costs of refinancing. Borrowers with flexible rate mortgages lose this opportunity, since interest rates on flexible rate bonds are reset more frequently basis, and thus price adjustments are negligible.

In summary, the increased complexity introduced by innovations requires the borrower to have a more sophisticated knowledge of financial matters and to take on more responsibility for the security of collateral and repayment of capital. As has been reported by Scanlon, Lunde, and Whitehead (2008), it is doubtful whether most borrowers are sufficiently equipped to deal with these challenges. Where they do not have sufficient knowledge or skill, households become dependent on financial advisers and service providers to ensure that they have the most appropriate products.

The credit-asset-price virtuous cycle The self-reinforcing cycle of ease in credit markets and growth in asset prices is well documented. B. S. Bernanke, Gertler, and Gilchrist (1999) and Disyatat (2011) explained this in the context of the financial accelerator, rising property, and asset prices more generally, incentivise borrowing via balance sheet improvements and positive sentiment. In some cases borrowing is speculative, in order to benefit from the rising tide. Low interest rates and greater ease of access to mortgage debt simultaneously increase the pool of participants that demand assets, driving prices progressively higher. This virtuous cycle is mirrored by a similar decline in property prices and availability of credit on the way down. Conditions in credit markets and asset prices are thus difficult to separate.

3.3 Mortgage credit in Denmark

As mentioned above, the Danish mortgage lending market has also experienced a number of the innovations, and is a particularly interesting case due to a relatively unique approach to mortgage lending. The system is characterised by what is called the balance principle, which Laustsen (2009) describes as a traditional fund matching principle for mortgage lending. Denmark is unique in that this traditional principle has been respected for over 200 years. As noted by Laustsen (2009, 1), it results in “Transparent pricing in the form of a direct transfer of market-based prices to the individual borrower and market-based prepayment terms. And to the issuer: Limited and transparent risks.”12 As noted by Haldrup (2017, 2), a mortgage deed in Denmark is a “money-creating debt contract,” but in Denmark, this is financed from the existing money stock13.

These stable mortgage lending and covered bond markets have, since 1996, experienced a number of product14, operational15 and legislative16 innovations. The IMF (Sheehy 2014) conducted an assessment of the risk related to the structure of mortgage debt in Denmark in 2014, and found that there was a strong shift after 2003 towards flexible rate mortgages. This strong shift was warned against, and the financial supervisory authority, in collaboration with banks, began to reduce the exposure of HH to flexible rate products. While the problem was recognised, the level of flexible rate mortgage bond exposure remains high, with roughly 70% of outstanding mortgage debt to be repriced within the next five years. As in most other countries, the rights and protections of the borrower have been enhanced by several additional legislative changes17, several of which have been implemented in order to keep up with the rapid innovations in mortgage markets described above.

3.3.0.1 Composition of Danish mortgage debt

The composition of Danish real estate debt is rather complex to measure in its entirety, as there is a strong possibility that first-time home buyers will take an additional bank loan against their physical property for approximately 15% of the market value. In the data below, this portion of the debt is not included, and thus, the total debt outstanding represents a somewhat lower total than that official measures of total household debt used in the model that follows18.

The following data are constructed from administrative registers, which allows for a more granular view of recent developments than is typically available. The actual data are significantly more detailed than that presented here, but further disaggregation makes visual comparison difficult due to the relative (in)significance of some subcategories of debt. The two main dimensions on which we are interested in splitting mortgage debt are the term remaining on the debt and the length of time for which the interest rate is fixed (referred to as ‘interest fixation’ below). The interest fixation for ARM products shortened dramatically leading up to 2007, but has lengthened somewhat since the crisis, Unfortunately, the detailed micro-data is only available after 2009, which means that details during the expansion of mortgage debt are not available.

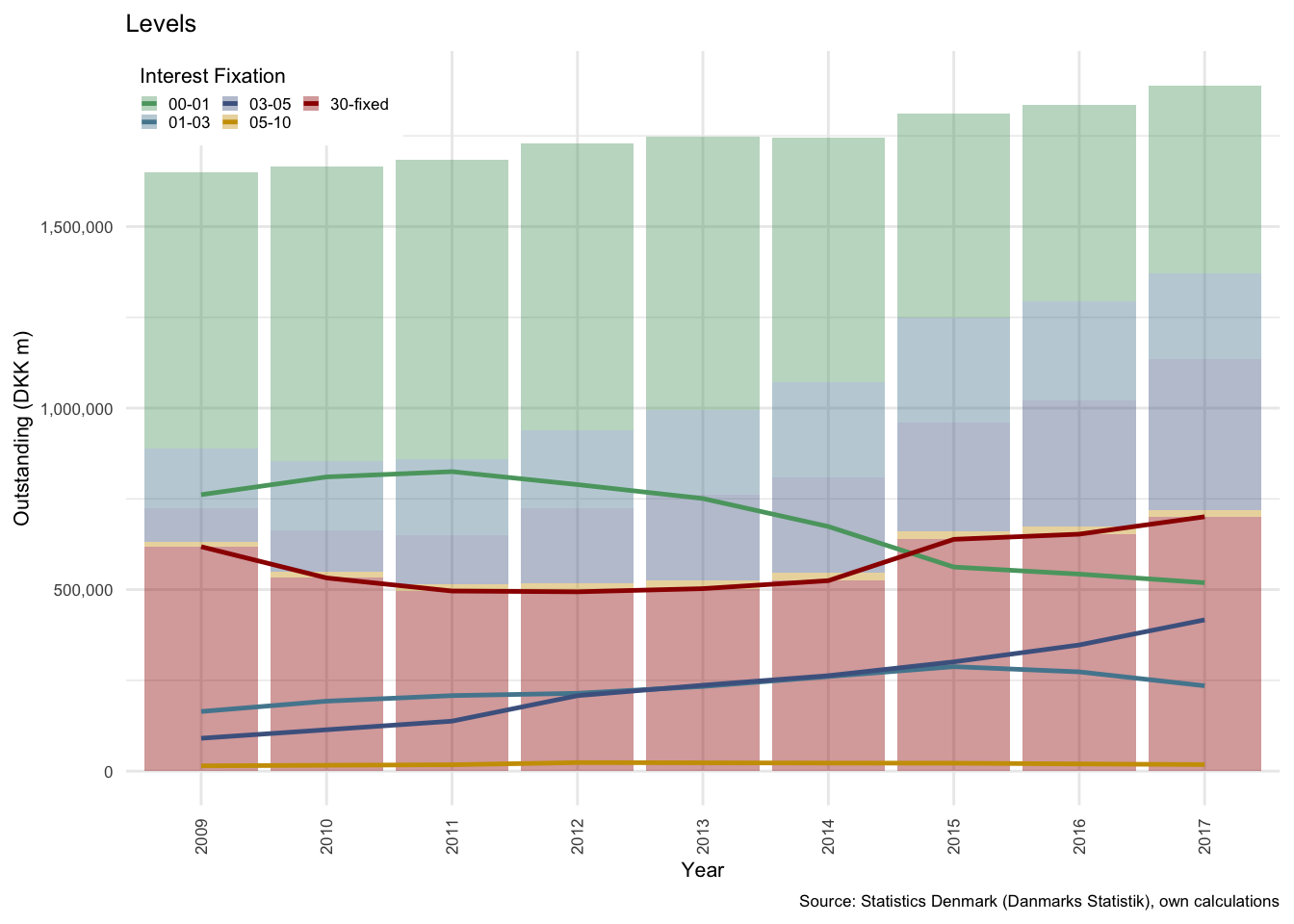

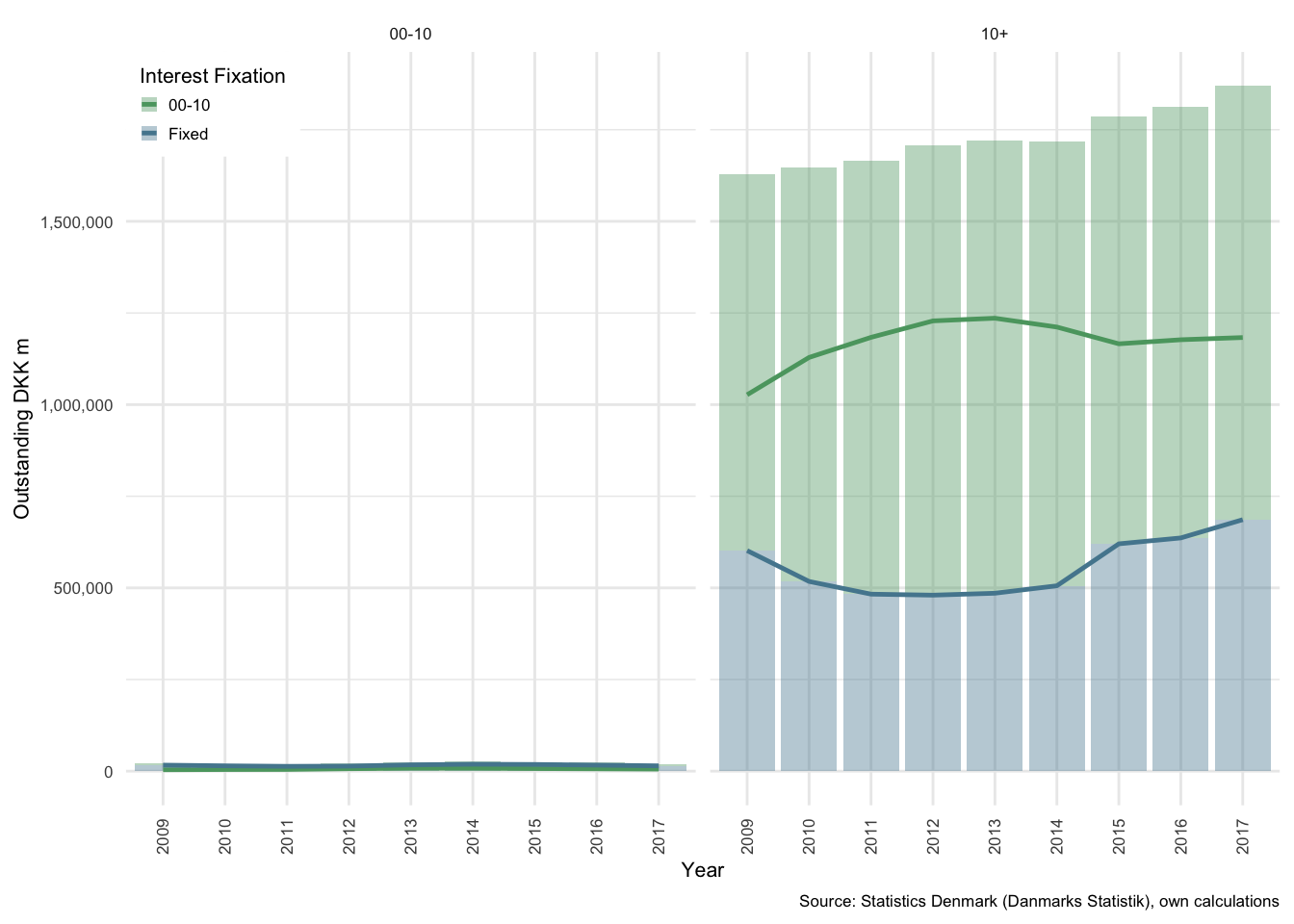

At a national level, the total level of debt split by interest fixation, can be seen in Figure . The first thing to note is that the nominal level of mortgage debt, in panel (a), has continued to rise throughout the period from 2009 through 2017.

Figure 3.1: Mortgage debt in Denmark: All term lengths

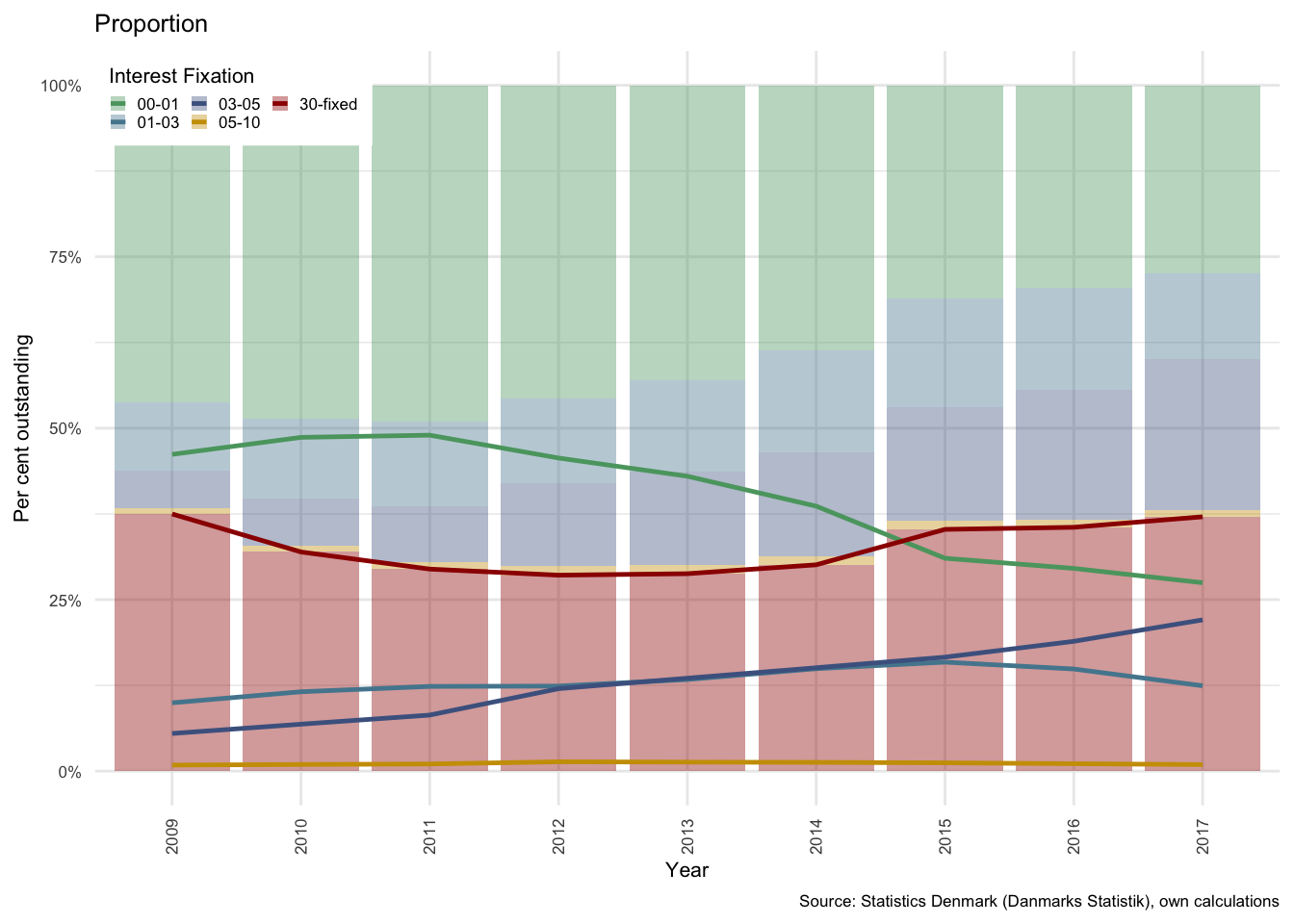

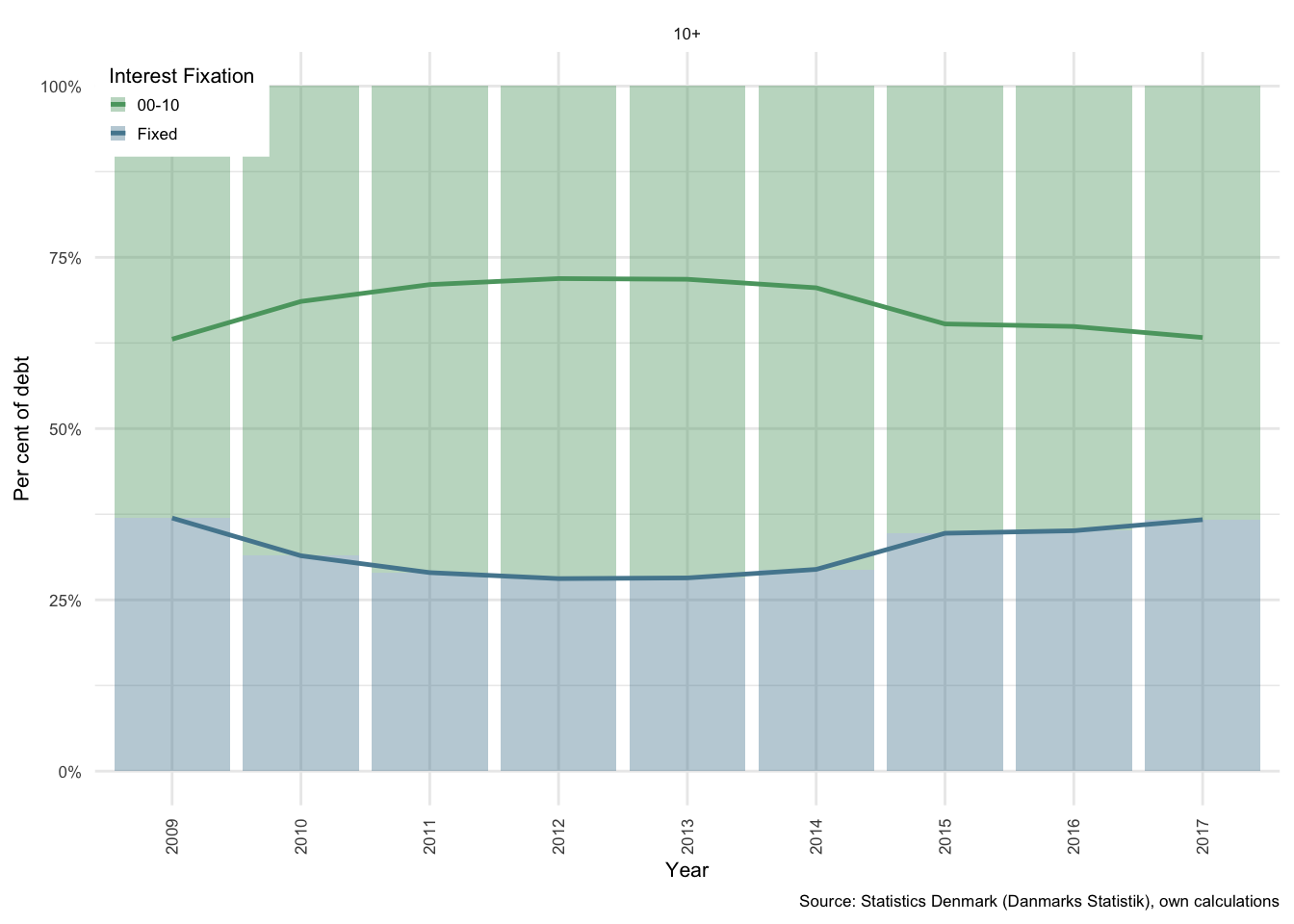

This can also be considered in proportional terms, where the percentage of debt outstanding in each category is easier to read. As can be seen in Figure part (b) above, the 30-fixed category, which covers all fixed rate products19, was still in decline as a proportion of total outstanding mortgage debt from 2009 to 2012.

The most concerning factor, and one raised by Sheehy (2014), in an IMF stability report, was the growing proportion of debt that would reprice within relatively short intervals. At the start of 2011, debt with an interest fixation of less than and up to 1 year (the green line) was by far the largest contributor. This was recognised by both domestic and foreign prudential regulators as a risky development, and in collaboration with the banking sector and real estate finance companies a variety of measures were implemented to reverse this trajectory. (Sheehy 2014)

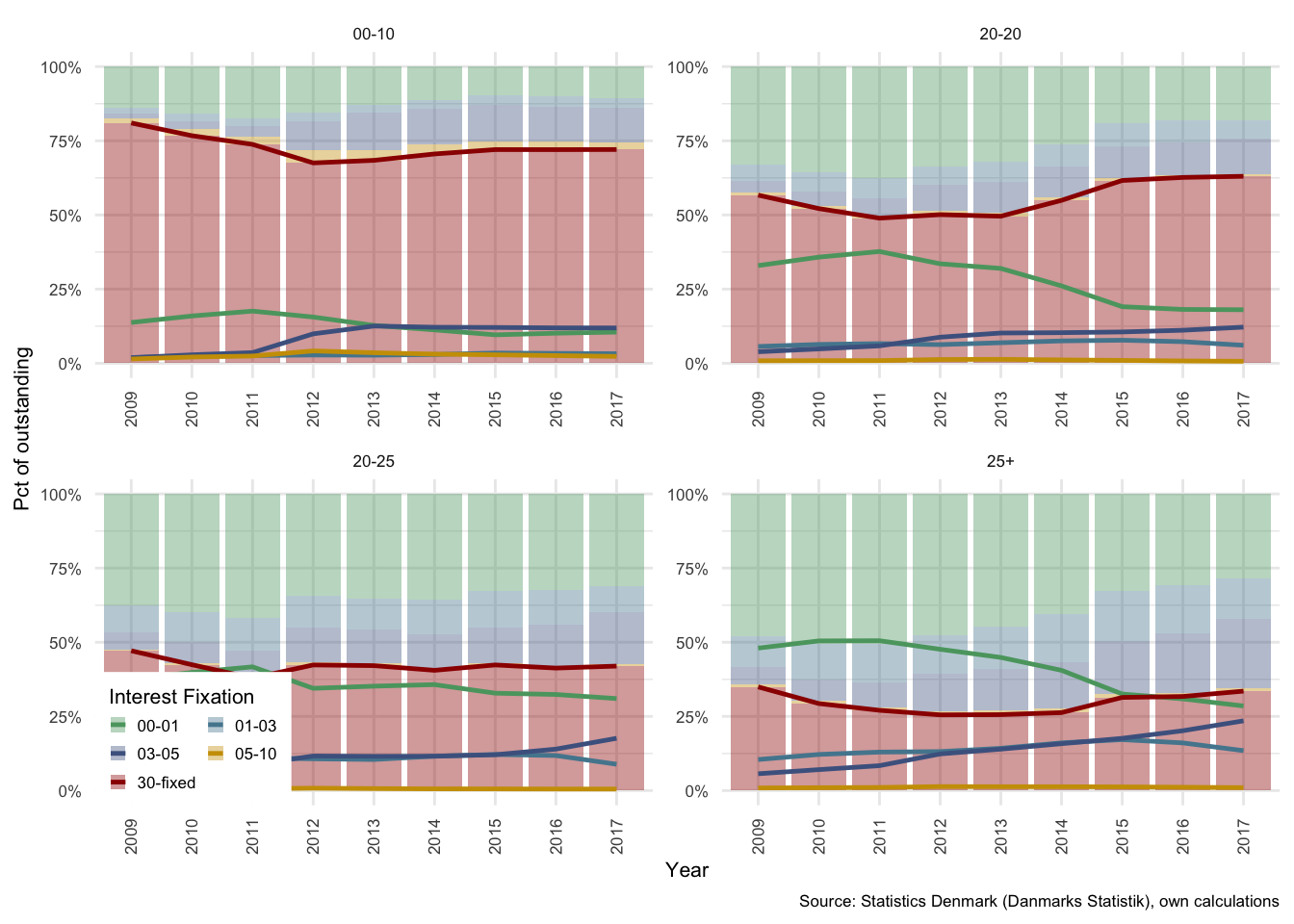

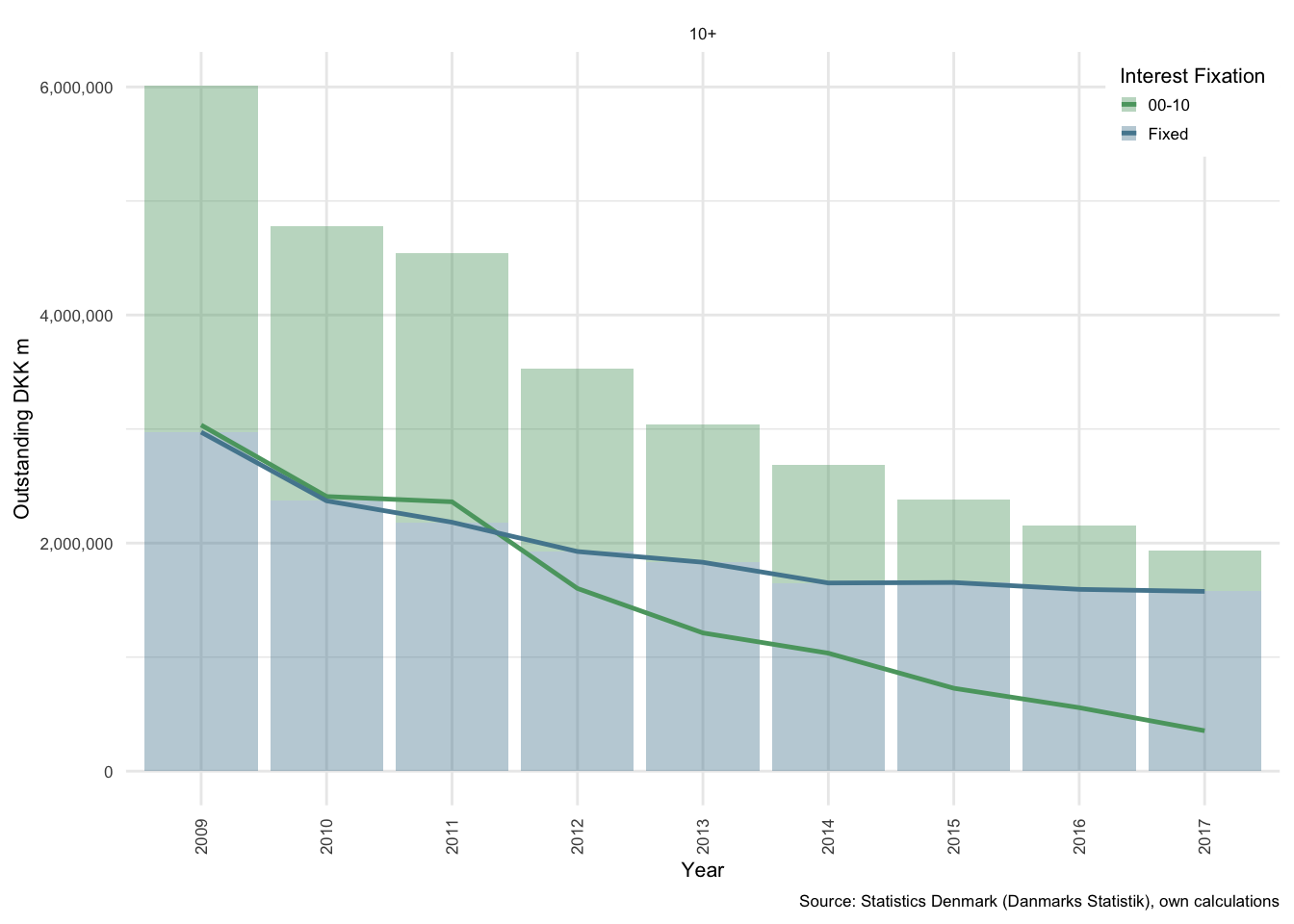

These patterns can further be decomposed into a variety of term structures. As can be seen from Figure , the proportional composition of debt is significantly different for each of the term groupings20. We will not explore this too deeply, as the relative importance of each category varies dramatically.

Figure 3.2: Composition of mortgage debt in Denmark: Split by term

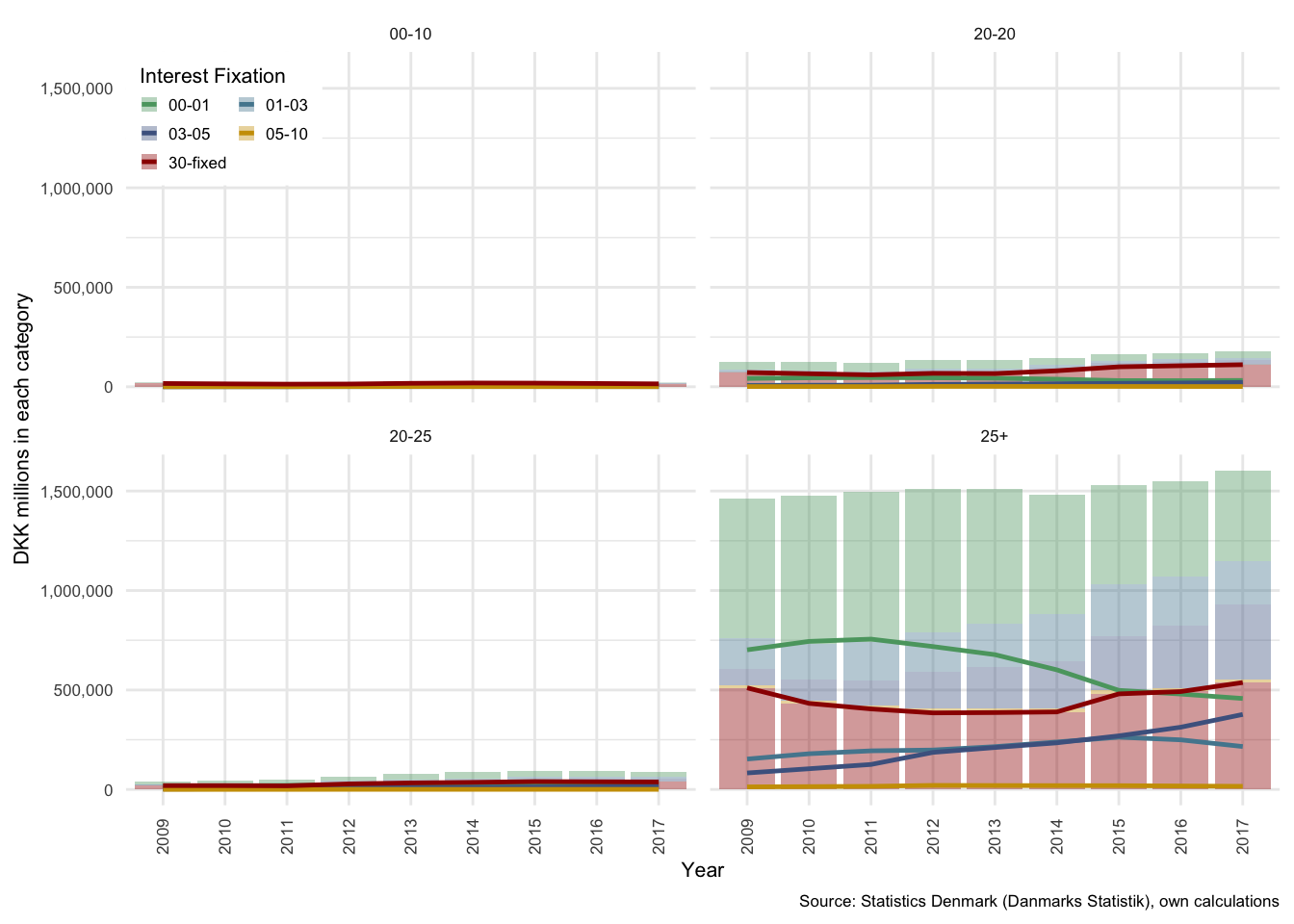

Figure illustrates the total outstanding debt in each of the term categories, it can quite easily be seen that by far the largest portion of debt has a term to maturity of over 25 years. In Denmark, the maximum term for which mortgage debt can be acquired is 30 years, thus all debt in this category in each year was issued under five years prior to the year in question. Roughly only one sixth of all outstanding mortgage debt has a term to maturity of less than 25 years.

Of the debt with greater than 25 years to maturity, it can be seen from Figure , that only approximately 30% of this outstanding debt has an interest fixation period of longer than 5 years. This together with approximately half of the other 15% results in a total of just over 37% of all outstanding mortgage bond debt. This means that the remaining 63% of mortgage debt will adjust together with interest rates. The outstanding mortgage bonds will also adjust in price, which effectively means that in the event of an increase in interest rates, nominal debt outstanding will remain fairly constant for the 63% that has flexible interest products, and debt service costs will rise commensurate with the rise in rates. The aggregate opportunity cost related to capital adjustments for borrowers in this case is potentially very large.

By 2017, the proportion of debt with an interest fixation period of 1 year or less had fallen to approximately 25% of all outstanding debt. A significant improvement from just under 50% for 2010 and 2011.

Figure 3.3: Levels of mortgage debt in Denmark: Split by term

Based on the distribution that can be seen in Figure above, the remainder of the paper uses a much simpler term and interest fixation categorisation. In order to capture all long term debt, all outstanding debt with a term longer than 10 years is included in long term debt, while all shorter terms maturity are included in the short term category. Similarly, interest fixation periods of less than 10 years are included in the short fixation period category, of which the overwhelming majority is fixed for less than five years. All interest fixation periods of longer than 10 years are included in the fixed-interest category. Because the level of mortgage debt with a shorter term is so low (largely irrelevant), this additional categorisation is dropped. Any shorter term mortgage debt is also likely to have similar characteristics of longer term debt that has short interest fixation periods. As such, it is assumed that the only fixed interest debt held by HH is held in the form of mortgage debt. It is therefore possible to categorise all debt in terms of the “interest fixation” dimension.

This is supported by Figure , where the proportion of debt in the shorter term category is essentially negligible in comparison with the longer term outstanding portion.

Figure 3.4: Composition of mortgage debt in Denmark: Simplified, panels by term

Figure shows the nominal outstanding amounts in the short and long term to maturity categories. As can noted above, the short-term-to-maturity debt to the left is of negligible interest for the analysis that follows, and so most of the figures below focus purely on the long term-to-maturity (10+ category) to the right.

Figure , part (a), reflects the relative proportions of fixed and flexible-interest fixation periods in each interest fixation category. The debt with interest-fixation periods of less than 10 years will be referred to as adjustable rate mortgages (ARMs) or flexible-rate mortgages below.

Figure 3.5: Outstanding mortgage debt and interest payments: Term of 10+ years

Figure 3.6: Interest payments

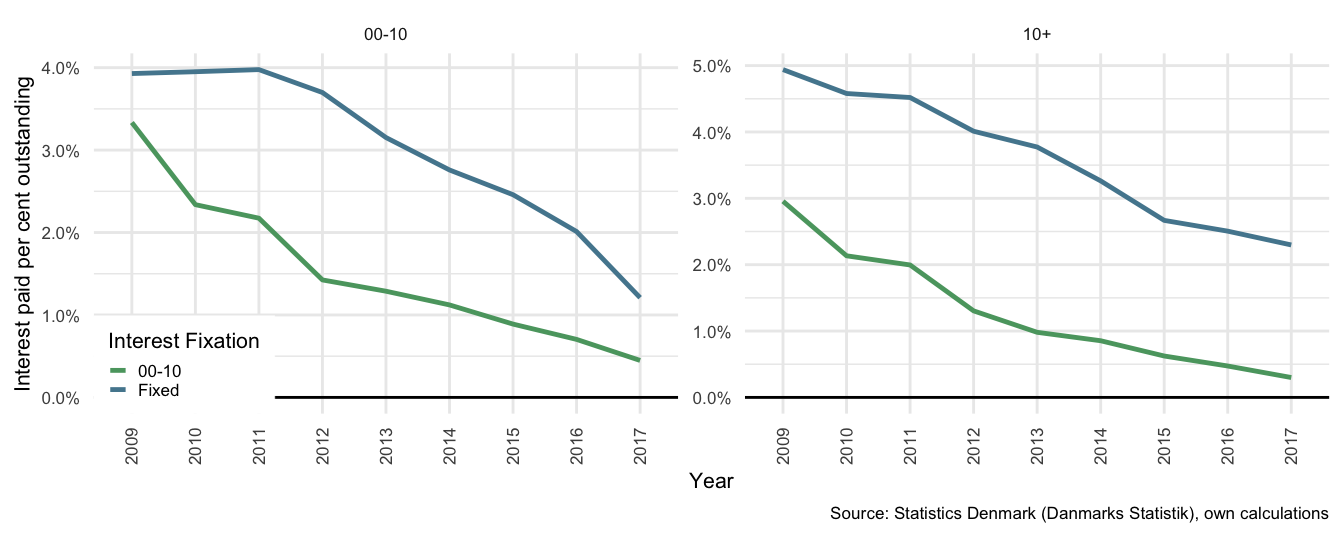

The cost of the outstanding debt has not followed the same pattern. Figure part (b) above, shows that the total interest expenses paid on shorter ARM debt has declined in nominal terms from roughly equivalent to the fixed-interest debt in 2011 to just a fraction of total interest paid on fixed-interest products by the end of 2017.

This can then be represented as an average rate of interest by calculating the amount paid divided by the total outstanding debt. In Figure , the short-term-to-maturity characteristics are shown on the left to illustrate the these products follow market rates more closely. Again, however, it is the panel to the right that we are most interested in, where it is possible to see that longer term ARM debt paid an average rate of just under 0.5%, while fixed rate longer term debt paid on average approximately 2.4% in 2017. The spread has interestingly remained relatively constant between the two average rates, but the proportional decline in the ARM average rate has been approximately -86%, while the same for fixed rate products has been approximately -50%. It appears, from this illustration, that a fall in official interest rates has passed through to mortgage markets at roughly the same speed in fixed and ARM products21.

Figure 3.7: Interest paid per cent of mortgage debt outstanding: By term

As can be expected, in the Danish environment, as interest rates fall and the option to refinance remains available to households, the rate of interest on fixed-interest securities has followed the flexible rate of interest downwards - with a relatively constant spread of approximately 2% points. Unfortunately we do not have data on how this spread alters during a rising interest rate period. It can be seen that there was some delay in convergence in shorter terms to maturity. This is expected as the costs associated with refinancing existing contracts are likely to outweigh the benefits of a reduction in interest expense on smaller capital values, or on products with shorter terms to maturity (i.e. fewer interest payments remaining).

In a rising rate environment borrowers again have the incentive to refinance in order to take advantage of falling bond prices, since in Denmark the borrower has the option to either pay back the cash capital value or to repurchase an equivalent bond to the one issued on the date of borrowing (otherwise known as a prepayment or buy-back option). If interest rates rise sufficiently to make it profitable, and if they have accumulated sufficient equity, the borrower has the opportunity to make a substantial reduction in the outstanding capital amount. Thus, unless rates remain unchanged, or only vary marginally, for an extended period of time, the proportion of outstanding debt that has been recently refinanced will typically be quite high22.

3.3.0.2 Affordability of debt

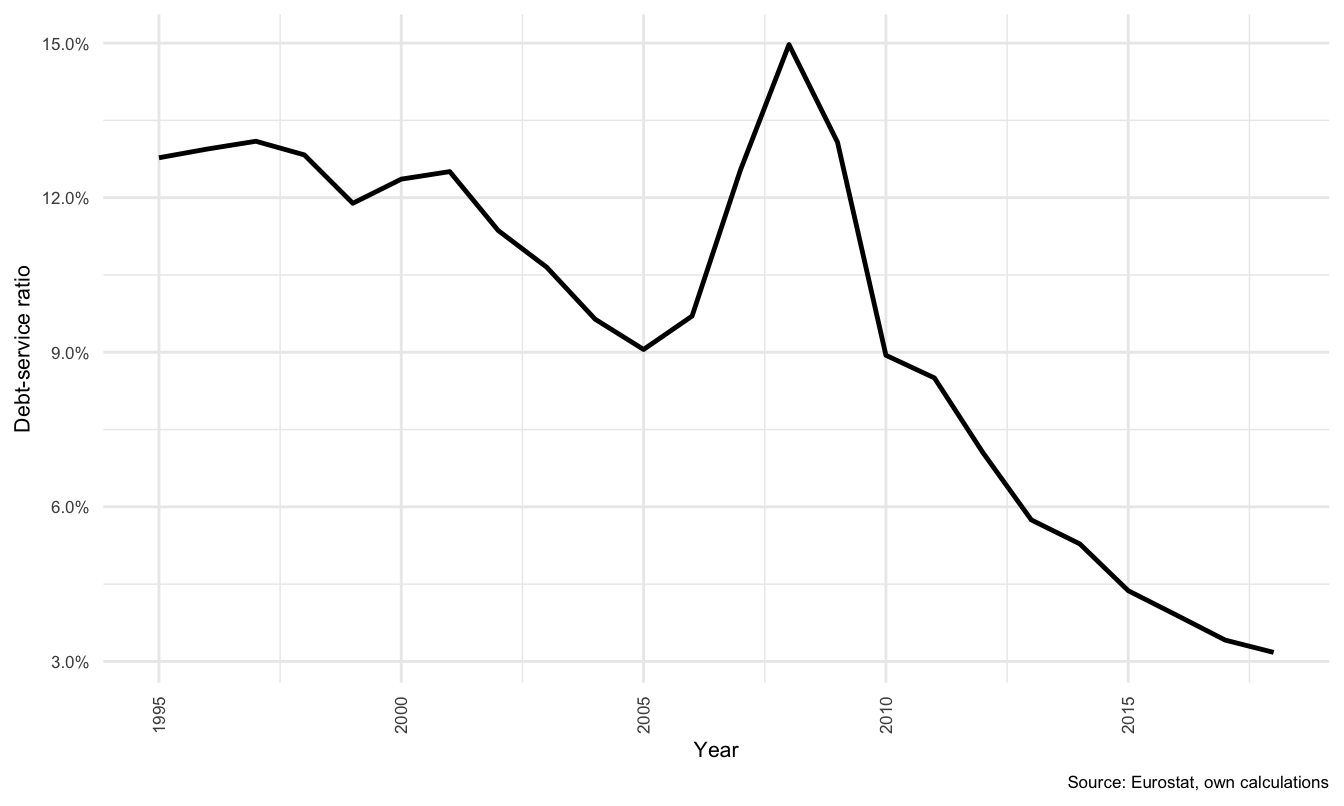

The debt-service ratio (DSR) is shown in Figure , and calculated as the ratio between total outgoing property income payments to annual HH disposable income. In aggregate terms, it is unsurprising that the DSR has fallen continuously for the Danish household sector since the GFC. It is presently at the lowest level since 1995, and according to data collated by Abildgren (2017), the lowest level ever. Thus in relative terms, while debt may be at record high levels relative to income, the aggregate cost of servicing that debt is at an all time low.

Figure 3.8: Debt-service ratio: Denmark

This paradox between the level of debt outstanding and the declining DSR is discussed in analysis in Section The implications for the economy as a whole and for the household sector depend on the macroeconomic linkages between the sectors and the drivers of agent decision-making in the model structure.

3.4 The model

The model implemented in this section is based on Byrialsen and Raza (2019), which is at the time of writing the most advanced empirical Stock-Flow-Consistent (SFC) macroeconomic model of Denmark. The full model together with an explanation for each equation and the logical connections between each of the sectors, flows and stocks is provided in Section , in the appendix.

Throughout this section some of the equations and explanations thereof are duplicated for explanatory purposes. It will provide only a brief summary of the core features of the model, and the highlight the main changes made for this analysis.

The model consists of the five main institutional sectors, namely the household sector (HH) non-financial corporate sector (NFC), the financial corporate sector (FC), the general government (G), and the rest of the world (ROW). It was developed between 2017 and 2019 with a focus on the Danish HH. As such, the behaviours of all sectors are significantly simplified, except in so far as they engage directly with HH. The model is fully empirical, in the sense that all variables included in the model are available as a dataset, against which the performance of the model can be tested.

One feature is worth noting up front. As mentioned in the introduction, the full model has 131 endogenous and 78 exogenous variables. Included in the exogenous variables are all rates of return and all financial asset prices. The most important implication is that correlated asset price and market movements are not endogenous in the model, and this limits the analysis to very short-term model responses.

3.4.1 Data

The data used for the model in this article is sourced from a combination of Eurostat data, OECD data, and AMECO data. The period for which annual data is available in sufficient detail is from 1995 to 2017. This data is then processed in a series of aggregations. The data and the model accounting structures follow the ESA 2010 (Statistical Office of the European Communities. 2013) accounting structure, and the contents of the financial balance sheet can be summarised as:

Monetary gold and special drawing rights (F1), Currency and deposits (F2), Debt securities (F3), Loans (F4), Equity and investment fund shares (F5), Insurance, pensions and standardized guarantee schemes (F6), Financial derivatives and employees stock options (F7) and Other accounts (F8). These data are aggregated according to Table .

| Interest bearing (\(IB\)) | \(F_1\), \(F_2\), \(F_3\), \(F_4\), \(F_7\) or \(F_8\) |

| Net interest bearing (\(NIB\)) | \(F_1\), \(F_2\), \(F_3\), \(F_4\), \(F_7\) or \(F_8\) |

| Net equities (\(NEQ\)) | \(F_5\) |

| Pension (\(PEN\)) | \(F_6\) |

The financial markets are thus highly aggregated in the model with effectively only three asset classes. \(IB\) covers all securities that provide a financial return that is analogous to interest, as does \(NIB\). The only difference is that for NFC, GOV and ROW, as part of the aggregation process, only the net position in these assets and liabilities are considered.

The other two major asset classes are equities and pension funds. All except HH equities are expressed as net equity assets and liabilities, \(NEQ\), and for HH they are expressed as equity assets, \(EQA\), as they cannot issue equity liabilities by definition. Pension assets are expressed as \(PEN\), and are recorded as net pension assets (\(NPEN\)) for ROW.

3.4.2 Major changes

The most significant change in this version of the model is the introduction of a split between fixed and flexible rate mortgage debt. This relatively simple alteration allows one to test the sensitivity of HH balance sheets to a change in debt composition. The drivers of debt remain the same, and the rates of return on all other assets have been left unchanged.

This is to isolate the channel through which the change in the cost of borrowing affects households in the short term. This makes it possible to identify the transmission channels and magnitude of each shock more clearly. It is one of the advantages of fully exogenous rates of return and asset prices, but comes at the cost of more realistic inter-market (“pass-through”) responses.

3.4.3 Balance sheet and transactions flow matrices

As with all SFC models, the balance sheet matrix represents the distribution of ownership of assets (\(+\)) and liabilities (\(-\)) in the modelled economy. As can be seen from Table , the sum of all rows, with the exception of fixed capital, are zero. This reflects that each asset (except fixed assets, \(K\)) is exactly offset by a liability held by another sector.

The financial asset classes mentioned above are assigned to each sector according to assumptions of which sector issues or holds each type of security. FC holds the majority of counterpart financial securities, and in all sectors except HH, financial assets and liabilities are recorded in net terms (assets minus liabilities).

The interest bearing liabilities of HH are, as noted in the previous section, by a vast majority, long term debt. This is separated into fixed-interest (\(IBL(FI)^F\)) and flexible-interest (\(IBL(FL)^F\)) (or, ARM) mortgage liabilities.

Horizontal consistency captures the idea that all accounts are recorded as dual entry accounting records, and the sum of all sector positions in any financial asset class should be zero. Vertical consistency represents the financial position of each sector, where financial net wealth (\(FNW\)) is the sum of all assets and liabilities and will either be a net positive or negative value. The sum across sectors of the \(FNW\) of all sectors is also zero.

| Financial Stocks | ||||||||

| Interest bearing (IBA / IBL) | \(-IBL^{F}\) | \(+IBA^{H}\) | 0 | |||||

| Interest bearing Fixed | \(+IBA(FI)^{F}\) | \(-IBL(FI)^{H}\) | 0 | |||||

| Interest bearing Flexible | \(+IBA(FL)^{F}\) | \(-IBL(FL)^{H}\) | 0 | |||||

| Net interest bearing (NIB) | \(NIB^{N}\) | \(NIB^{F}\) | \(NIB^{G}\) | \(NIB^{W}\) | 0 | |||

| Net equities (NEQ) | \(NEQ^{N}\) | \(NEQ^{F}\) | \(NEQ^{H}\) | \(NEQ^{W}\) | 0 | |||

| Pensions (PEN) | \(-PEN^{F}\) | \(+PEN^{H}\) | \(NPEN^{W}\) | 0 | ||||

| Fixed Stocks | ||||||||

| Financial net wealth (FNW) | \(FNW^{N}\) | \(FNW^{F}\) | \(FNW^{G}\) | \(FNW^{H}\) | \(FNW^{W}\) | 0 | ||

| Fixed assets (K) | \(K^{N}\) | \(K^{F}\) | \(K^{G}\) | \(K^{H}\) | \(K^{T}\) | |||

The transactions flow matrix is presented below. This matrix, much like the balance sheet matrix presented above, observes the requirements of horizontal and vertical consistency. In this table, all items that result in a positive flow of funds for the sector in question are marked with a plus sign (\(+\)), and all those that result in a flow outwards of funds are marked with a minus sign (\(-\)).

The expenditure approach to GDP is captured in the first five lines of the table, and can be captured as,

\[\begin{equation} Y = C + I + G + (X - M) \label{eq:gdp_intext} \end{equation}\]

Where \(C\) is consumption, \(I\) is investment, \(G\) is government expenditure, \(X\) is exports and \(M\) is imports. All in nominal terms to reflect the actual flows of funds in each period. The income approach to national expenditure is captured in the following six lines in the table up until the row called Savings. Each row name reflects the flow that is applicable to each sector. The full detail of how these flows are defined can be found in the full model description in Section , in the appendix.

Capital income (\(rK\)), transfers (\(STR\)), capital transfers (\(KTR\)), acquisitions less disposal of fixed assets (\(NP\)) and net lending (\(NL\)) are presented without a particular sign attached to each sector. The reason for which is that each sector both receives and pays social transfers, and although GOV is the primary counterpart for all of these, the size and net sign of these transfers can change over time. The same is true for \(KTR\) and \(NP\). Net lending (\(NL\)) is a passive (residual) value and is determined by the balance of funding requirements between the sectors over time, and can therefore also swing between negative or positive as a flow.

| Private consumption | \(+C\) | \(-C\) | 0 | ||||||||

| Government consumption | \(+G\) | \(-G\) | 0 | ||||||||

| Investment | \(+I\) | \(-I^{N}\) | \(-I^{F}\) | \(-I^{G}\) | \(-I^{H}\) | 0 | |||||

| Exports | \(+X\) | \(-X\) | 0 | ||||||||

| Imports | \(-M\) | \(+M\) | 0 | ||||||||

| GDP | Y | 0 | |||||||||

| Taxes | \(-T^{N}\) | \(-T^{F}\) | \(+T^{G}\) | \(-T^{H}\) | \(-T^{W}\) | 0 | |||||

| Gross operating surplus | \(-B2^{N}\) | \(+B2^{F}\) | \(+B2^{G}\) | \(+B2^{H}\) | 0 | ||||||

| Wages | \(-WB^{N}\) | \(+WB^{H}\) | \(WB^{W}\) | 0 | |||||||

| Capital income | \(rK^{N}\) | \(rK^{F}\) | \(rK^{G}\) | \(rK^{H}\) | \(rK^{W}\) | 0 | |||||

| Transfers | \(STR^{N}\) | \(STR^{F}\) | \(STR^{G}\) | \(STR^{H}\) | \(STR^{W}\) | 0 | |||||

| Pension adjustments | \(-CPEN^{F}\) | \(+CPEN^{F}\) | 0 | ||||||||

| Savings (per sector) | \(-S{N}\) | \(+S{N}\) | \(-S{F}\) | \(+S{F}\) | \(-S{G}\) | \(+S{G}\) | \(-S{H}\) | \(+S{H}\) | \(-S{W}\) | \(+S{W}\) | 0 |

| Capital transfers | \(KTR^{N}\) | \(KTR^{F}\) | \(KTR^{G}\) | \(KTR^{H}\) | \(KTR^{W}\) | 0 | |||||

| Acquisitions less disposal FA | \(NP^{N}\) | \(NP^{F}\) | \(NP^{G}\) | \(NP^{H}\) | \(NP^{W}\) | 0 | |||||

| Net lending | \(NL^{N}\) | \(NL^{F}\) | \(NL^{G}\) | \(NL^{H}\) | \(NL^{W}\) | 0 | |||||

| \(\Sigma\) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

The three rows after the Savings row illustrate adjustments to the level of savings (\(S\)) as a result of capital transfers (\(KTR\)), purchase and sale of fixed assets (\(NP\)) and (from the third row of the table) the level of investment (\(I\)) of each sector - summed vertically in the capital accounts column for each sector. The sum of all of these items is reflected in a net financing requirement for each sector, in the table is called Net lending. The sum of all net lending positions in the economy is again necessarily equal to zero, as one sector’s surplus is at least one other sector’s deficit. The sum of all columns and all rows are thus all equal to zero, and this criterion is respected by the data collected from Eurostat on an annual basis.

Financial and fixed assets in the model are subject to both transactions and revaluations (or capital gains or losses). The accumulation of certain types of assets or liabilities depends in part on the action of the sector in question and in part on the effects of the other sectors. As can be read in the full model description in the appendix, the nominal values that are sourced from the Eurostat database and or AMECO can then be deflated using appropriate price indices. There are 19 different price indices used in the model, some of which are calculated, but the majority of which are sourced either from Statistics Denmark, AMECO or the OECD. The details of the model structure and the performance of the model relative to the data available can be found in Byrialsen and Raza (2019), and the details of the behavioural equations available in Section , in the appendix.

What we are most interested in here, however, is the specific channels through which the scenarios proposed below transmit. As mentioned above, the model contains active behaviours and passive behaviours. In each period, in order to ensure closure in the model, there is one variable in each sector that is passive to the budget constraints of each year.

The passive accumulator flows (or residual, buffer variables) for each sector are as follows: transactions in net interest bearing securities for NFC (\(NIBTR^N_t\)), GOV (\(NIBTR^G_t\)), and ROW (\(NIBTR^W_t\));and, transactions in interest bearing assets for HH (\(IBATR^H_t\)). While specific behavioural equations determine the holding of all other financial assets, \(NIB\) securities act as a catch all category for NFC, GOV and ROW. The sum of those positions is then absorbed by FC. As will be discussed below, the final closure of the model is provided through the indirect provision of equity assets to HH by FC on demand. This is fitting, since HH purchases of mutual funds or unit trusts are likely to be fulfilled by FC, rather than directly by NFC.

3.5 Scenarios

This section briefly explains the four scenarios investigated using the model. Apart from alterations to the structure of household mortgage liabilities, the model operates in the same manner as in Byrialsen and Raza (2019). The shocks presented below are measured as a percentage change from the baseline scenario. This allows for a simpler comparison between scenarios, and the aggregate nominal and real values of stocks and flows are illustrated where relevant.

The first shock (and Scenario 1) is an increase in interest rates in 2020, the second shock (and Scenario 2) is a decline in property prices in 2022. Scenario 3 compounds the first two, in that the first shock is kept in the model before the shock to property prices is imposed. The last scenario, Scenario 4, is a reduction in the level of ARMs in 2017. Effectively, the last scenario changes the pre-conditions for the first two shocks, but applies them in exactly the same manner. It is therefore possible to make a direct comparison between Scenario 3 and Scenario 4, given two different starting points.

This ordering allows the answer to a counter-factual question: What if HH had not taken on as much flexible rate mortgage debt? How would this shift in interest rate exposure affect outcomes, both for HH and the broader economy? In essence, what might have been the case if the innovations leading up to 2003 had not impacted borrowing decisions to the same degree? There are however, some limitations to the current model that are relevant for this exercise.

3.5.1 Limitations for interpretation of results

Adjustable Rate Mortgages (ARMs) typically do not adjust immediately

As noted above, the bulk of ARMs in Denmark adjust fewer than 5 years into the future. This allows households an extended period of time to observe interest rate fluctuations and make a decision regarding refinancing or property sale. It also means that the effects of an interest rate change will only impact HH cash flows after between one and five years.

A decline in house prices is unlikely to happen in isolation

A fall in house prices is not expected to occur in isolation. Unlike in the model below, a collapse in property prices is unlikely to be an isolated event. It would more likely accompany broader systemic problems or be triggered by some form of financial or economic crisis.

The structure of the economy at end 2017 is integrated with the volume and structure of household debt

For the fourth scenario, it is assumed that we can simply shift the structure of debt and leave the remainder of the economy unchanged. In reality, the total level of debt outstanding would probably be significantly lower if ARM and interest-only products had not been made available. This would have affected a significant array of economic variables, not least of all, domestic demand and house prices. Although this is true, HH have already accumulated significant levels of debt. As such, Scenario 4 is less a question of, what if things had been different, and more a question of how to structure policy in order to best influence future refinancing decisions of HH.

Interest rate changes would change the composition of debt

Refinancing in response to interest rate changes in Denmark is extensive. In a rising interest rate environment, the incentive is to repurchase the previously issued bond at a reduced price, settle the older debt, and then refinance at similar monthly instalments, but with a lower capital value outstanding.

With falling interest rates, the incentive is to refinance at lower monthly instalments, and if possible using a bond with fixed-interest, thus creating the opportunity to refinance if rates rise significantly in the future, and thus reduce the level of debt outstanding. It is therefore unlikely that the structure of debt would remain constant after a shift in rates23. Due to the costs involved in refinancing, a change in interest rates is expected impact debt structures gradually, remaining fairly stable for the first year or two, and adjusting to a greater degree in the medium term (approximately up to 5 years).

3.5.2 Scenario 1 - An increase in interest rates

The first shock is a simple interest rate change. The point is to illustrate the expected impact on the level of household disposable income and the household balance sheet.

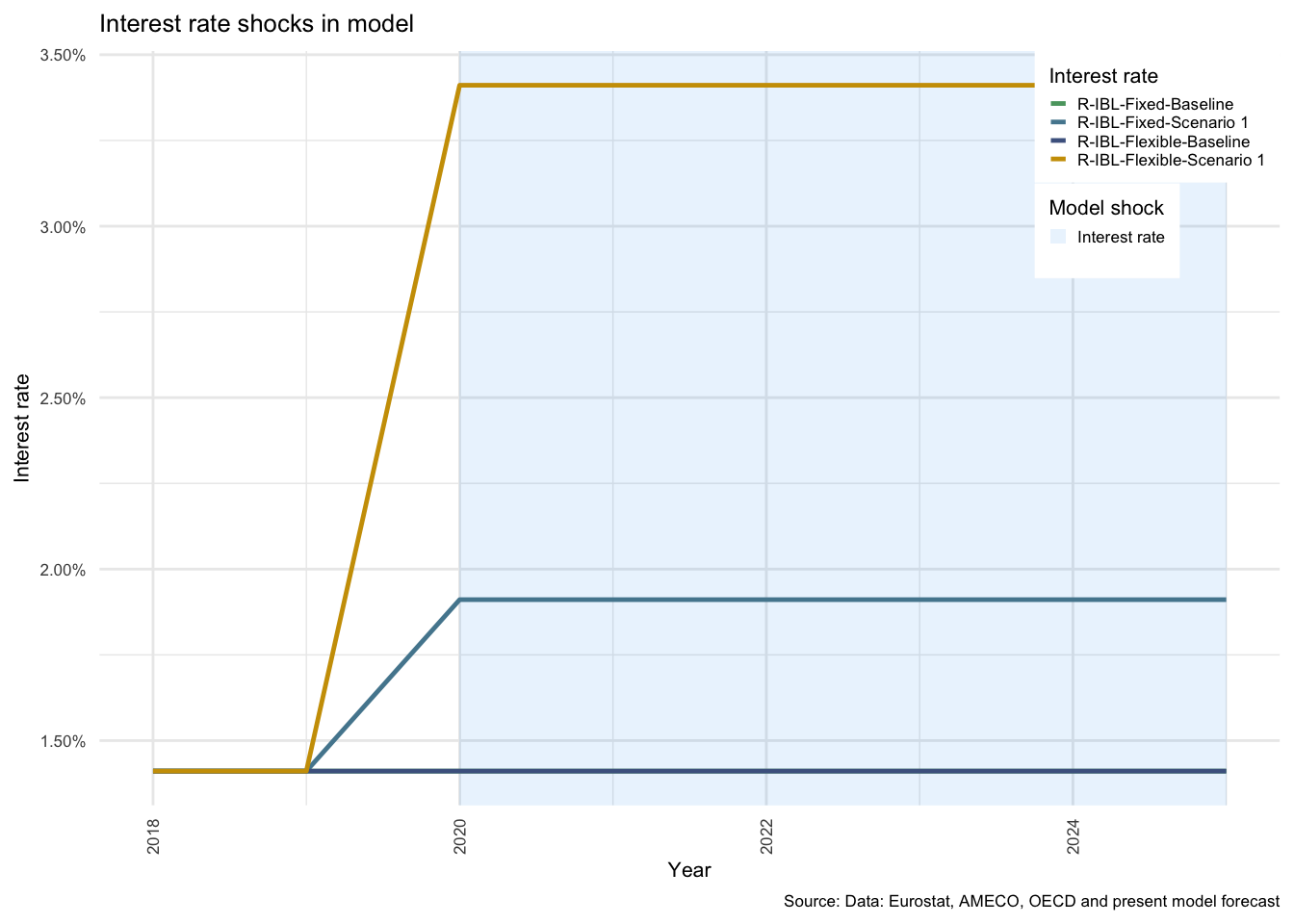

In this shock we consider a 2 percentage point (\(2\%\) points) rise in official rates. This is assumed to be passed through perfectly to ARM mortgages (interest rate on flexible-interest-rate mortgage debt, i.e. flexible rate products, with subscript (FL), (\(r^H_{L(FL)_{t}}\)). The cost of fixed-interest mortgage debt (\(r^H_{L(FI)_{t}}\)) is increased by a proportionally lower adjustment of point five percentage points (\(0.5\%\) points) to reflect lower sensitivity of adjustments of the overall stock of fixedinterest rate products. This is a strong assumption, and is not likely to hold over longer periods of time, fixed-interest rate debt holders are expected to retain their debt at lower interest rates, while the majority of flexible-interest rate holders are expected to participate fully in the rise in interest rates after a period of three years24.

In the model baseline, the current rate is calculated as interest payments relative to outstanding debts. This gives a weighted average at the end of 2017 of 1.41% for all debts25. After the shock, the adjustment is from this average rate upwards - thus flexible-interest rates are adjusted up to 2.41% and fixed-interest rates up to 1.91%. This constitutes a 141.75 per cent increase in flexible rates, and taking into account changes in the level of outstanding debt in 2021, a 136.29% increase in interest payments. For fixed-interest debt, it constitutes a 35.44 per cent increase in fixed rates, and a 32.38% increase in interest payments.

The interest rates in the model include, interest on fixed (\(r^H_{L(FI)}\)) and flexible rate (\(r^H_{L(FL)}\)) mortgages, and the counterpart assets (\(r^F_{A(FI)}\), \(r^F_{A(FL)}\)), the general rate of return on net interest bearing assets (\(r_{N}\)), and the return on interest bearing assets for households (\(r^H_{A}\)). The other rates of return are the domestic and foreign rate of return on equities (\(\chi _t\)), and pension assets (\(\psi _t\)). All rates of return in the model are determined exogenously, which means that any adjustment must be applied manually. As noted above, the change is limited to the cost of borrowing for HH only.

In the case of household debt, it is FC that holds the counter-balance assets. Thus,

\[r^F_{A(FI)_{t}} = r^H_{L(FI)_{t}}\] and, \[r^F_{A(FL)_{t}} = r^H_{L(FL)_{t}}\]

FC receives \(r^F_{A(FI)_{t-1}}(IBA^{F\sim H}_{A(FI)_{t-1}})\), and the two interest rates are simply made equivalent. An increase in rates results in an increase in costs for HH and an increase in revenues for FC.

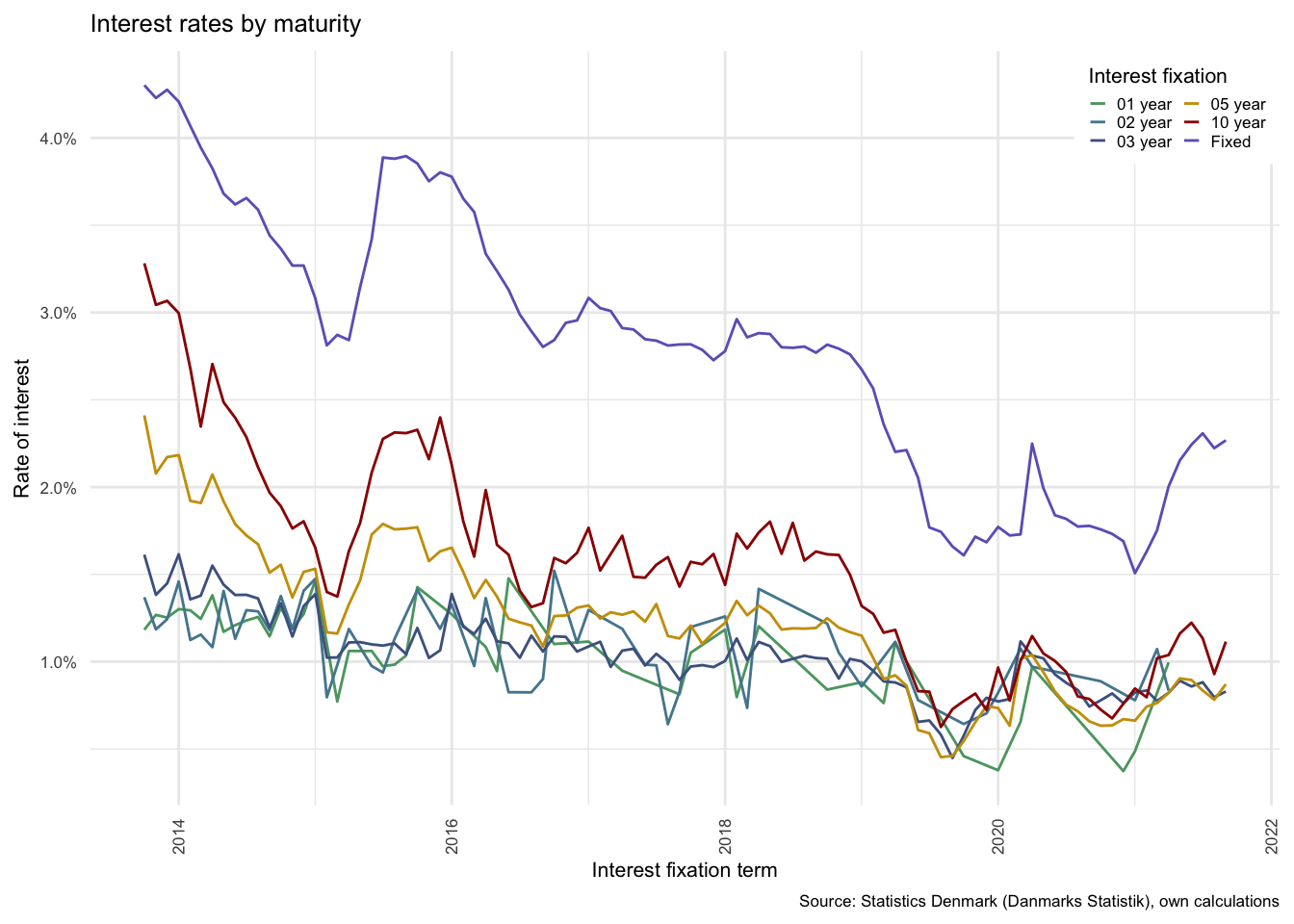

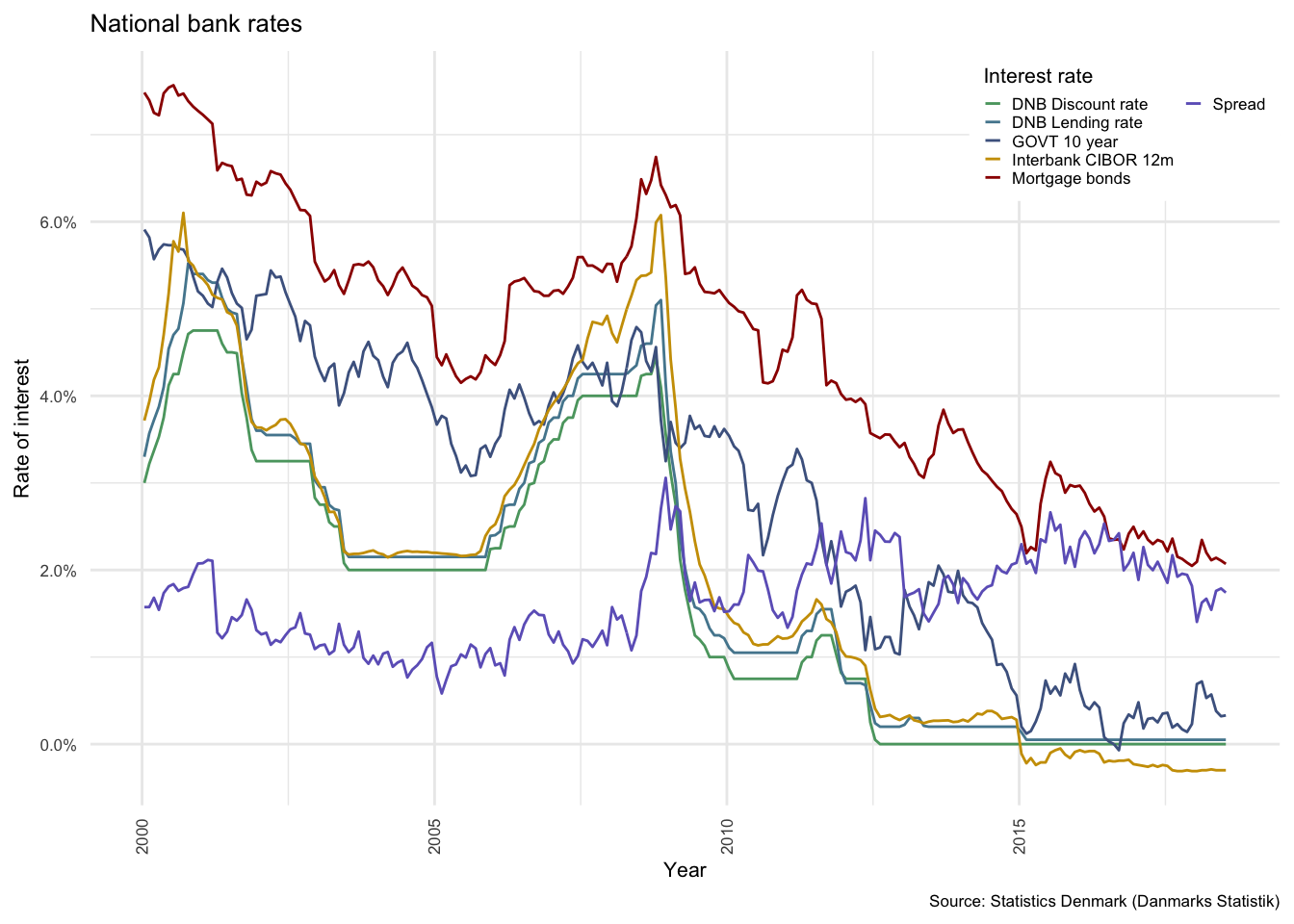

Figure illustrates, in part (a) the actual monthly interest rates available for new debt on Danish mortgage markets since 2013 (separated by term of interest fixation). Part (b) shows the progression of official interest rates in Denmark since 2000, where the “Mortgage bond” rate is the dark-red line, and is comparable with Fixed mortgage bonds in panel (a), the purple line, from 2013 onwards. Part (c) illustrates the impact of the shock to interest rates in the model in 2020.

Figure 3.9: Interest rates in Denmark

As can be seen from part (a), the rates available to fixed rate borrowers have followed market rates downwards throughout the period, although this illustrates only those rates available, rather than those paid. Figure showing the amounts actually paid in the section above, however, illustrates that the amount paid has also declined at a similar pace, although with a marginal delay.

The interest rates in the model are split into fixed and flexible rates for the purpose of testing the effects of a shock to interest rate on alternative compositions of mortgage debt. The baseline value of interest rates remains just below 1.5% on average for all debt.

The expected outcome is that where the proportion of fixed-interest outstanding debt is higher, the effects of a shock will be weaker, and vice versa. This of course can only have an impact in the case where mortgage debt is itself split into fixed- and flexible-rate debt.

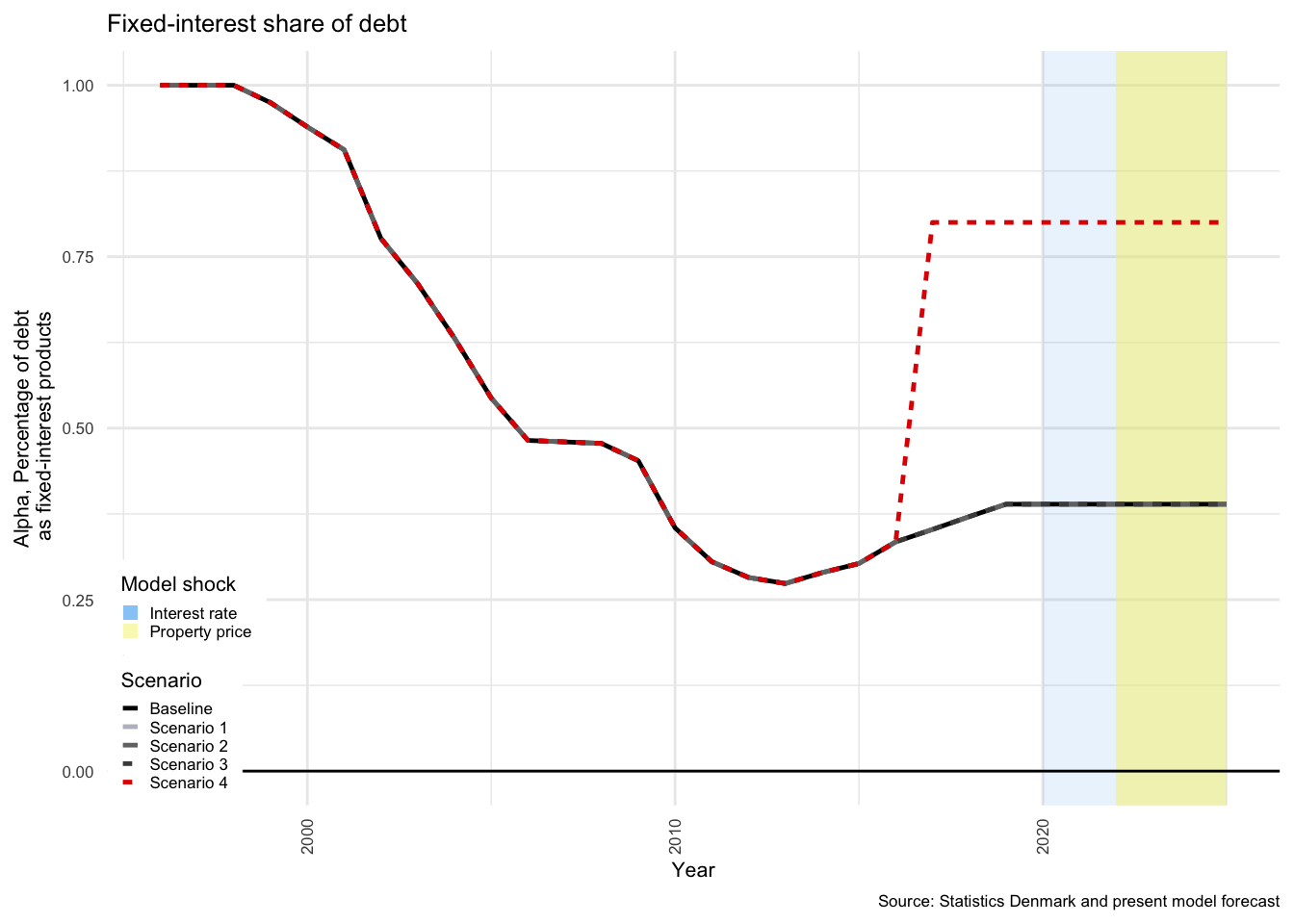

The total level of outstanding \(IBL\) for HH is split into fixed-interest (\(IBL_{FI}\)) and flexible-interest bearing liabilities (\(IBL_{FL}\)). The proportion of interest bearing assets held as \(IBL_{FI}\) is \(\alpha\).

\[\begin{equation} IBL^H_{{FI}_t} = \alpha(IBL^H_t) \end{equation}\]

and thus,

\[\begin{equation} IBL^H_{{FL}_t} = (1-\alpha)(IBL^H_t) \end{equation}\]

The level of \(\alpha\) is calculated from data acquired from multiple data sources at Statistics Denmark, and varies over time. The split was first introduced in 1996, but initial volumes were low. As discussed in Section , while the composition of this debt is significantly more complex than this, a strong argument can be made for an aggregation up to just these two categories. This split has no effect on the model prior to the shock in 2020, as the rate of interest on each is considered to be equal to the average rate used in the baseline scenario up to that point.

It is also possible to shock all other rates of return to a similar degree. Given the integration of financial markets, this would produce results in the model that are more realistic. Unfortunately, it would also conceal the effects that are purely due to dynamics linked to the interest cost of borrowing for households26.

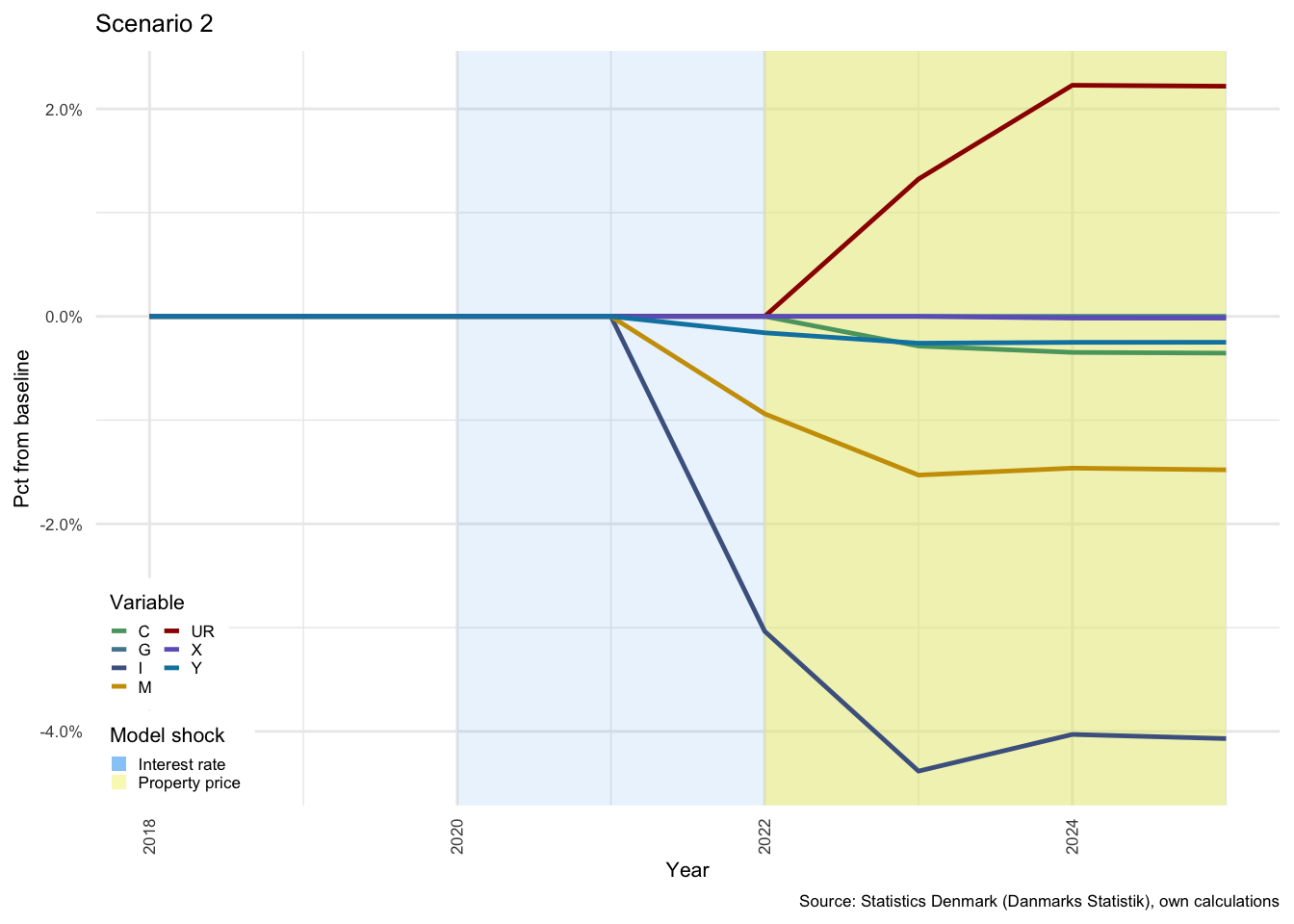

3.5.3 Scenario 2 - A fall in house prices

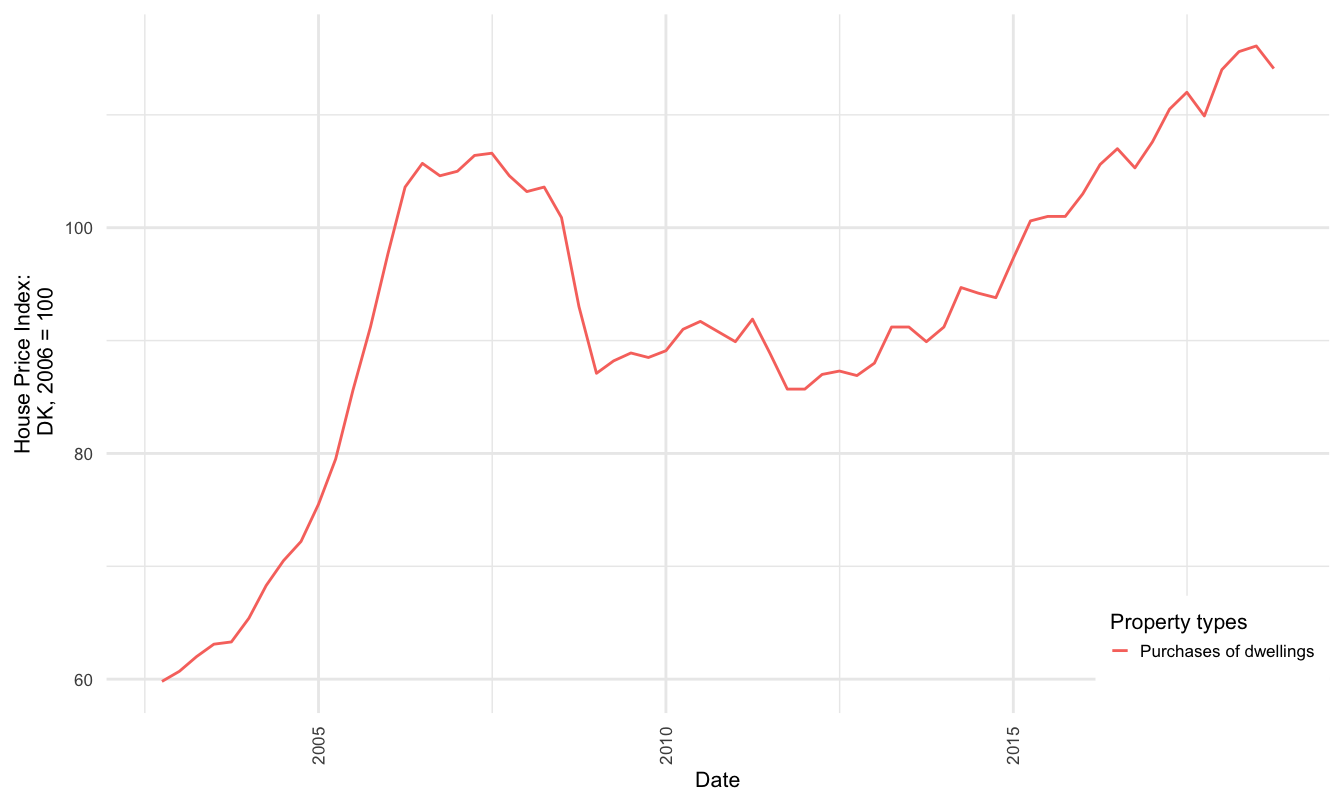

The second scenario is a fall in house prices. This is effected through a negative twenty per cent adjustment to the house price index (\(-20\%\)). This is a large change to house prices, but is equivalent to the stress test applied by the IMF (Sheehy 2014). At a national level, Figure illustrates that the average nominal house price index (HPI) for dwellings in Denmark has risen at a relatively steady pace since the GFC.

Figure 3.10: National House price index (HPI), 2006 = 100

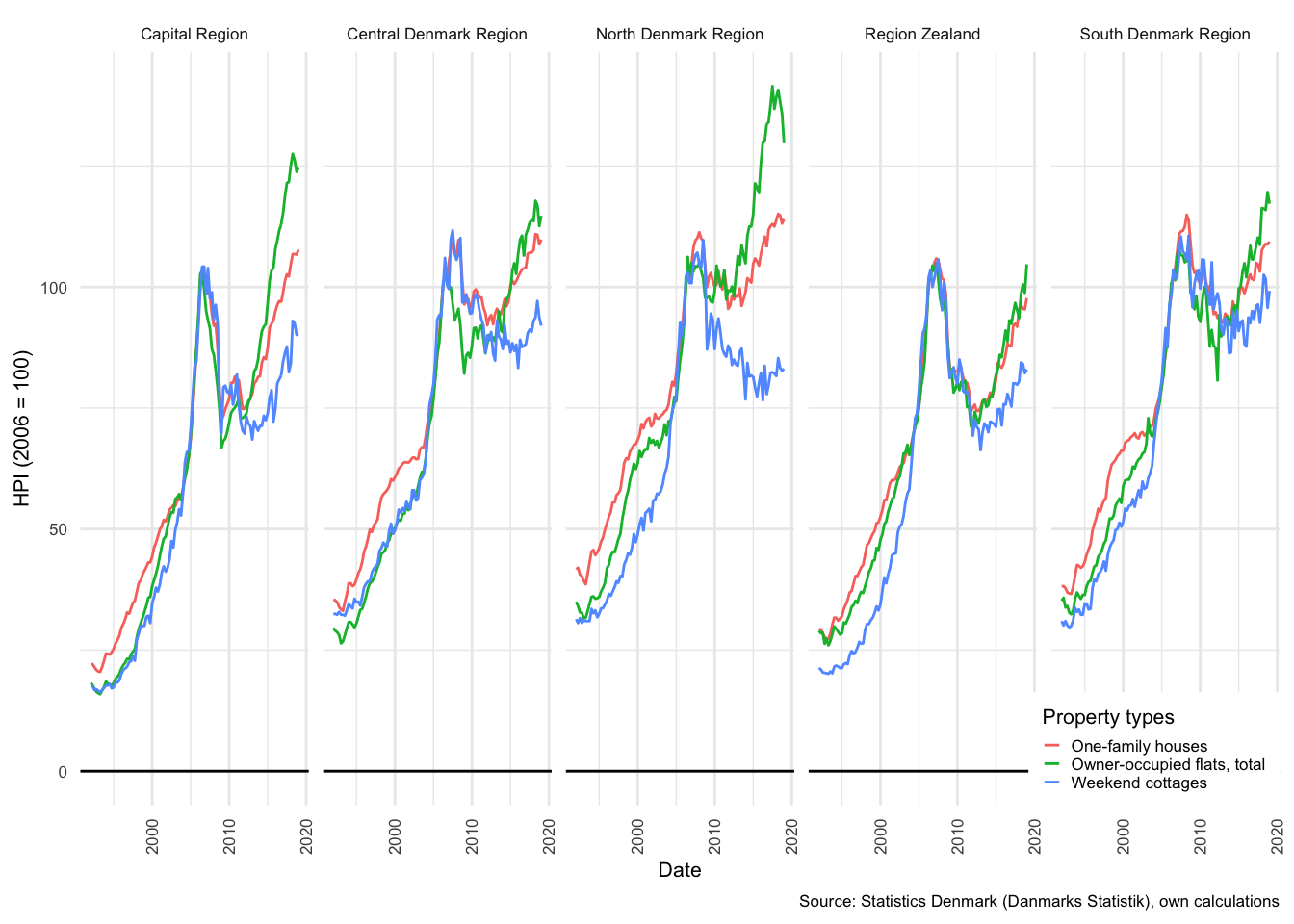

This follows a collapse of house prices during the GFC, where prices of Danish dwellings fell approximately 20% from the peak in 2006 to the trough in 2011. This average was not uniform across property types or regions. As shown in Figure , the prices of owner occupied flats in the Capital and North Denmark Regions have risen at roughly the same pace as prior to the GFC. This is not predictive of a correction or price collapse, but does suggest a possible housing price bubble in those markets. All other regions, appear to have only just recovered to pre-crisis prices27.

Figure 3.11: House price index (HPI), 2006 = 100

A more serious concern for potential borrowers is that several markets, particularly those for weekend cottages (otherwise known as summer houses) have not recovered in the period following the GFC. Thus, any property purchased between 2005 and the collapse in 2007 would have a high probability of falling into negative equity28.

In this model, households are only permitted to make productive investment in housing, which, as in G. Zezza (2008), Fontana and Godin (2013) and Beckta (2015), is considered only as a primary market. The major difference here is that households are assumed to produce the houses, whereas firms are housing producers for all three of the above-mentioned studies. The secondary market for houses is assumed to affect prices, but not the demand for additional housing investment. Demand for housing investment is determined by by a Tobin’s-Q-like function, partially driven by changes in disposable income and previous period housing investment, and partially driven by a relative shift in sales price (\({P^H_{t-i}}\)) and construction cost (\({P^i_{t-i}}\)) indices.

Real investment in fixed assets (dwellings), in Equation , is estimated as a log-linear function that depends on conditions in previous periods. This assumes that the decision to invest in houses occurs based on recent developments, but that actual changes in investment in fixed assets takes some time to materialise. It thus takes one period before the effects of the house price shock can be observed.

\[\begin{equation} ln(i^H_t) = \beta _i + \beta _i ln(i^H_{t-i}) + \beta _i ln \Bigg( \frac{P^H_{t-i}}{P^i_{t-i}}\Bigg) + \beta _iln(yd^H_{t-i}) \label{eq:realhousinginvestment_intext} \end{equation}\]

The shock imposed on the model is to the numerator of the Tobin’s Q ratio29. The imposed decline in house prices affects sales prices negatively, relative to the cost of production, and thus has a contractionary effect on the Tobin’s q ratio, \(\Bigg(\frac{P^H_{t-i}}{P^i_{t-i}}\Bigg)\), and thus on HH real investment (\(i^H_t\)). The shock is implemented as a permanent decline in prices, and thus changes the value of the ratio for all periods following the shock. Growth in house prices continues according to the same trajectory as in the baseline in order to make for a more effective comparison.

The nominal level of investment in housing can be calculated by inflating the real investment in housing series (\(i^H_t\)) by the investment price index (\(P^i_t\), which is sourced from Statistics Denmark):

\[\begin{equation} I^H_t = i^H_t(P^i_t) \end{equation}\]

The nominal stock of housing (\(K^H\)), as with other assets to come, follows the simple process of previous stock (\(K^H_{t-1}\)), plus acquisition (in this case investment in new houses), less depreciation (\(D^H_t\)) plus capital gains (\(K^H_{CG_t}\)).

\[\begin{equation} K^H_t = K^H_{t-1} + I^H_t - D^H_t + K^H_{CG_t} \label{eq:nominalhoushingcapital1} \end{equation}\]

Capital gains on houses, in turn, can be calculated in an ex post manner as: \[\begin{equation} K^H_{CG} = \Delta P^H_t (K^H_{t-1}) \end{equation}\]

Which is simply the change in the price of houses applied to the level of stock at the end of the preceding period.

The change in house prices (\(\Delta P^H_t\)) leading into the current period is then by definition the same ratio proportion of capital gains to previous housing capital.

\[\begin{equation} \Delta P^H_t = \frac{KH_{CG}}{K^H_{t-1}} \label{eq:changehouseprice_intext} \end{equation}\]

Nominal housing capital held by HH at the end of the current period can be expressed as the price adjusted stock at the end of the previous period, plus net investment and depreciation. Equation is effectively a restatement of Equation , but with greater emphasis on the variable shocked in the analysis.

\[\begin{equation} K^H_t = K^H_{t-1}(1 + \Delta P^H_t) + I^H_t- D^H_t \label{eq:nominalhoushingcapital2} \end{equation}\]

The deflated real capital index can then be found, as in Equation () by dividing the series by the investment (housing) price index, from Equation ().

\[\begin{equation} k^H_t = \frac{K^H_t}{P^i_t} \label{eq:realhoushingcapital_intext} \end{equation}\]

Housing capital then forms part of HH net wealth, which feeds back into consumption decisions in subsequent periods. A decline in net wealth in period \(t\) leads to a decline in consumption in period \(t+1\).

The effects of changes in net wealth (\(NW\)), are then felt directly in the level of HH consumption, but with a lag on one period (as can be seen in Equation () in the appendix). Although a fall in house prices does not affect household disposable income to a substantial degree is contributes to a decline in overall economic activity, and therefore reduces the demand for labour in subsequent periods. This ultimately does affect household income but the effect is not as immediate as was the case for the interest-rate shock.

3.5.4 Scenario 3 - Combination of Scenarios 1 and 2

The third scenario consecutively applies the shocks from Scenarios 1 and 2. First the interest rate increase in 2020, and then the decline in property prices in 2022. This combination sets up the comparison to be introduced in Scenario 4 below.

3.5.5 Scenario 4 - Comparison for Scenario 3, proportion of fixed-interest debt 80%

The final alteration to the model is an increase in the proportion of mortgage debt held as fixed debt (\(\alpha\)) from the 2016 level of 33.42% up to 80% in 2017. This shift allows us to test the hypothetical difference of the impact of a shock to interest rates in an artificial scenario, where the proportion of flexible debt amounts to only 20% of outstanding household mortgage liabilities.

3.6 Simulations

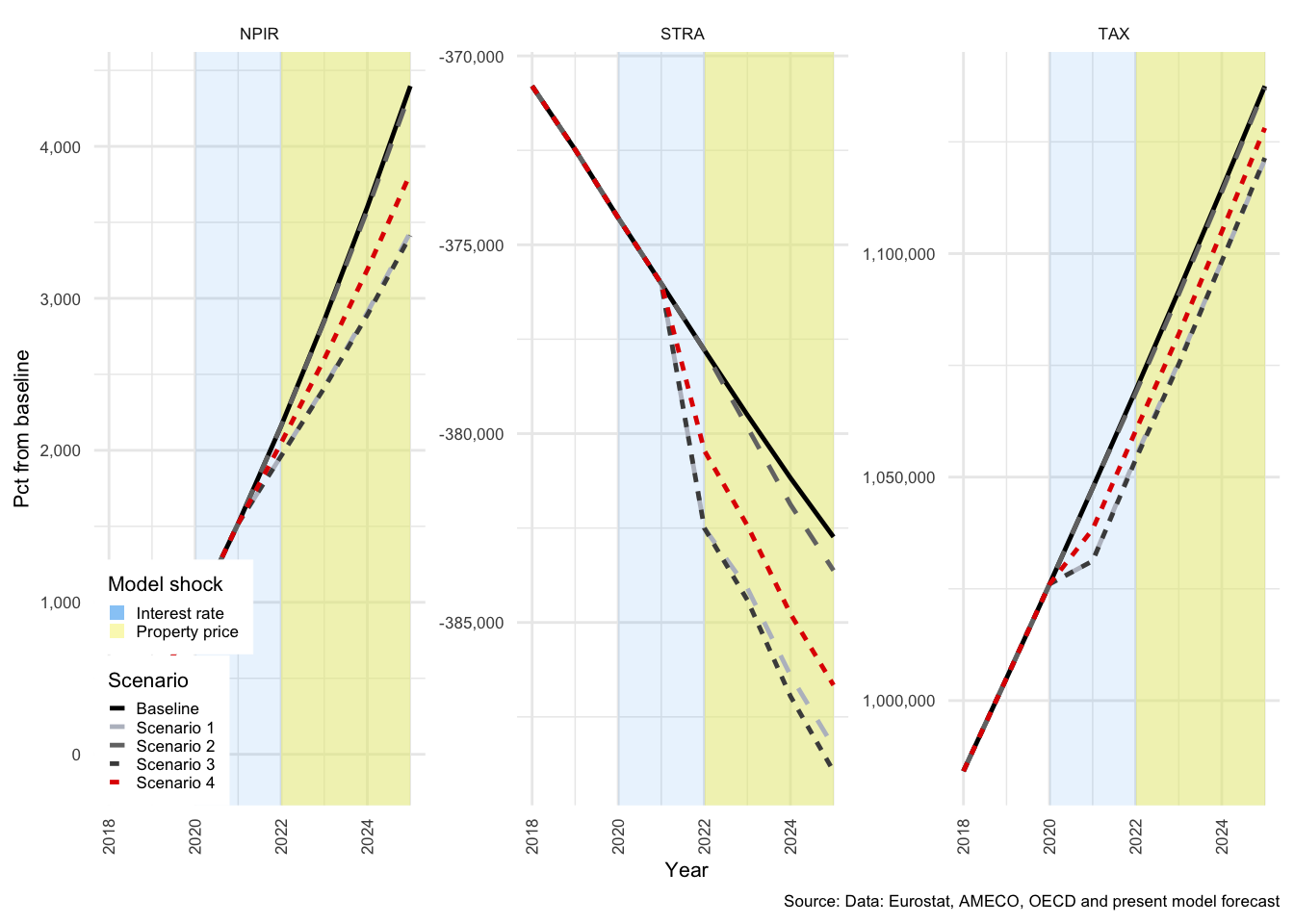

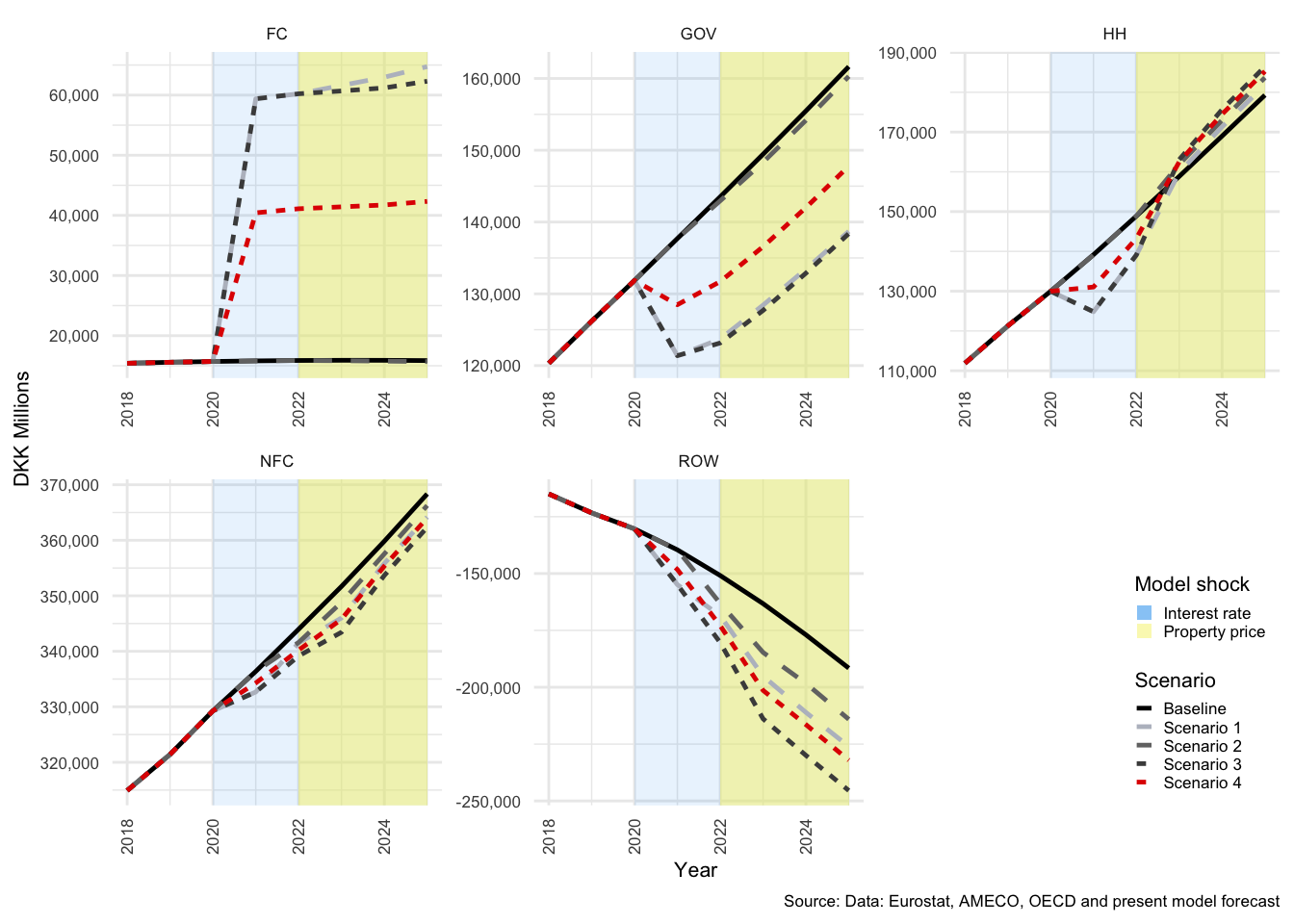

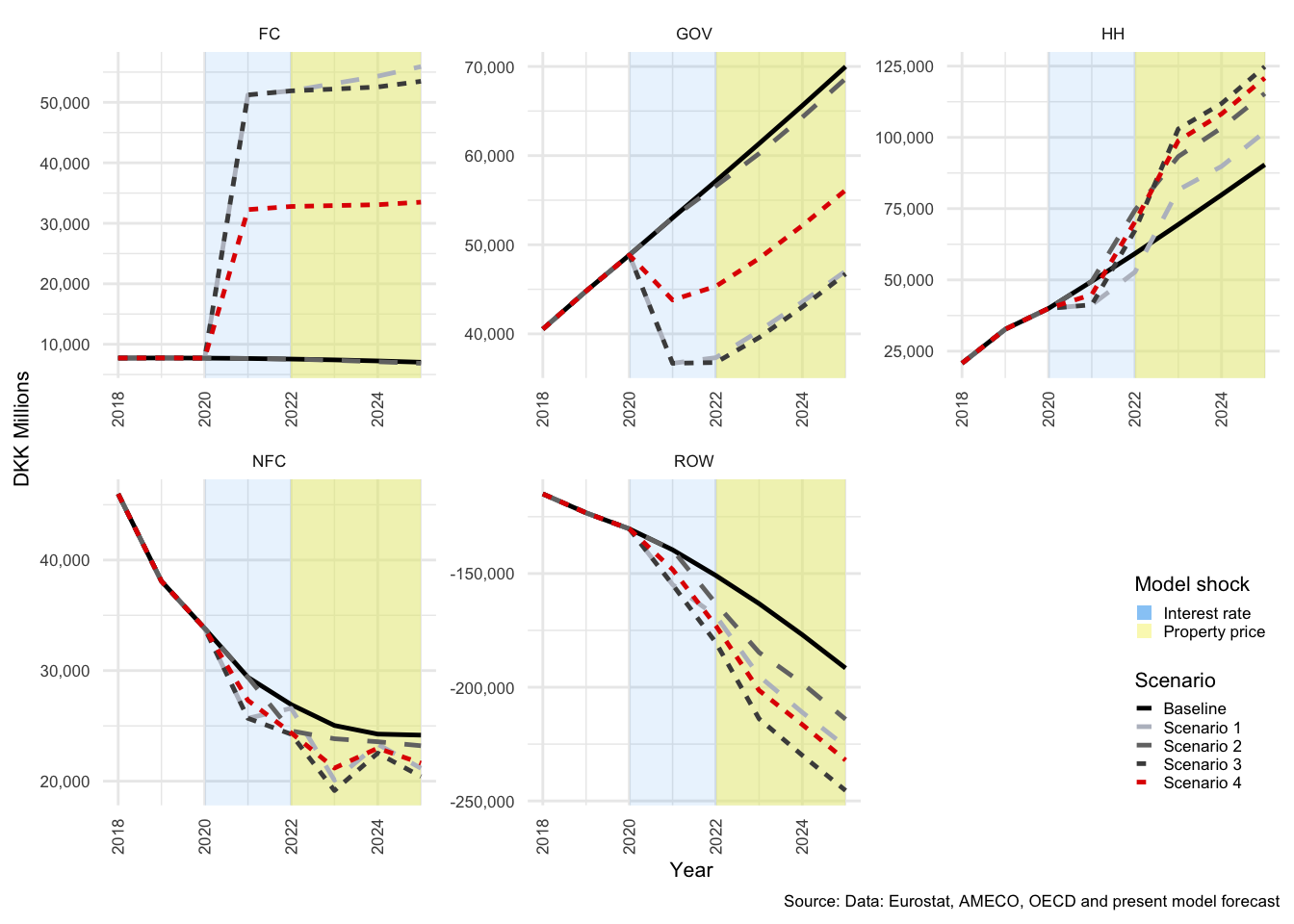

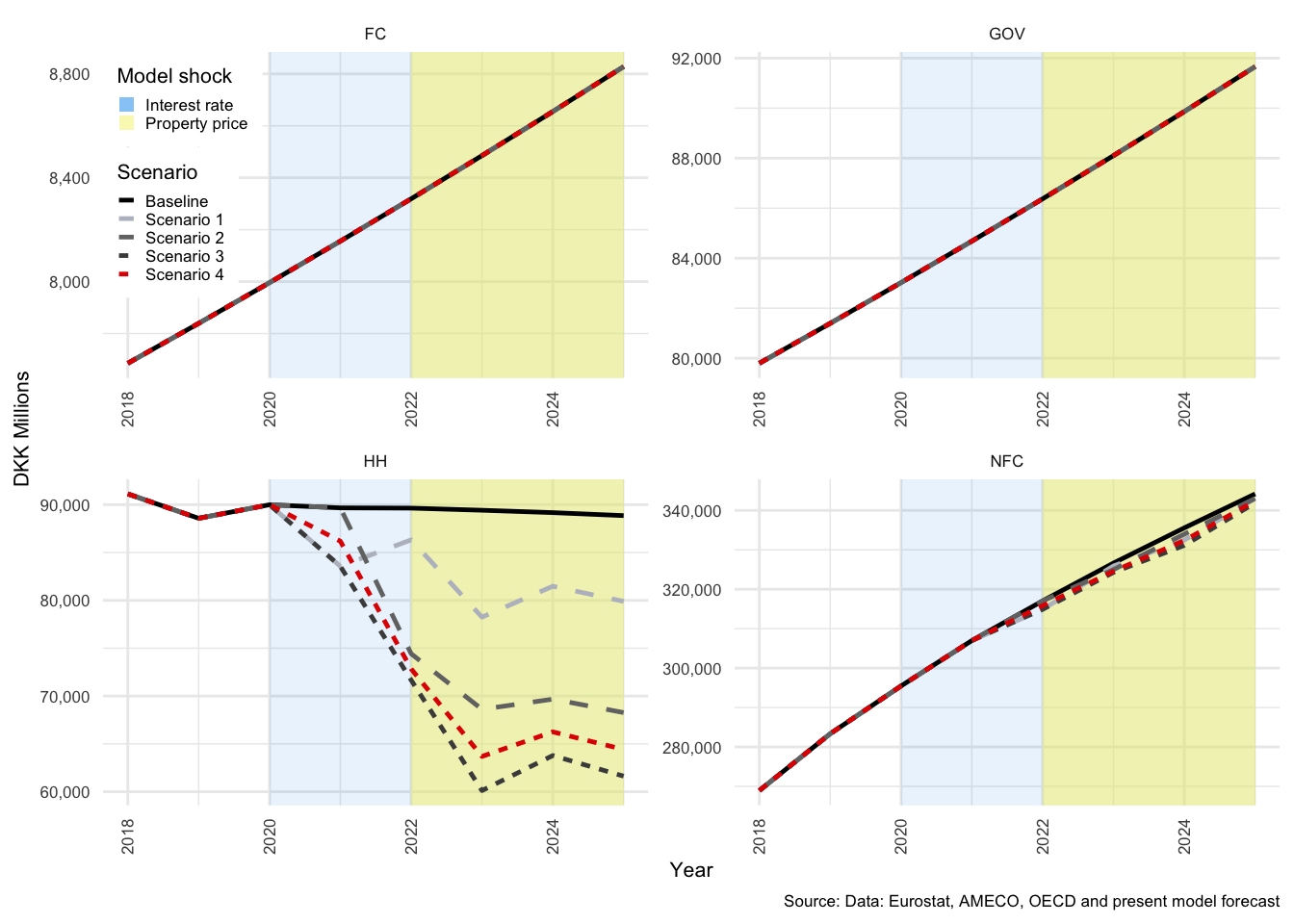

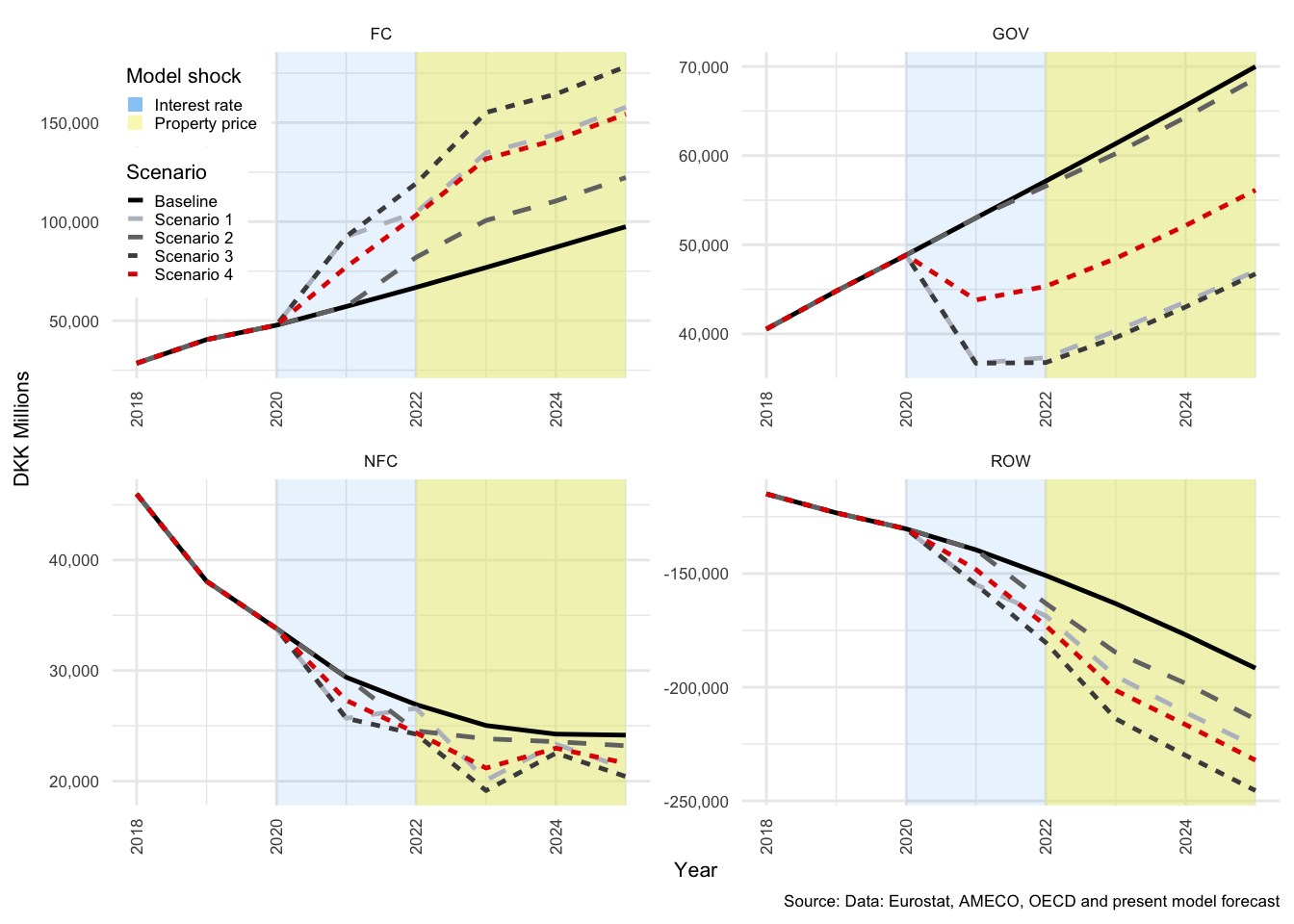

This section explains the transmission of the two shocks in the scenarios described above. First, the components of the economy that are most dramatically affected are identified, and thereafter the key transmission channels that cause these effects are briefly discussed.

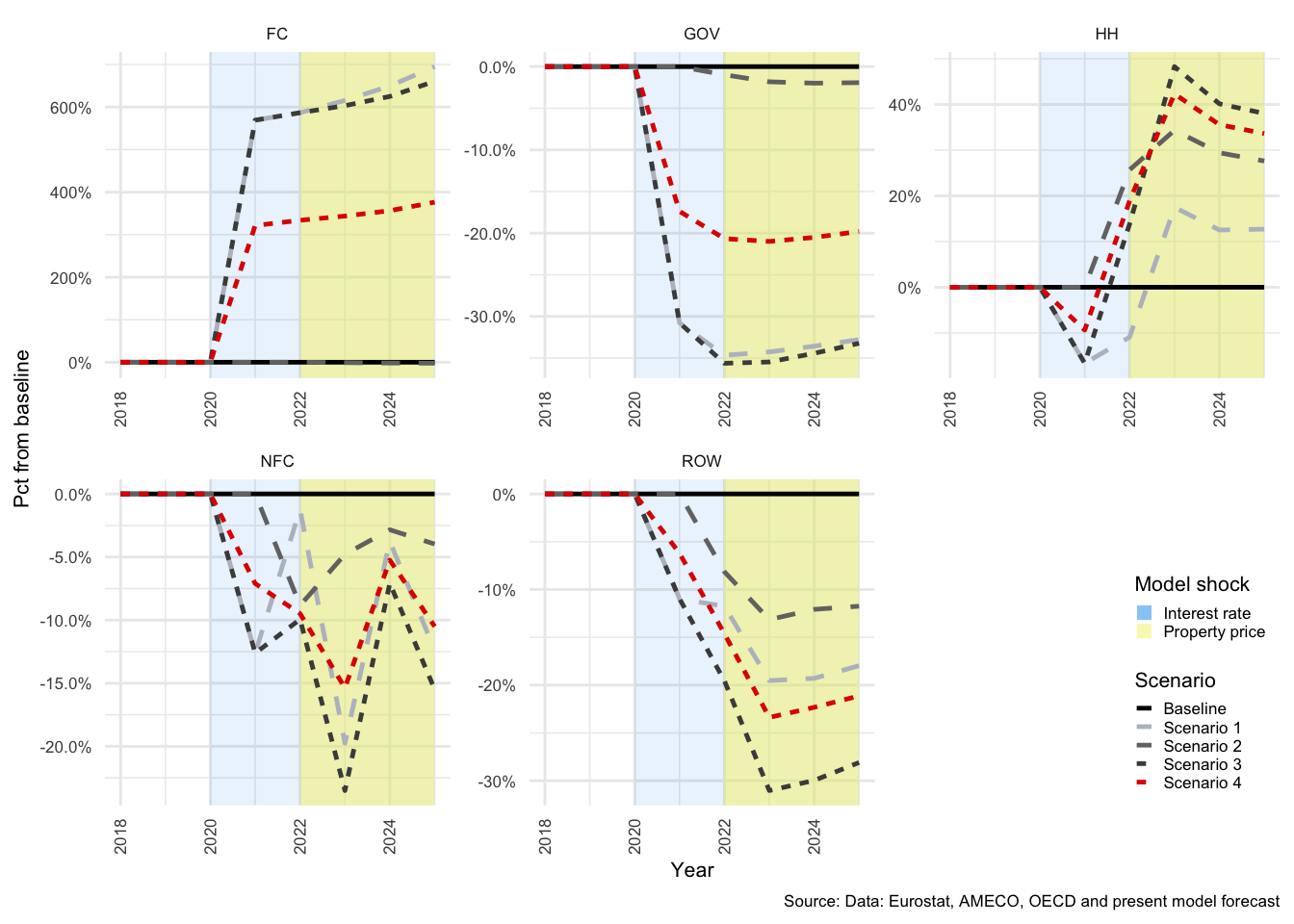

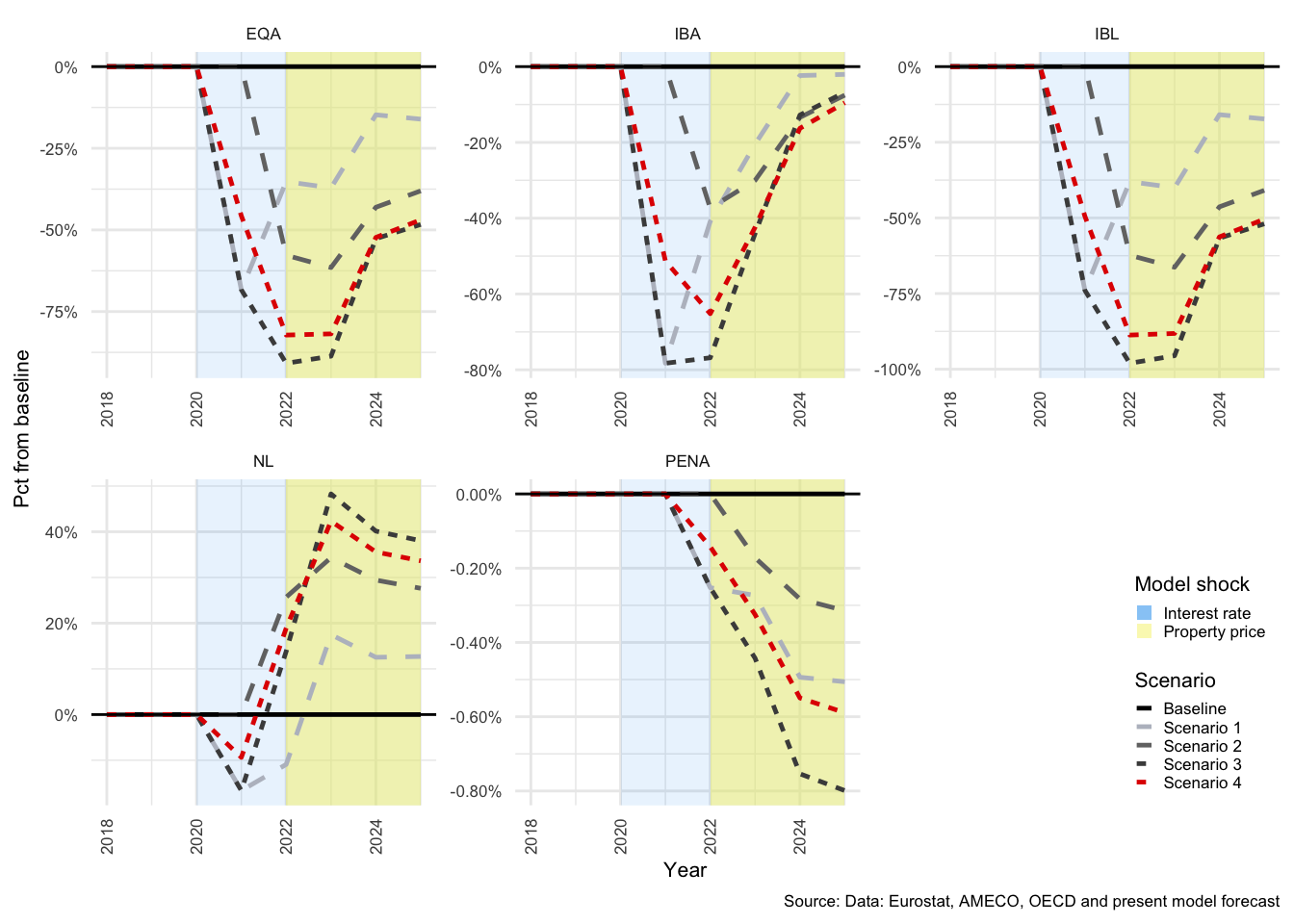

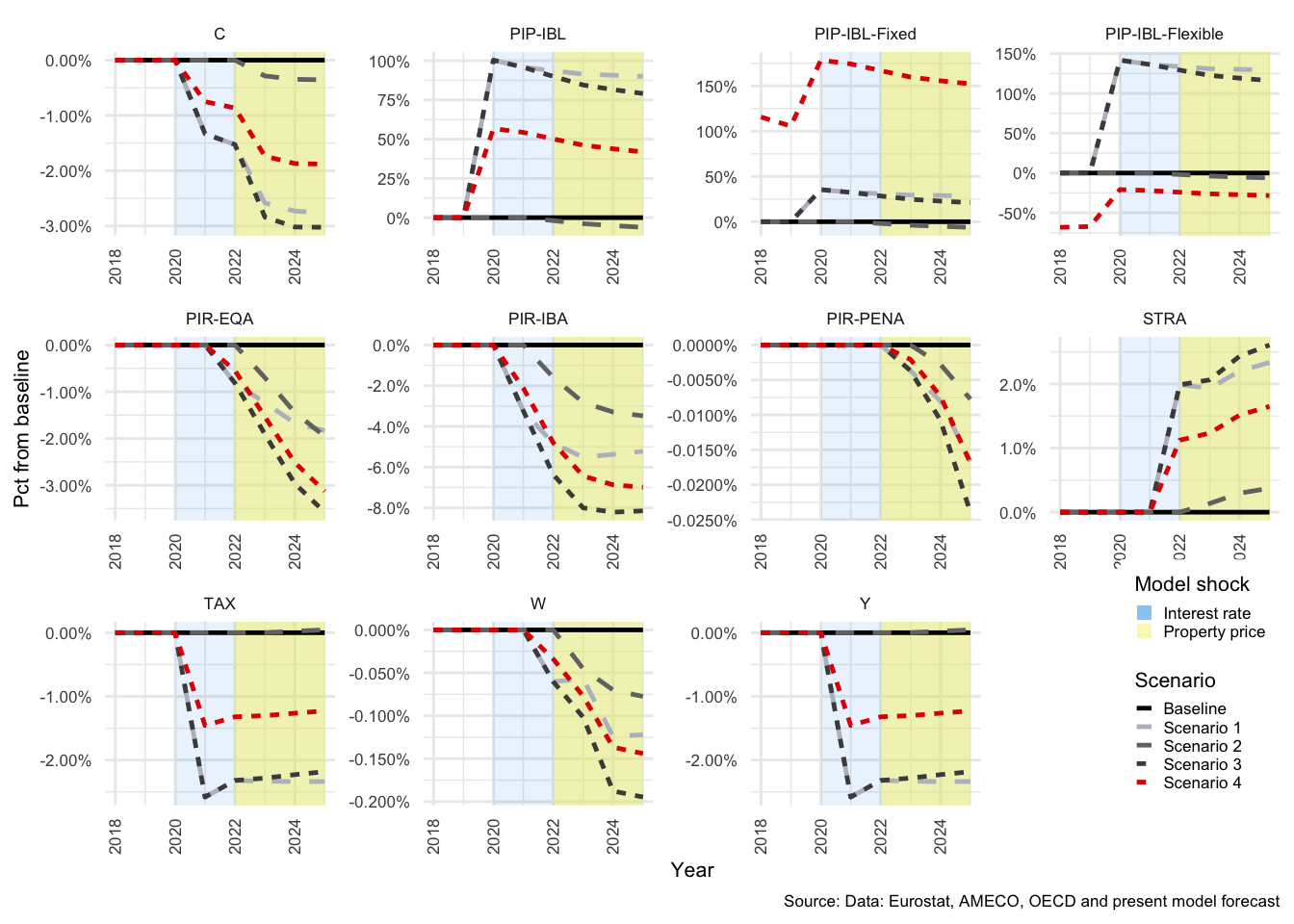

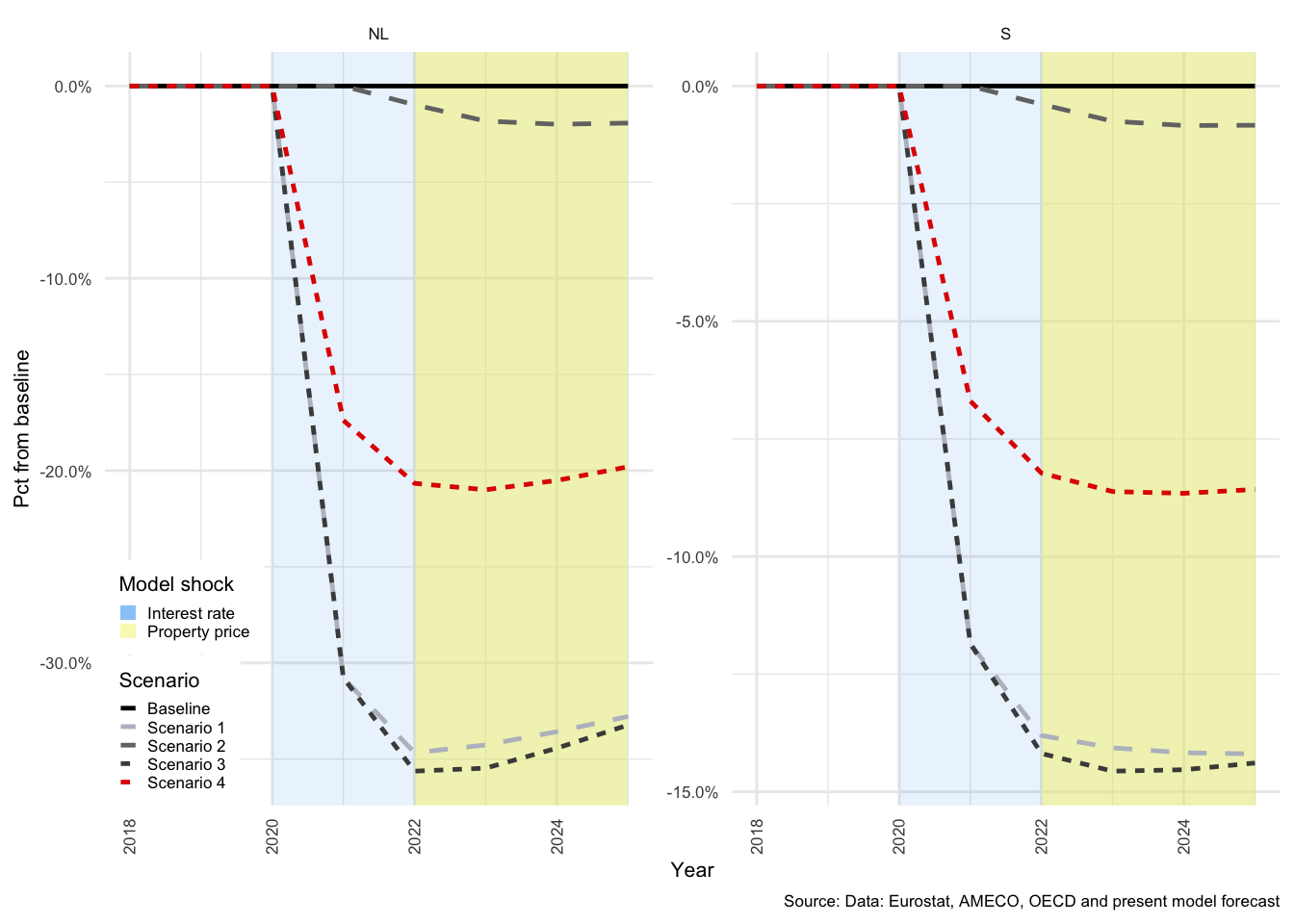

The key take-aways from this section are that shock 1 and 2 both propagate through the economy as described above, and that Scenario 3 results in greater volatility in the responses of the economy than Scenario 4. This has implications for the stability of the balance sheets of each sector and for the economy as a whole.

The effects of each shock are summarised in tables in Section for each of the above-mentioned scenarios30. This approach allows a quick summary of the impacts of a shock. It shows all affected variables, and thus provides a snapshot of how broadly the shock propagates. One drawback is that it is a cross section in time, and thus is not able to show the progression of feedback effects over time. These tables are both used as a guide to the most important transmissions, and as a consistency check, to ensure that the model behaves within reason.

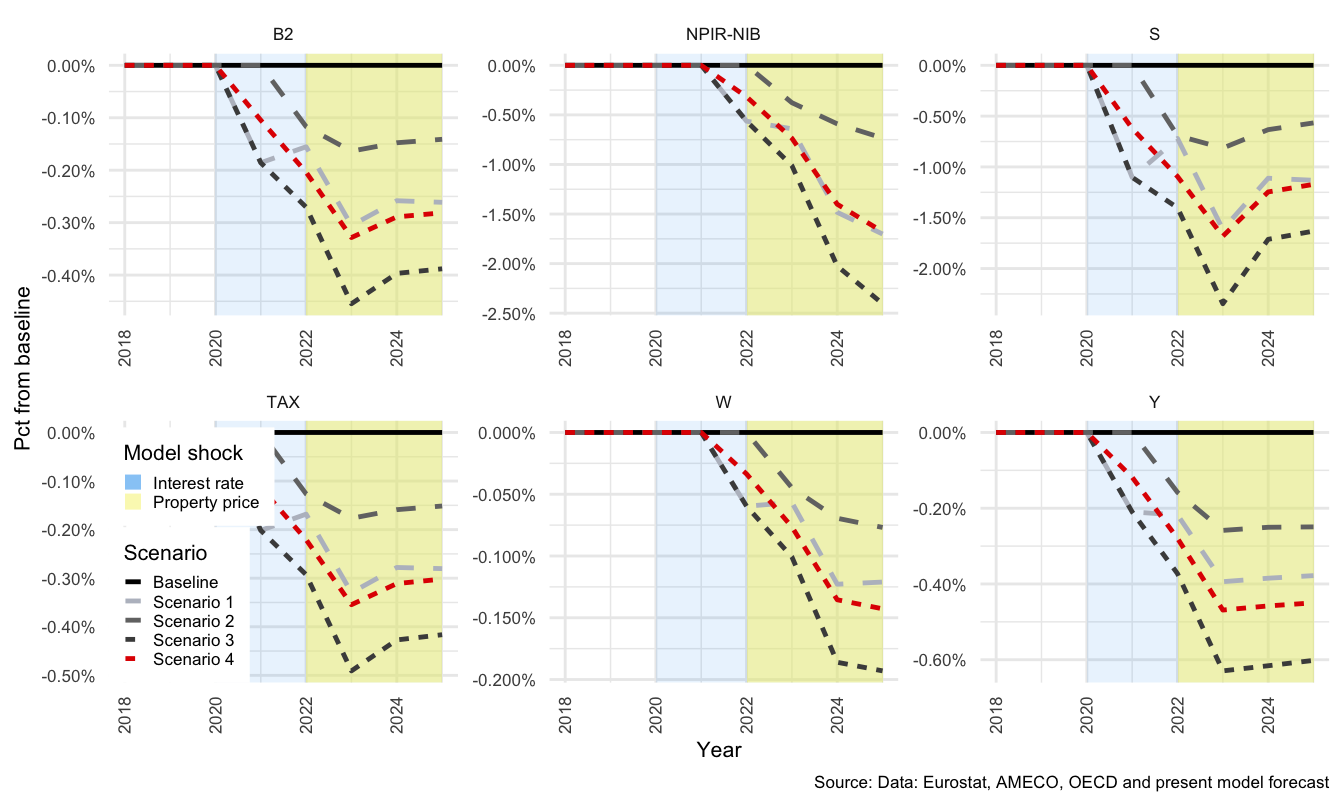

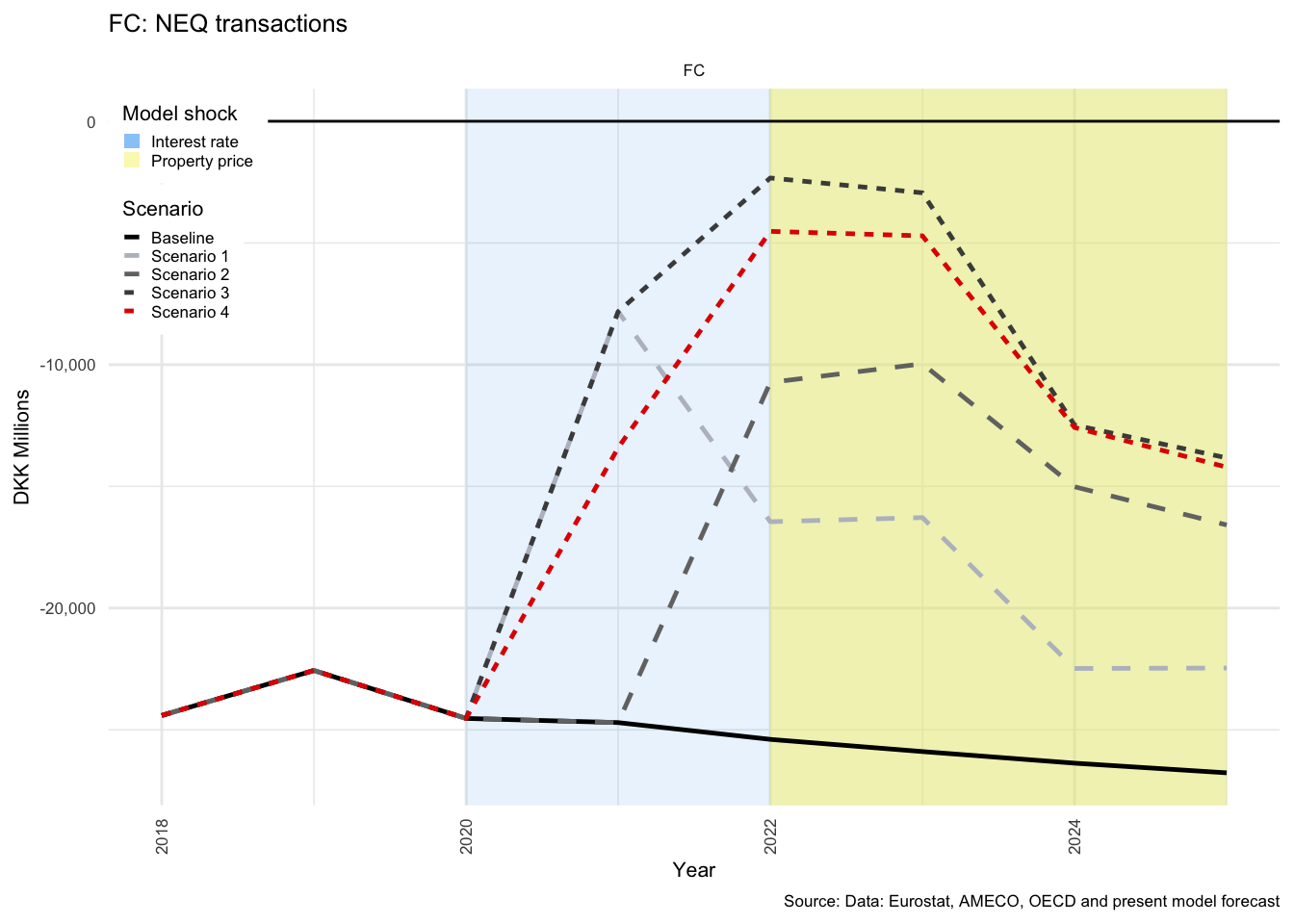

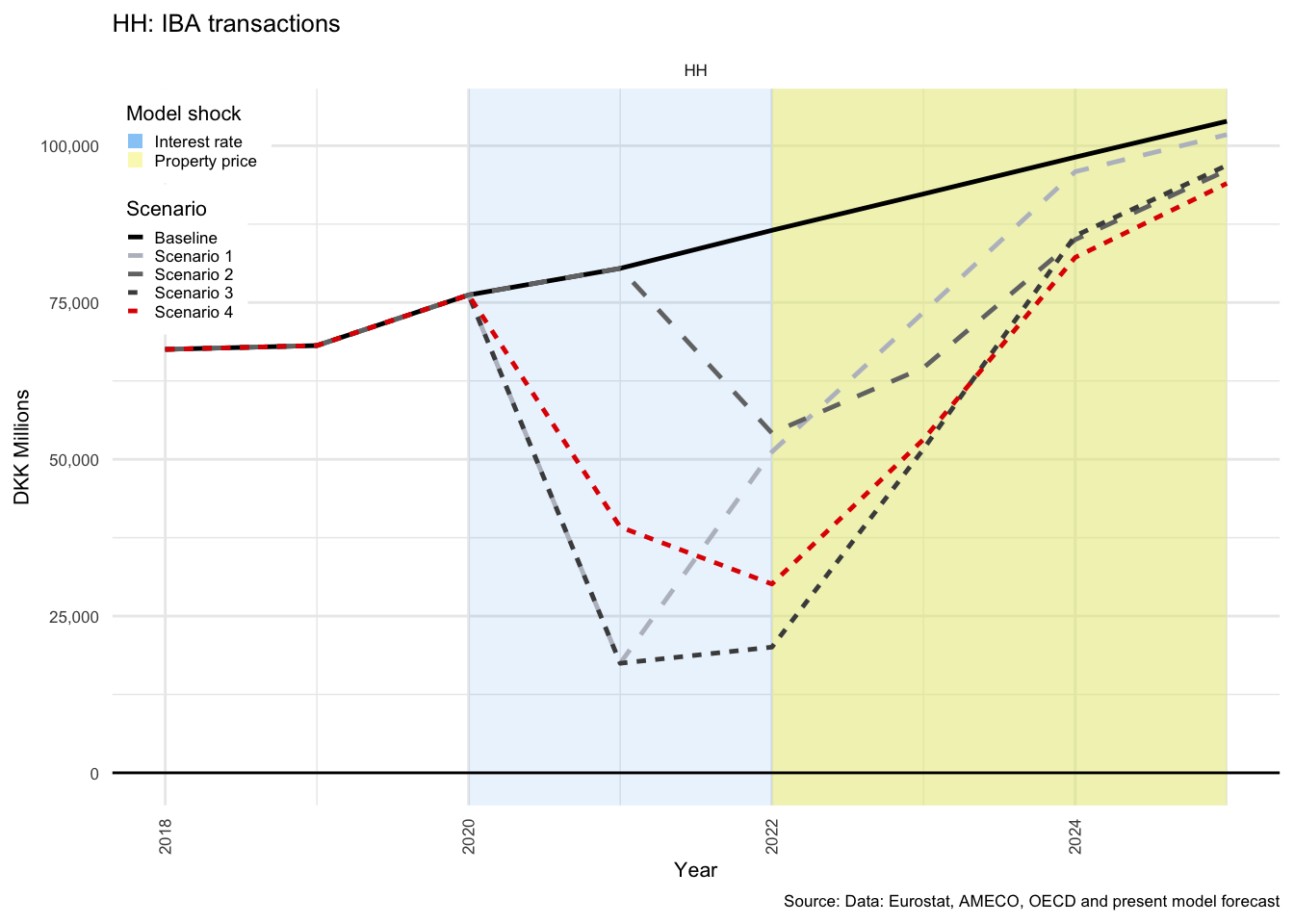

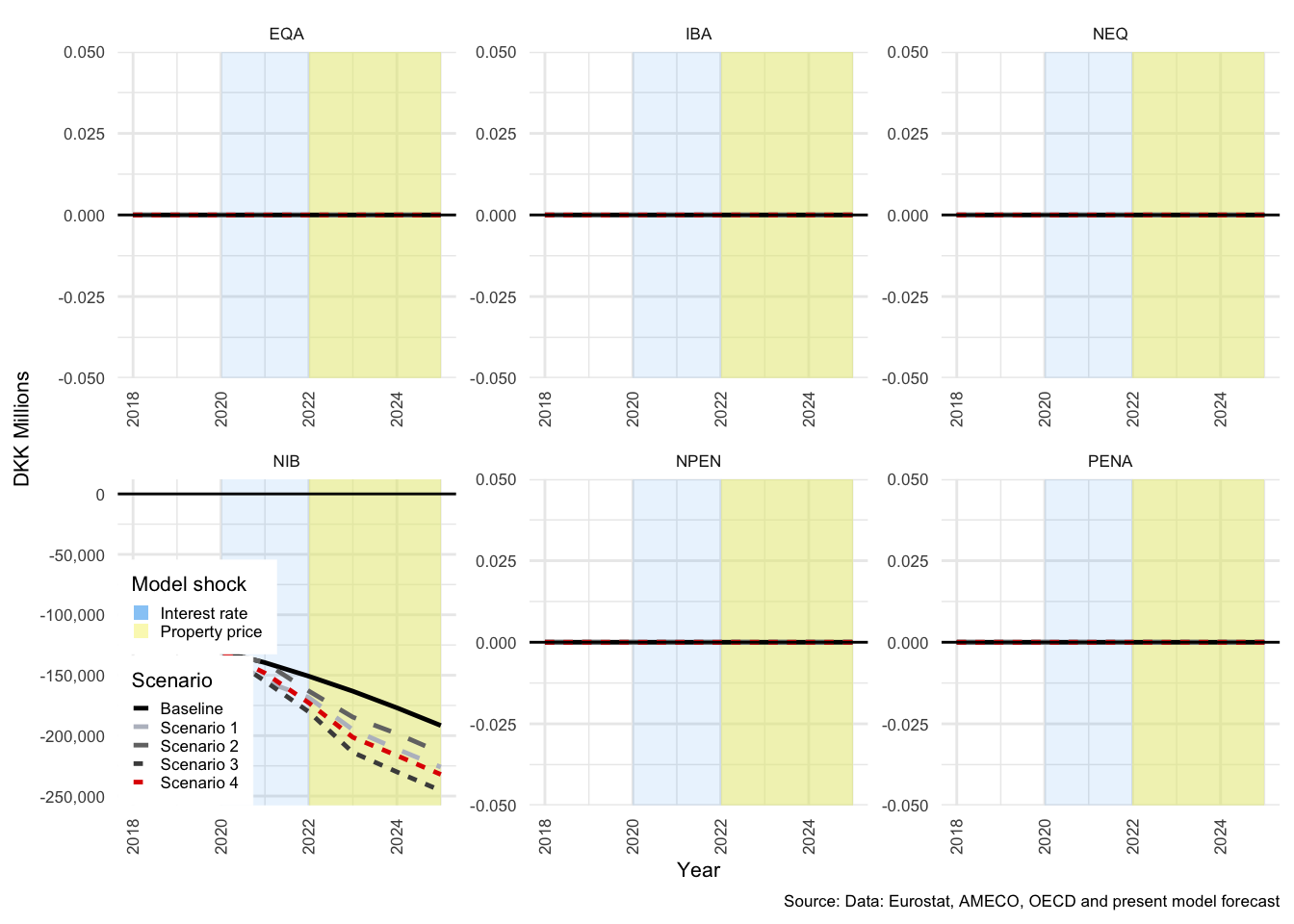

The model responds largely as expected to the first shock, with the exception of the rather extreme response of the financial sector. This is because FC transactions in net interest bearing assets (\(NIBTR^F\)) absorbs all financial transactions of the other sectors - or, stated differently, accumulates all financial imbalances. The second shock, to property prices, has a more interesting result with regard HH savings and will be discussed in more detail in the HH section below.

As noted above, each of the sectors has a buffer flow that summarises the collective effect of each shock, and each of the shocks are quite extreme in nature. It is therefore unsurprising that the effect on the passive elements is somewhat exaggerated. Even though shocks of the same magnitude have occurred in the past, they are not common events and have only been used here to enhance the potential risks associated with the different debt structures.

3.6.1 General economy

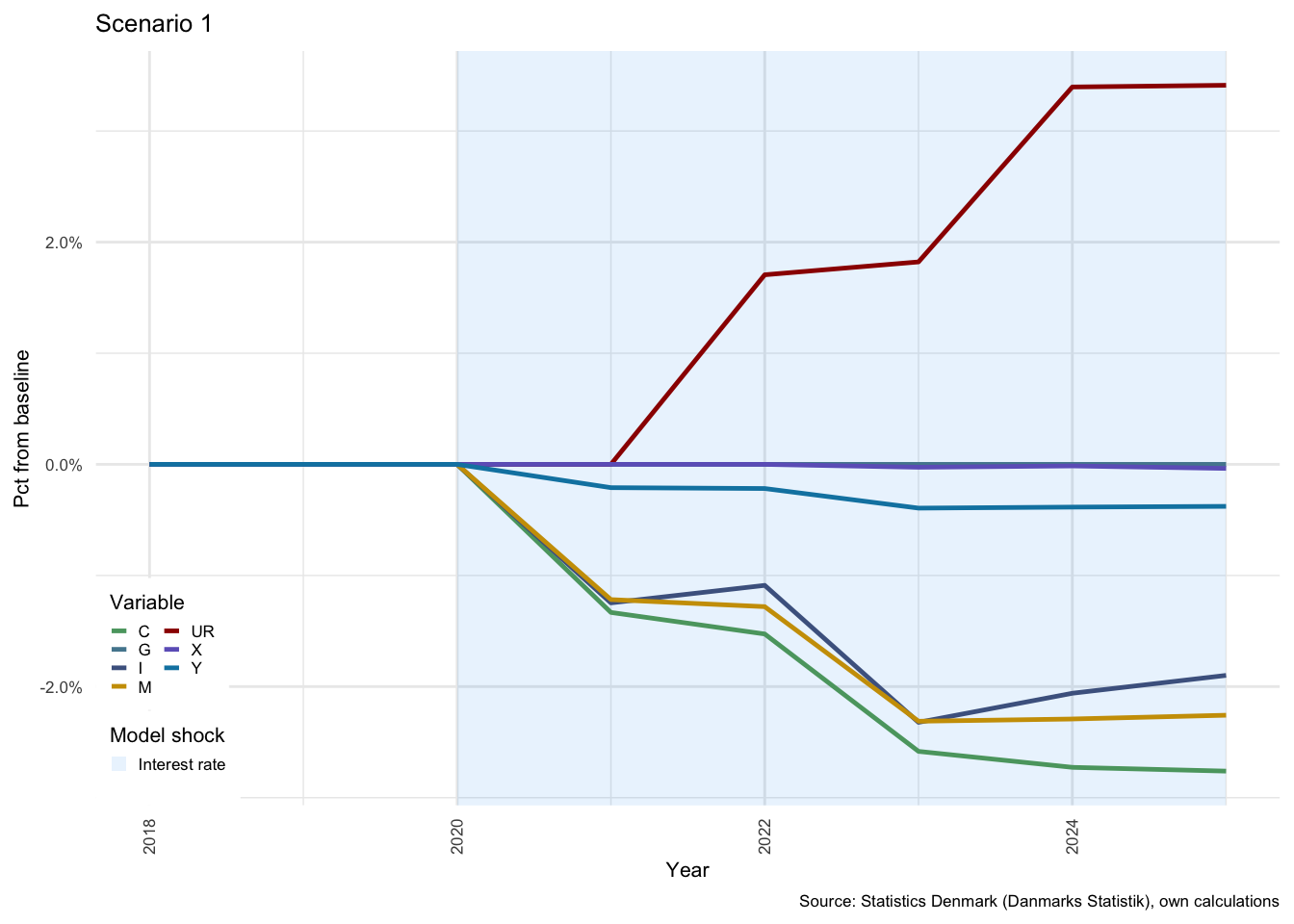

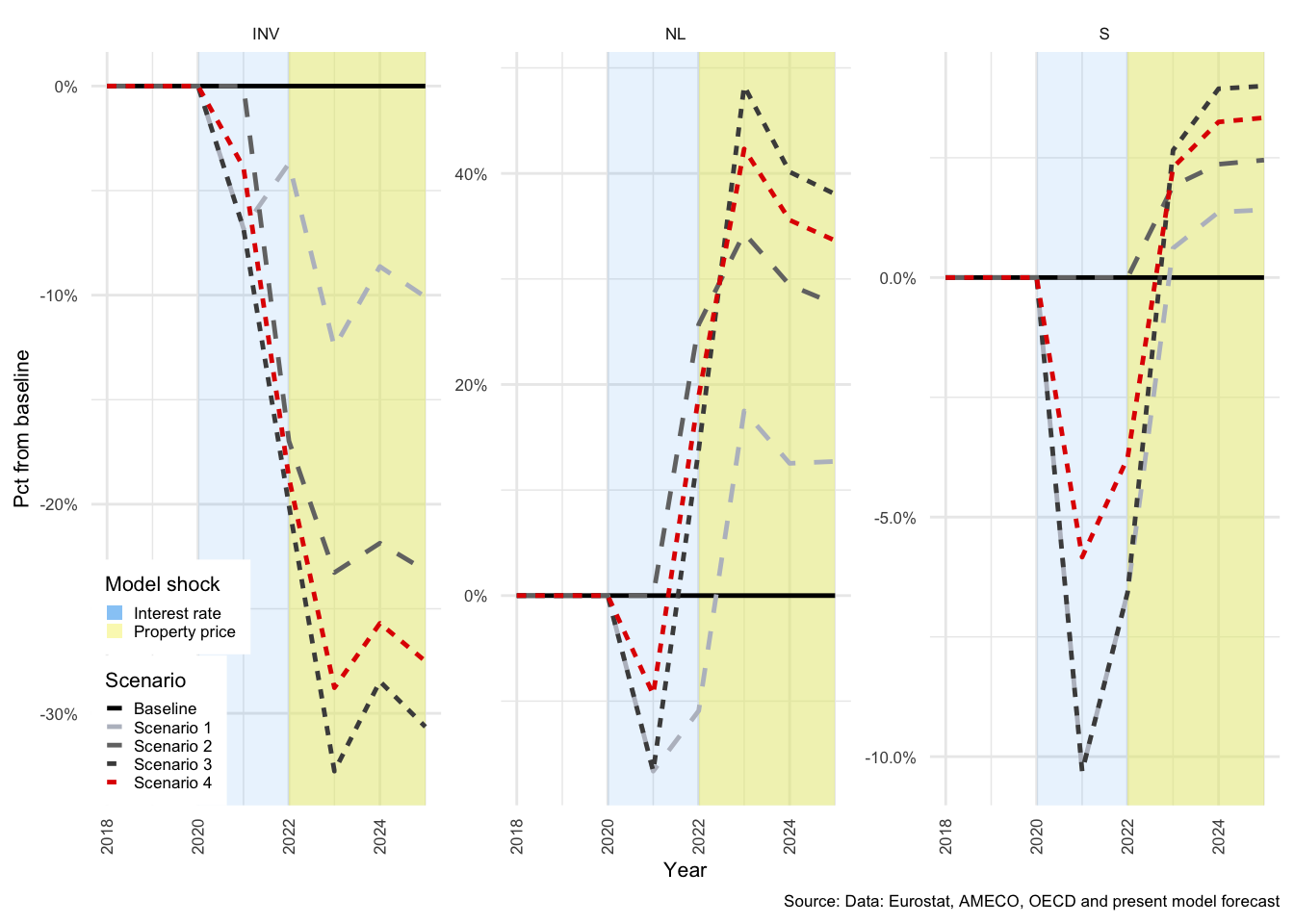

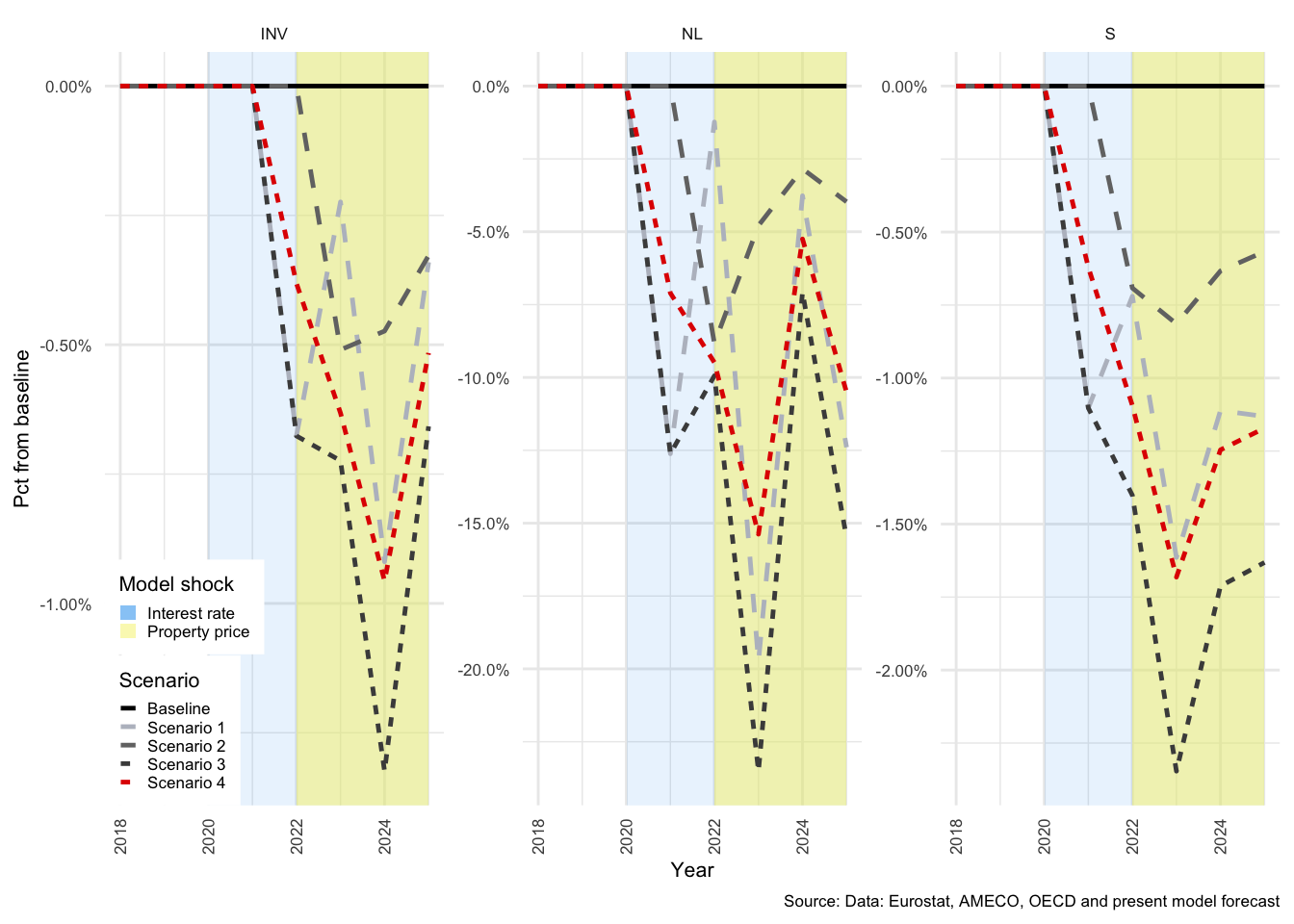

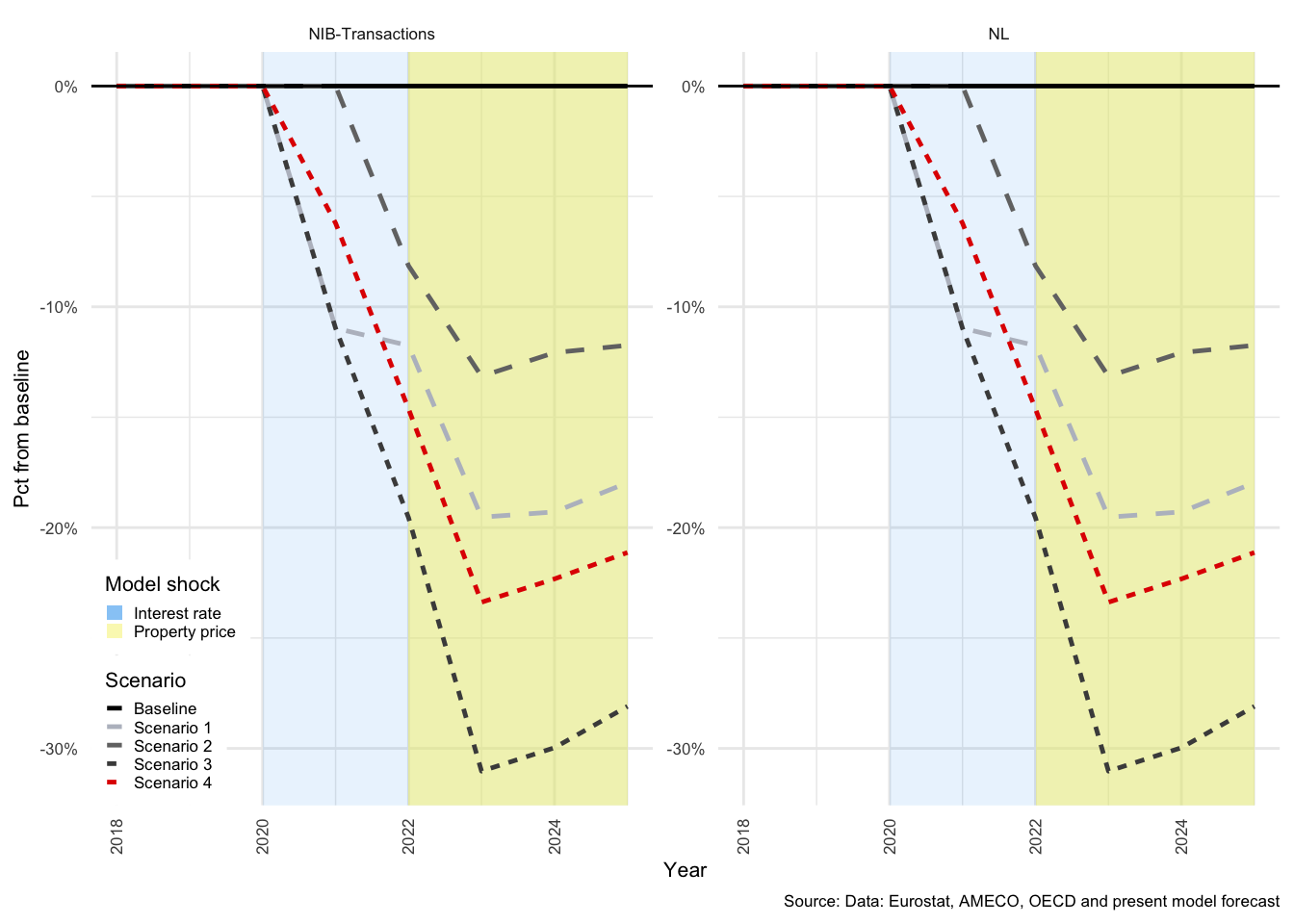

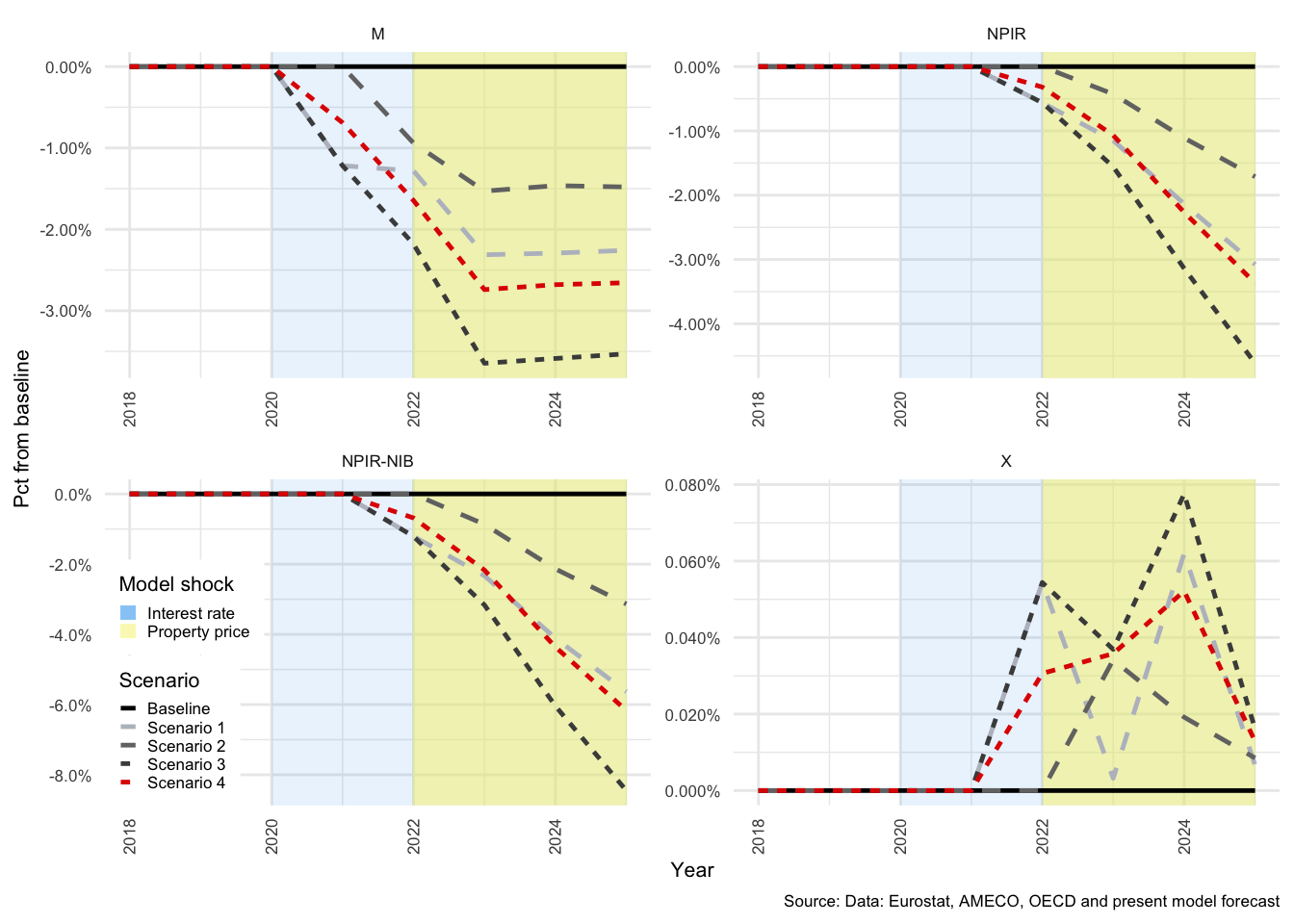

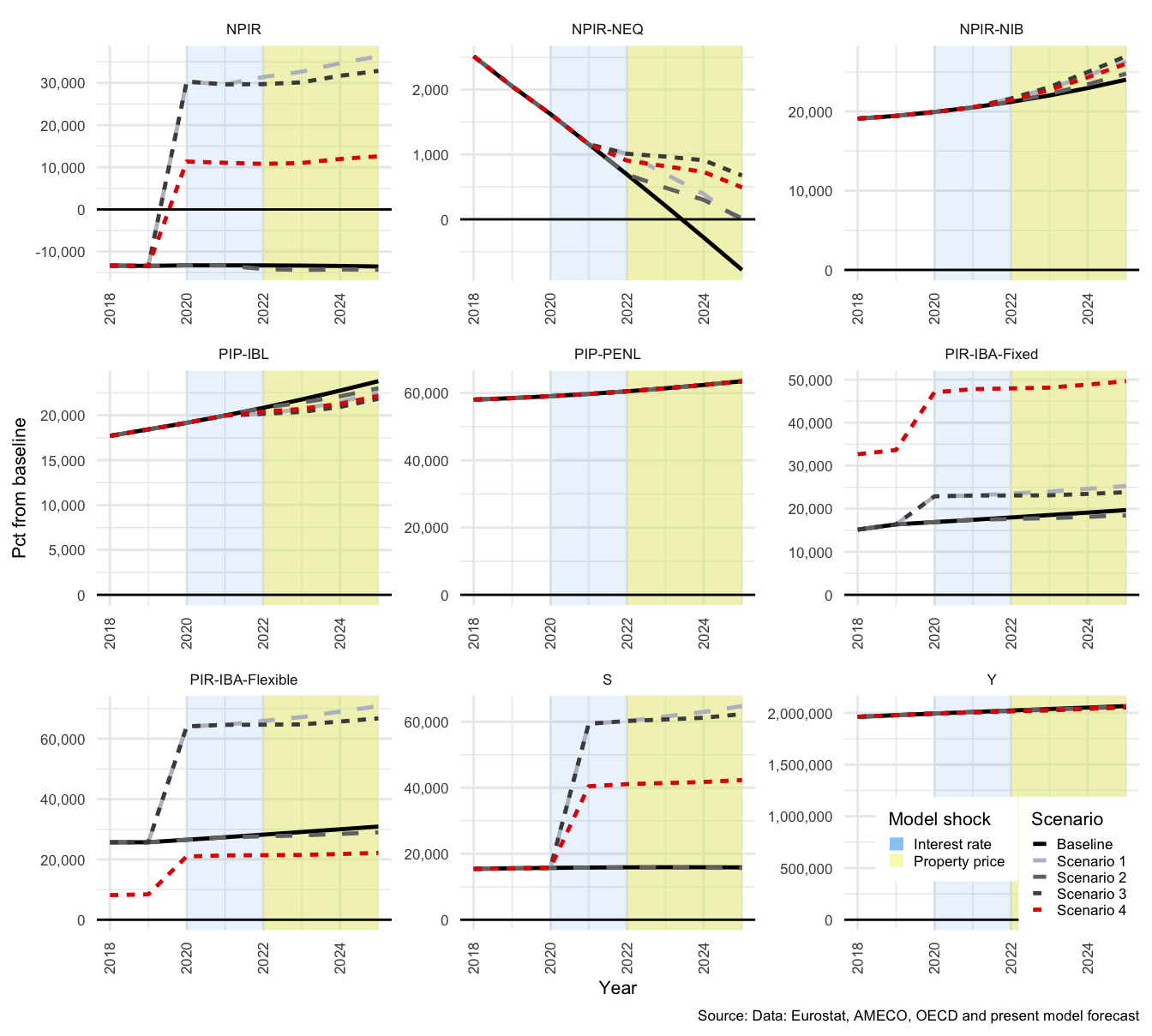

The first shock (to interest rates) has a delayed effect that is first visible in the shift from period 2020 to period 2021; as can be seen for Scenarios 1, 3 and 4. The second shock (to property prices) takes effect immediately in 2022, and can therefore be seen to take effect from period 2021 to period 2022 for Scenarios 2, 3 and 4. At a broader economic level, the strongest impact on the major components of GDP from the first shock are a decline in gross fixed capital formation (\(I\)) of -1.25% and in imports (\(M\)) of -1.22% (and as a result, net exports rise by just over 10.52%). Figure shows how \(C\), \(I\), \(G\), \(X\) and \(M\) would evolve relative to the baseline, for scenarios 1 and 2, and Figure that shows the same for Scenarios 3 and 4.

The shock to interest rates only impacts the model at \(t+1\) and so there is no change from the baseline in year 2020, whereas the impact of a property price shock takes immediate effect in 2022. Exports remain relatively unchanged under both shocks, only marginally affected due to a shift in domestic prices. \(Y\), or GDP, is more affected by the shock to interest rates in Scenario 1 than by property prices in Scenario 2, largely as a result of the limited impact of the property price shock on \(C\) and \(M\). The rapid rise in interest costs clearly result in a decline in all demand components except for \(G\), which is exogenous and therefore remains completely unchanged in all scenarios.

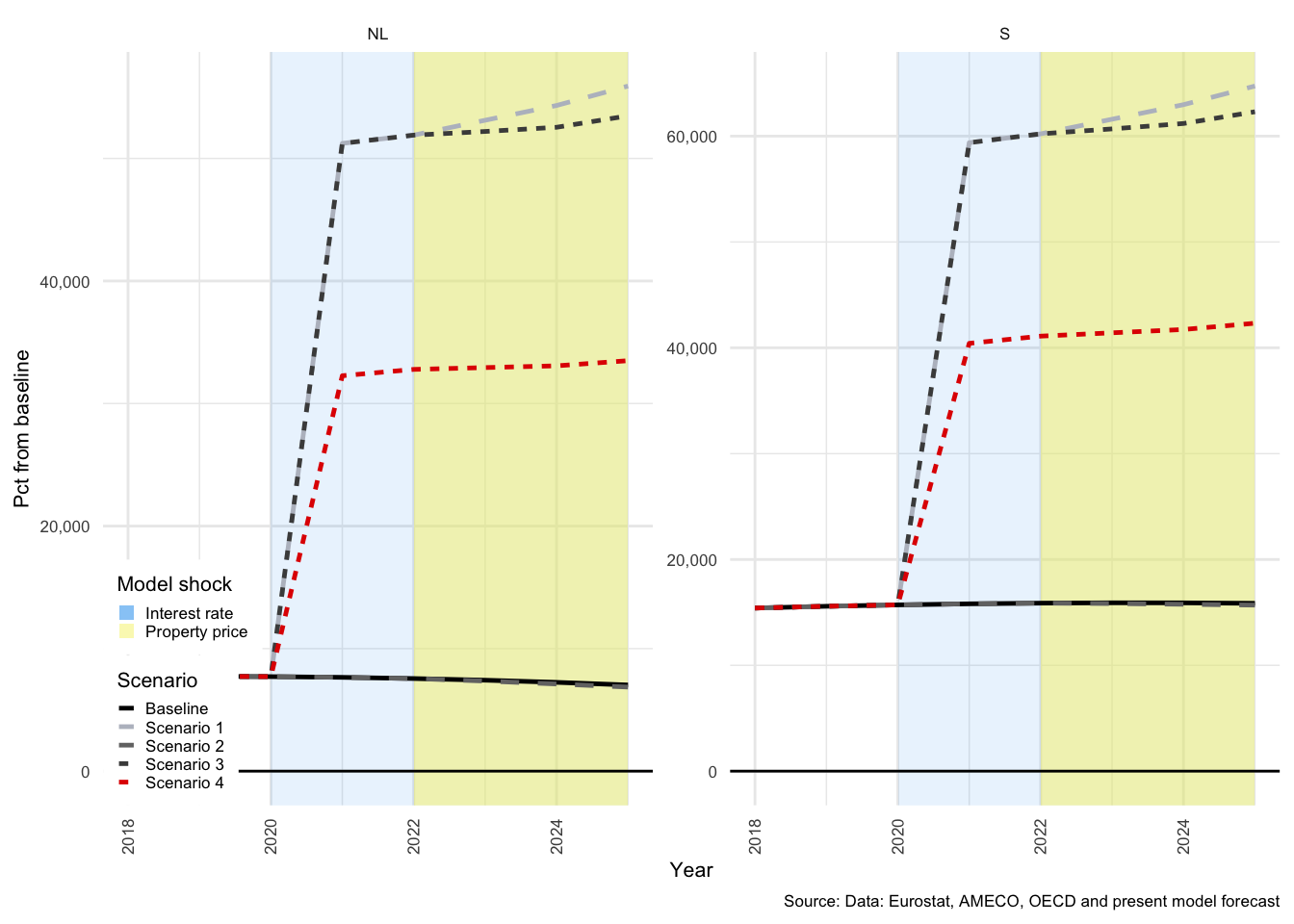

Figure 3.12: National income indicators - Scenarios 1 and 2

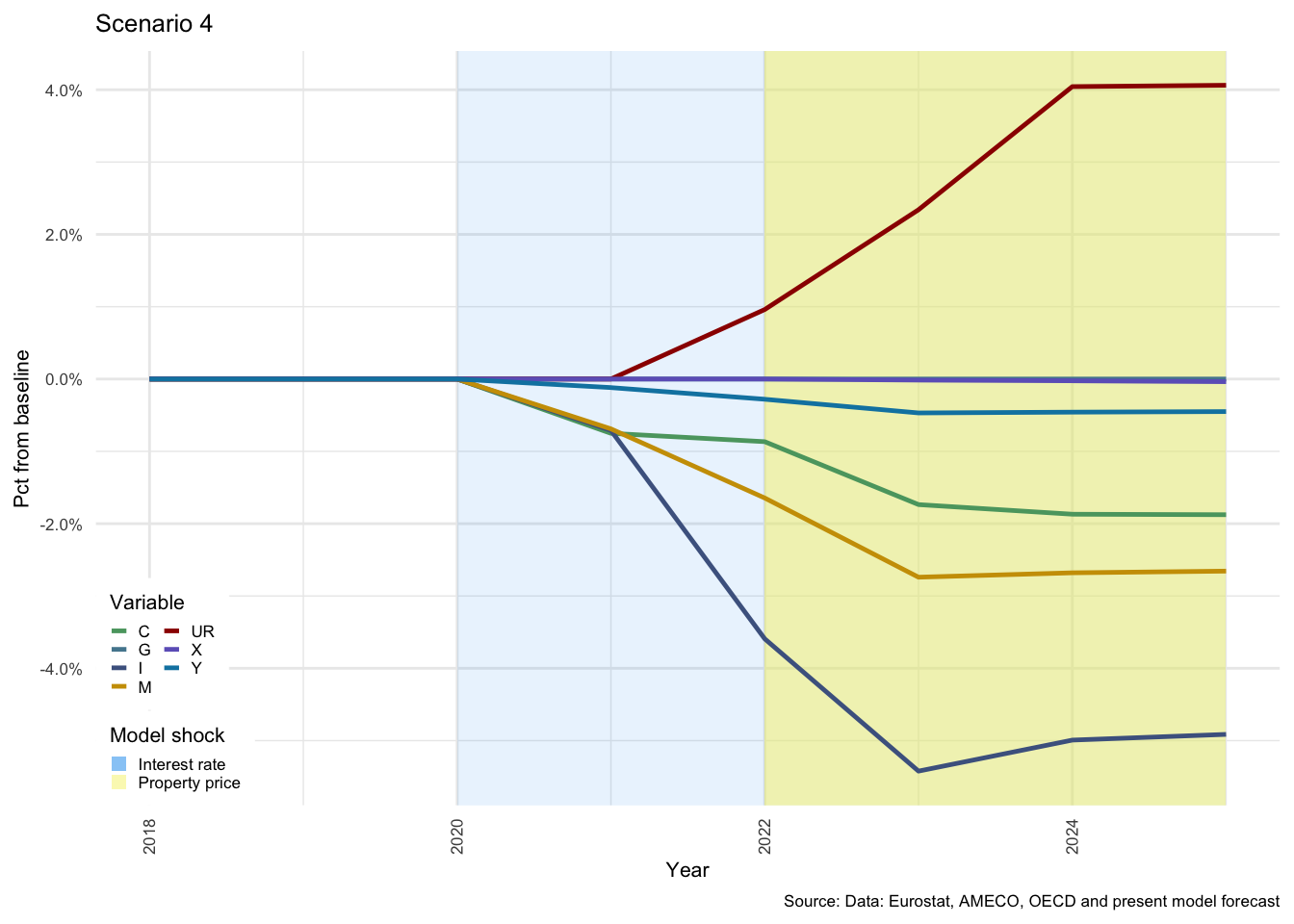

As described above, Scenarios 3 and 4 illustrate the compound effect of the two shocks under two different household debt positions. In Scenarios 1 to 3, proportion of fixed-interest debt (\(\alpha\)) is 38.91%, in Scenario 4, \(\alpha\) is set to 80%. The primary impact of this shift is a reduction in the sensitivity of household disposable income to a dramatic rise in interest rates.

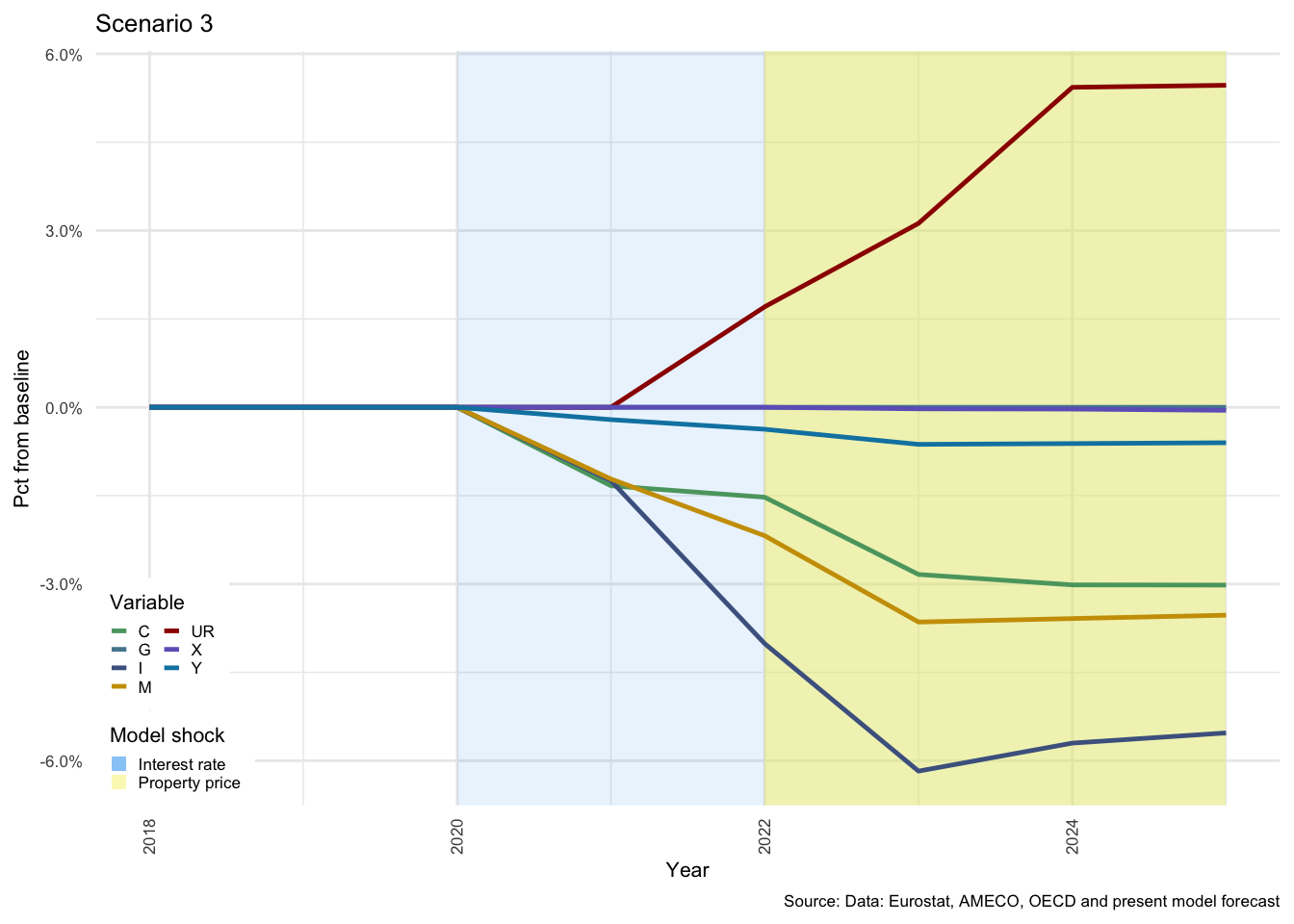

As expected, the effects of the combination of the two shocks are significantly dampened when \(\alpha\) is higher. This is clear from the scales in Figure , where on the left for Scenario 3, investment drops just below -6% compared with -5.5% on the right for Scenario 4. This pattern repeats itself throughout this results section.

Figure 3.13: National income indicators - Scenarios 3 and 4

GDP is also somewhat better protected from the shock in the latter case. The unemployment rate (\(UR\)) increase is a compound effect of the two shocks, and is also significantly higher in Scenario 3 than in Scenario 4. The number of persons employed are determined by the NFC, and is a function of the level of \(Y\) in the previous period and changes in the size of the labour force. Exogenous growth in the size of the labour force combined with a decline in economic activity, drive the proportion of unemployed persons upwards. This also results in a rise in the level of social benefits drawn by HH from GOV, but this will be discussed in the sections for each sector below.

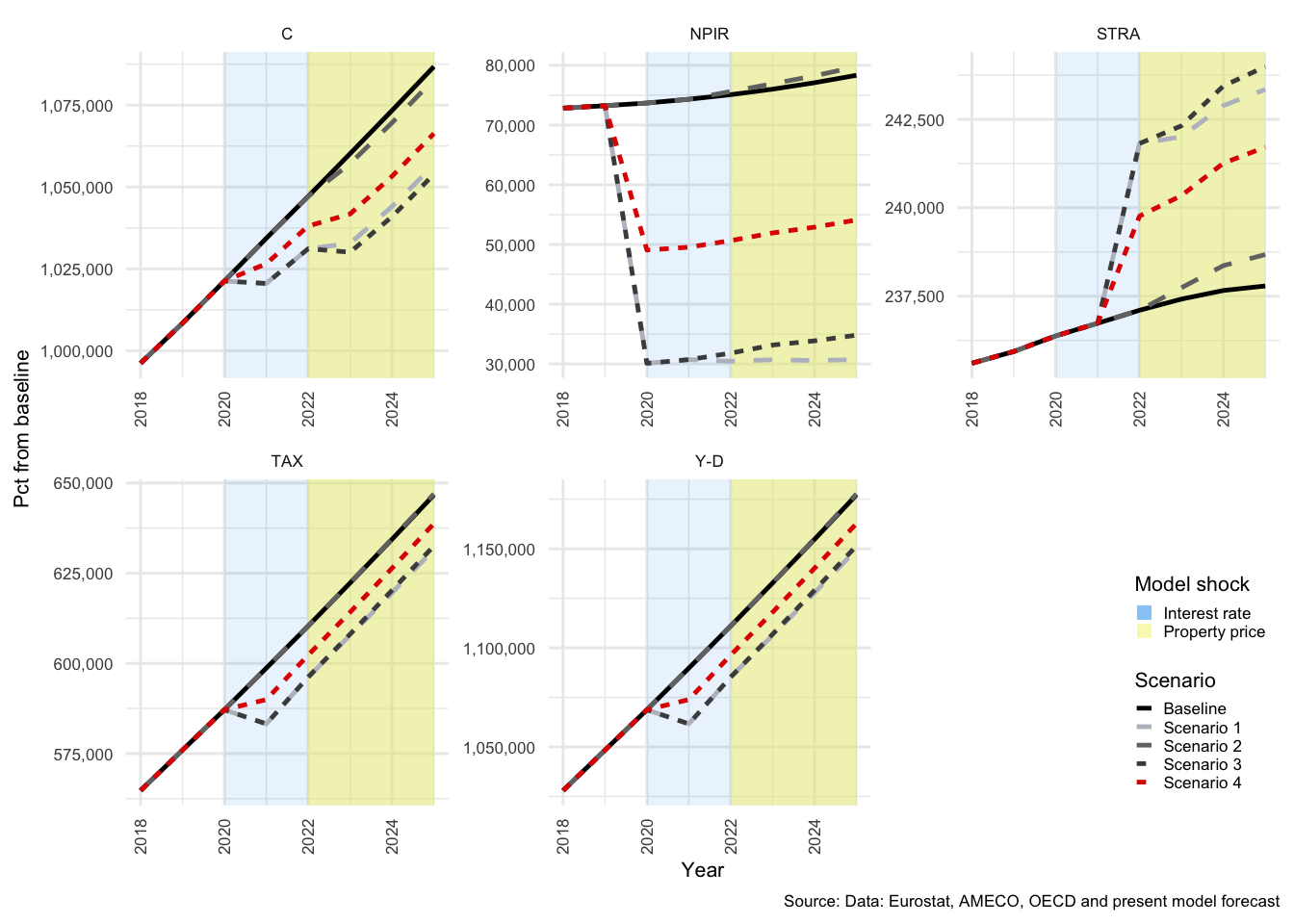

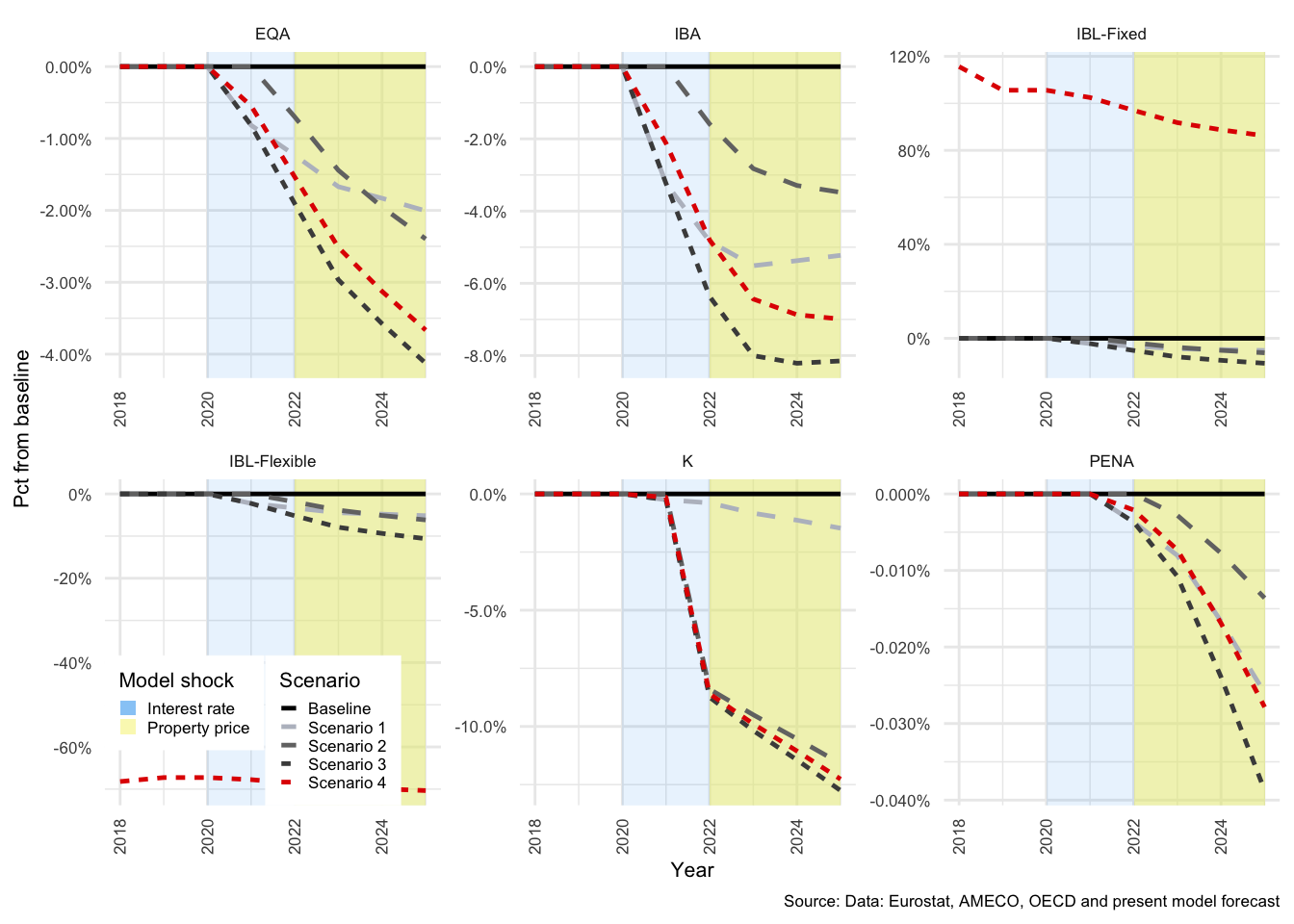

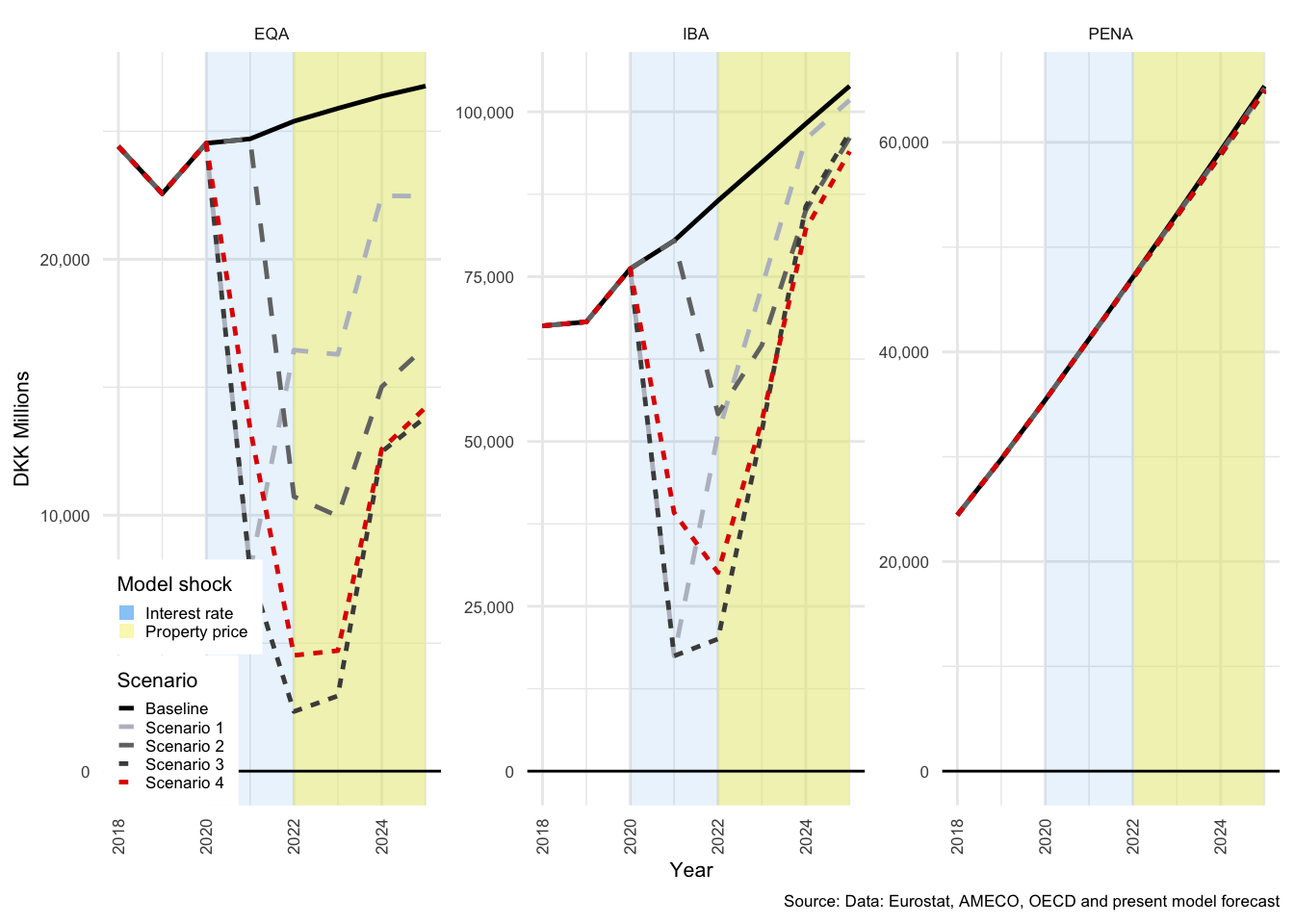

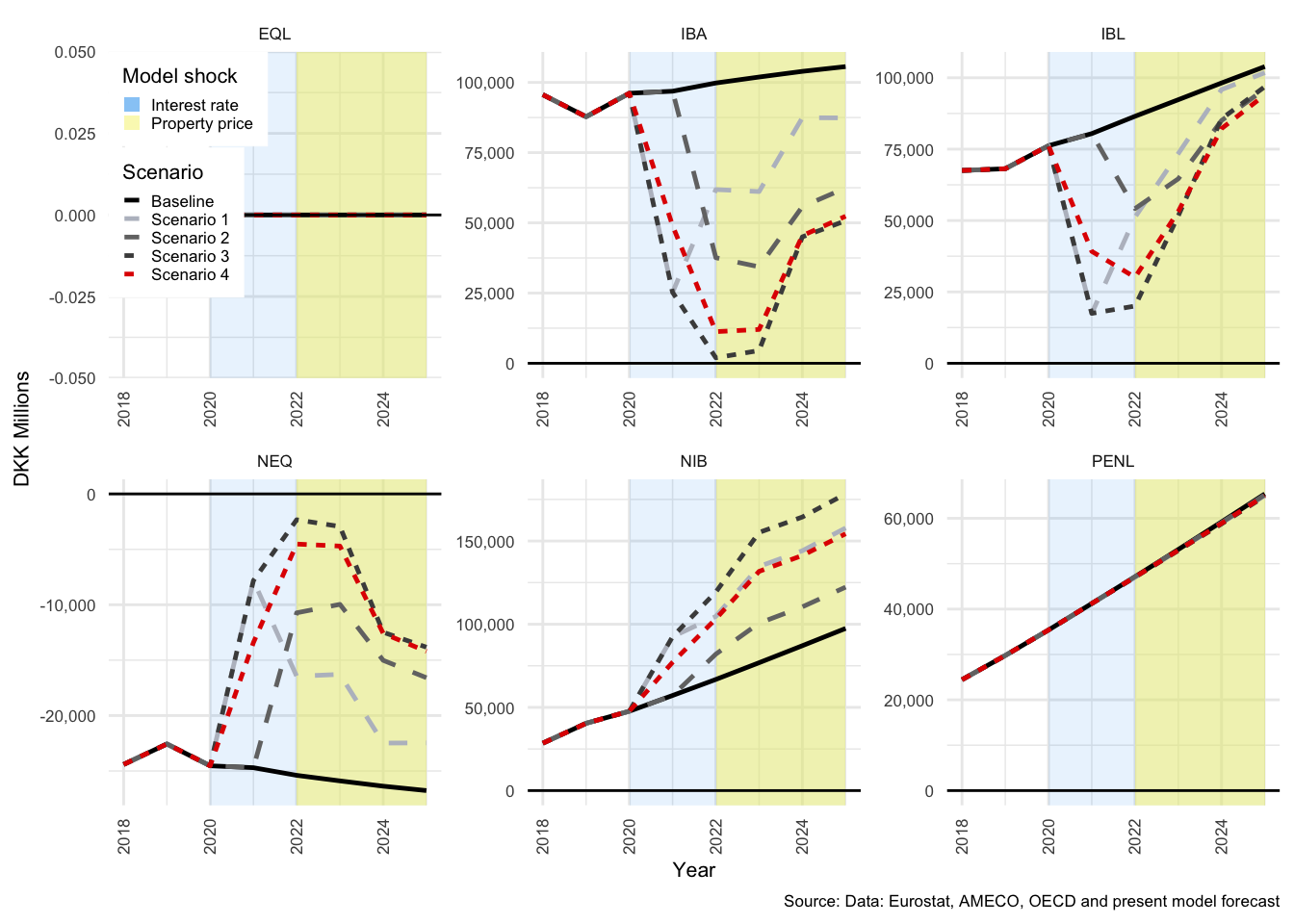

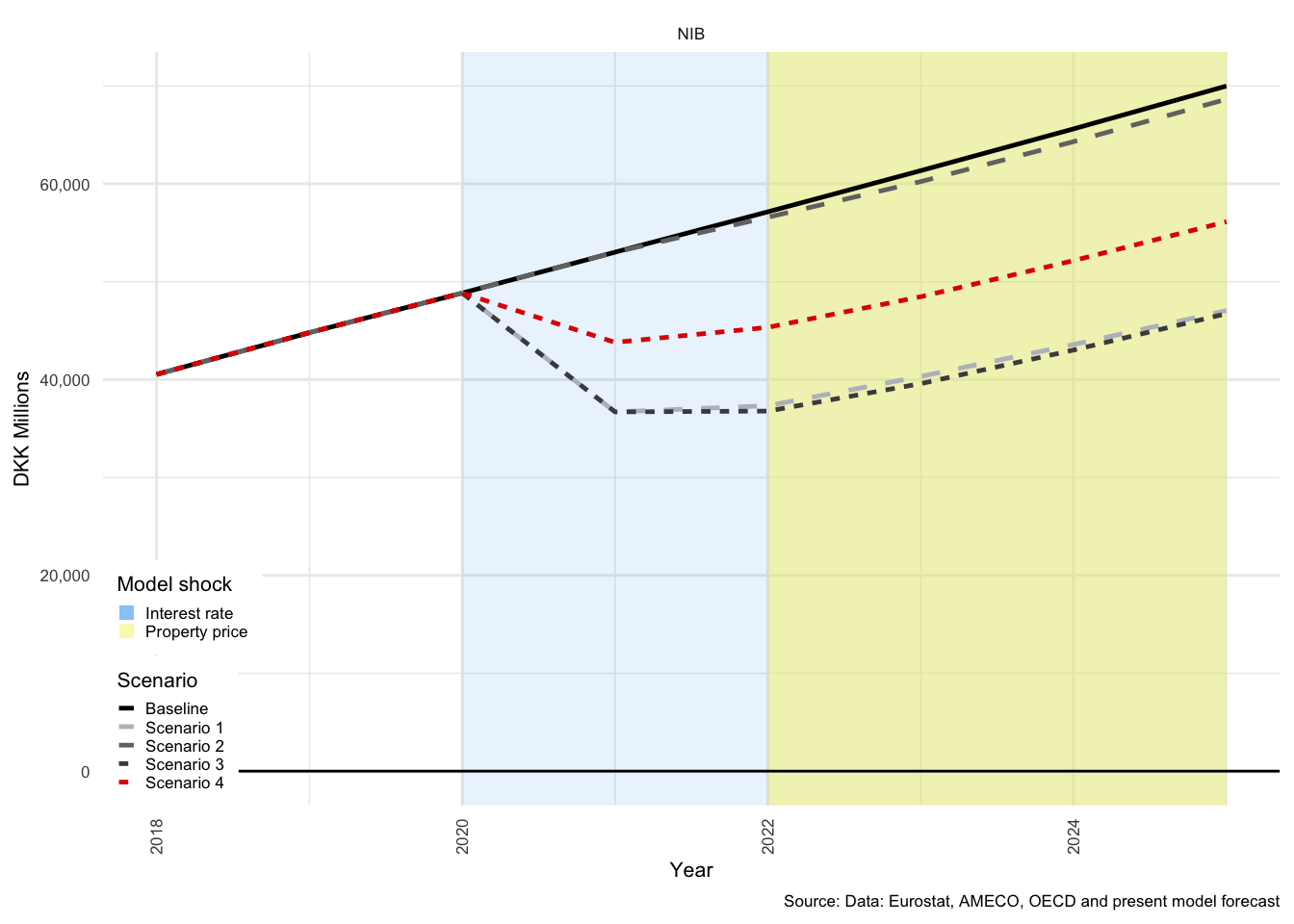

In many of the charts that follow, all scenarios are displayed for each of the variables. This allows for a comparison of the impact of the shocks. The baseline scenario is illustrated by a solid black line, Scenario 1 by a light-grey, dashed line. Scenario 2 by a medium-dark-grey, dashed line. Scenario 3 by the dark-grey short-dashed line and Scenario 4 by the red short-dashed line.